Open access peer-reviewed chapter

Open access peer-reviewed chapter

Abstract

Exploring the underlying issues of low uptake of health insurance by rural communities is a subject of growing importance for the attainment of inclusive health. Insurance plays a key role in many aspects of community development, especially the vulnerable and marginalized groups. Agreeably, human health insurance uptake in many developing countries seems to be increasing with the mandatory government policy direction that compels all employed citizens to subscribe to the health insurance policy. This study answers the question why health insurance presents a low uptake in the health systems. We reviewed 55 journal articles and 20 practitioner websites covering the period between 2003 and 2022 to understand the underlying reasons for the low uptake of human health insurance systems, especially among rural communities. The results show that policy direction significantly influences system change for the uptake of health insurance across different stakeholders.

Keywords

- insurance

- uptake

- medical system

- human health insurance

- policy

1. Introduction

Understanding the underlying issues of human health insurance among marginalized groups is becoming increasingly important. Over the years, research has shown that human health insurance remains the best choice for establishing social justice mitigation strategy [1]. The subject of inclusive human health, as outlined in sustainable development goal 3 (SDG 3), ensures healthy lives and promotes well-being for all at all ages, while sustainable development goal 2 (SDG 2) targets zero hunger for all. Consequently, there is increasing motivation to provide universal coverage of health services as a result of the Millennium Development Goal (MDG) targets for health improvement and poverty reduction [2]. Reference [2] shows that everyone has access to affordable, high-quality healthcare when they need it. Reducing the out-of-pocket costs that people incur for healthcare is an essential step toward increasing affordability. These are widely acknowledged as a barrier to access, particularly in poorer nations, and as dragging households deeper into poverty [3]. Due to errors in healthcare financing and delivery, several poor people approximately making up to 1,3 billion worldwide continue to lack access to effective and low-cost medicines, procedures, and other vital measures [4, 5].

At independence, several African countries adopted health systems that were supported and structured by the government, which suggested staff, facilities, and other inputs [6]. However, it appears that sub-Saharan African statistics on healthcare are largely insufficient. For instance, while the region constitutes only 11% of the world’s populace, 24% of the global disease burden is accounted for, and it accounts for less than 1% of health outflow globally [7]. The representation of the healthcare position in sub-Saharan Africa depicted above, combined with Africa’s position as a low-income region with poverty as a foremost obstacle to access to healthcare, demonstrates the necessity for social health insurance (SHI) as a means of providing access to healthcare for the majority of the populace [8]. Therefore, this situation agrees with and positions Kutzin’s [9] idea of the health insurance system as a means to pay for healthcare and guarantee access to services by offering a mechanism for distributing the risk of acquiring medical outflows among different individuals. Governments aim to influence and direct public life through policy, and the population serves as the unit of study for public policy [6, 8].

It is asserted that the majority of people in developing nations are based in rural regions, engaged in agriculture, and have unstable, fluctuating incomes and poor health services. In fact, the single most pressing and difficult challenge faced by several low- and middle-income countries is how to deliver inclusive and sustainable human healthcare for the more than 1.3 billion poor people who live in rural areas or work in the informal sector [4, 5]. They work as farmers, peddlers, day laborers, tax drivers, employees of the informal sector, store proprietors, and independent professionals, among other jobs [10].

Consequently, health systems are key to making and contributing to the agriculture market system and particularly food systems. Farmers will contribute positively to the economic growth of developing economies. Hence, the importance of the health insurance mechanism as an edging tool for rural farmers becomes important for them to remain and keep improving in both production and productivity in many aspects, including agriculture, education, community, and social stratification development [11]. The policy position of the government on health insurance may appear to influence the level of inclusivity in participation by marginalized populations. The government has the mandatory responsibility to ensure healthy populations, which will translate into increased productivity gains across various sectors of the economy [12]. Therefore, the health insurance system plays a key role in many aspects of community development, especially for vulnerable and marginalized groups in developing countries, where the government has developed a mandatory policy direction that compels all employed citizens to subscribe to the health insurance policy, yet gaps in adoption remain unknown among many citizens [13]. Albeit the low uptake, in the field of public health and health policy making, health insurance has been proposed to be a significant safety net for low- to middle-income residents by lowering emergency medical costs for all social classes [14, 15].

But historically, there have been a number of factors that have made it difficult for the underprivileged in sub-Saharan Africa to get healthcare. These include insufficient medical staff, facilities that are located far from intended beneficiaries, poor management of healthcare institutions that promote resource waste, and patients paying the majority of healthcare costs out of pocket [8]. The widespread belief that curative healthcare therapy is preferable to preventive healthcare therapy is another obstacle. This condition leads to issues of unfairness, inequality, and poor service quality. The concept of universal health coverage can be used to address the issue of low health outcomes in the developing countries, especially in Africa, even if discrepancies in health status are a global issue affecting health systems [8, 16].

Finally, globally, we have all committed to worldwide healthiness coverage. This is a tactical component of the post-2015 Millennium Development Goals (MDGs) intended to lower household and individual health costs, which are a significant contributor to poverty in many nations. The principle of leaving no one behind as Universal health coverage (UHC) is “the single most powerful concept that public health has to offer to address deep rooted health inequalities. It is regarded as a powerful equalizer that abolishes distinctions between the rich and the poor, the privileged and the marginalized, the young and the old, ethnic groups, and women and men,” according to Margaret Chan, Director-General of the WHO” [6, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18]. Therefore, medical health insurance systems are important if universal health coverage is to be achieved. It is against this reason that this study tries to answer the question why health insurance presents low uptake in the health systems.

2. Methods and materials

This section provides an outline of the approach employed to achieve the research objectives. Electronic databases, including Google Scholar, SciELO, AGRICOLA, SpringerLink, ScienceDirect, and Scopus, were searched for scholarly articles for performing a narrative review. Initial searches were made using a broad Boolean search phrase that includes the terms “health insurance for humans,” “insurance systems,” and “health insurance coverage.” The term “insurance system,” according to Cieza [19], denotes a health system that functions in unison and is encompassed of trained and motivated health workers, a well-maintained infrastructure, and a reliable supply of medicines and technologies, supported by adequate funding, robust health plans, and evidence-based policies. Subsequently, the search focus was narrowed down to include only topics concerning health insurance systems, public policy, community-level health insurance interactions, and adoption. Moreover, the top search engines offered free access to full-text articles. Where these connections could not be located, we utilized research websites such as ResearchGate, which provided the option of getting the complete text directly from the authors. Finally, it was required to use the Google Search engine in order to source research papers and reports that may have been ignored during the initial search. First, the reference lists of included research or review papers were combed through, followed by an examination of all journals that cited each of the included articles. Additionally, works published between 2003 and 2022 were evaluated.

3. Attempts to achieve inclusive human medical insurance coverage by various nations

3.1 Health insurance and health insurance systems

An advanced and risk-pooling system known as health insurance is used to pay for medical expenses that result from disease. These costs may be connected to hospitalization, medication, or medical appointments. Social and national health insurance could increase access to healthcare for all individuals and shield them from the financial risks associated with diseases [6, 17].

The achievement of insurance for all is highly dependent on a functional health insurance system that equally needs to obey the economic rules of supply and demand in the health sector, taking into consideration the people at the bottom of the pyramid, the guiding rules, and the supporting functions. For the system to function, it must respond to several factors that include the basic rule of demand and supply matrix as the core beginning, the various rules and regulations that need to be followed, and the support function that would ensure all the required functional support is in place for the entire health system to operate [17, 20].

It is widely acknowledged that healthcare service delivery systems and financing methods have significant consequences for people accessing and gaining from health coverage. Although national health insurance programs give people in many nations access to comprehensive and fair healthcare, putting them into place presents a number of difficulties [17].

A well-functioning health system is supported by qualified and motivated health professionals, a well-maintained infrastructure, and a consistent supply of medications and technologies, as long as it is sufficiently funded, ensuring robust health plans and implementing evidence-based policies [19]. Depending on the degree of economic growth and the political system in existence, healthcare systems vary from one country to the next. Healthcare is a primacy and a basis of worry worldwide. All countries, regardless of their private, public, or mixed healthcare system, face challenges about quality, delivery, and cost of services.

However, the World Health Organization (WHO) contends that a health system comprises of all groups, individuals, and activities whose main goal is to promote, restore, or maintain health, rather than just a pyramid of publicly owned personal healthcare delivery facilities or structures [21]. Health system targets mostly involve the enhancement of health and health equity in systems that are proactive, monetarily sustainable, and optimally efficient; they should furthermore prevent wasting resources. Nonetheless, to achieve these goals, a health system ought likewise to accomplish the intermediate goals of guaranteeing better access, effective coverage, quality, and safety of healthcare services for most of the populace [21].

Social health insurance is “a means of financing healthcare and ensuring access to services by providing a mechanism for sharing the risk of accumulating medical expenses among different individuals” [8, 9].

Furthermore, Kutzin [9] stresses the strategic significance of financial protection as well as the capability, willingness, and access to health services as fundamental for social health insurance. He contends that as public policy goals for the health sector include advancing equity, efficiency, acceptability (to providers and users), and sustainability, increasing the reach of health insurance may help with these goals [9]. However, he warns that the pursuit of broad coverage through health insurance is not the end of policy [8]. There is not a single paradigm that applies to all health insurance system designs. Priorities, populations, development, governmental structures, and other aspects differ widely among nations. This heterogeneity has given nations seeking reforms a range of experience to consider [22].

There are numerous varieties of health insurance programs available worldwide, including:

Social health insurance: Public multipayer systems with indirect provision.

National health service: Centralized single-payer systems with direct provision.

National health insurance: Centralized single-payer systems with generally private provision of medical services.

Private insurance: Some countries have private multipayer systems with indirect provision.

3.2 Human health insurance systems in perspective

3.2.1 Global

The current global insurance trends indicate challenges in both the availability and accessibility of insurance products for marginalized groups, especially in developing countries, as the example of Zambia [23]. Social health insurance (SHI), community-based health insurance (CBHI), and private health insurance (PHI) are the three most prevalent forms of health insurance plans found worldwide [24]. The requirements and coverage of these various programs vary. SHI is a mandated program in which participants are required by law to participate and pay a predetermined premium amount [25].

3.2.2 Health insurance systems in Korea

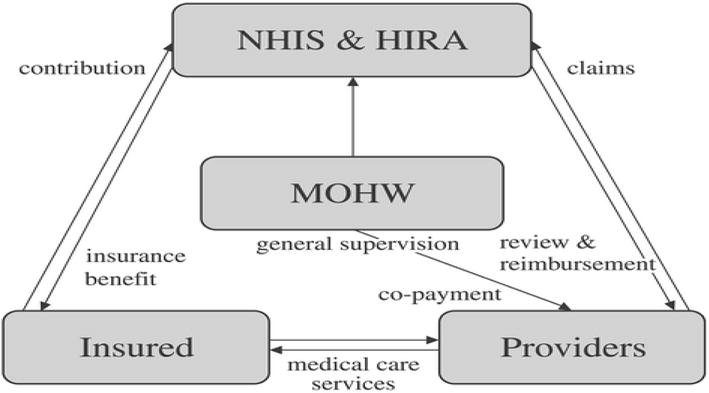

The National Health Insurance (NHI) program, which is a universal social insurance program that covers the entire population and is mandatory by law, is used to execute the healthcare system in the Republic of Korea. The NHI Service (NHIS) oversees the running of this system under the guidance of the Korean government. The sole insurer, known as the NHIS, works to improve social security by ensuring that people have access to the required medical treatment for illness, accident, pregnancy, and death. It similarly runs a free medical relief program as a practice of public support for individuals in the low-income group, for whom the application of social insurance is tough through NHI [26, 27]. This suggests that medical assistance plays a significant role as a social security system in Korea for people in lower income categories who pass a means test and are supported by local governments rather than the NHI system [24]. Loyalists and veterans who get benefits as persons of national merit are also incorporated in the medical relief group. The percentage of medical relief beneficiaries is about 3% of the entire population in South Korea [28]. The rapid introduction of a private health insurance (PHI) program can deprive important healthcare application by those who are poor, while the benefits of the adoption of PHI are moderately modest [28, 29].Figure 1 displays the association that takes place between the insurers, health service providers, and NHIS and Health Insurance Review & Assessment Service (HIRA) in delivering comprehensive and long-lasting health medical insurance in [28].

Figure 1.

The figure shows the associations among key parties of Korean National Health Insurance (NHI) that include the Ministry of Health and Welfare (MOHW), National Health Insurance Service (NHIS), and the Health Insurance Review & Assessment Service (HIRA). Adopted [

3.2.3 Health insurance approach: Swiss system

Multiple private insurers operate in regulated, competitive markets as part of the health insurance systems of Switzerland and the Netherlands, which offer universal coverage. The systems share a number of characteristics, including an individual mandate, basic benefits that are standardized, a strictly regulated insurance market, and funding plans that make insurance affordable for low- and middle-income families. The degree of centralization, the basis for insurer competition, the availability of managed care, and the extent to which they rely on patient cost-sharing to influence participants’ care-seeking behavior are all significant distinctions between the two systems. Since 1996, the Swiss system has been governed by a health insurance law designed to provide access to treatment, make it more affordable, and keep costs in check. Every resident must obtain fundamental health insurance from one of the several rival private insurers operating within the confines of the social insurance law’s established market rules. All applicants must be accepted by insurers during designated open enrollment times with community-rated premiums, and insurers must be nonprofit. About 12% of enrollees are enrolled in managed care plans of some kind, mostly fee-for-service plans with a primary care gatekeeping component [30]. The 26 cantons of Switzerland serve as the insurance markets and insurance mandate. Numerous strategies have been used by cantons to enforce coverage. The income tax system provides premium subsidies. To identify people without coverage, tax data can be compared to enrollment data from insurers. A third of the population and 40% of all Swiss households are thought to benefit from this premium assistance. This share exceeds 50% in several cantons [30]. The canton or the community of residence may designate an insurer for a person who needs medical care but has no insurance. The Federal Office of Public Health (FOPH) oversees the requirement for basic health insurance. The Federal Office of Private Insurance (FOPI) has distinct regulations for supplemental insurance, which may be provided by both basic health insurers and other insurance firms. The same set of benefits must be provided by all basic insurance schemes [31].

3.2.4 The Dutch health insurance system

A health insurance scheme resembling the present German system existed in the Netherlands until 2006 [31]. Most people participated in nonprofit “sickness funds” funded by fixed-income donations; those with greater incomes purchased commercial insurance. This two-tiered system has been replaced by a single system under the new Health Insurance Act, where all citizens are required to get minimum essential coverage from a private insurer, which may be for-profit or nonprofit and includes insurers that formerly served as sickness funds. However, most Dutch people (90% or more) choose supplemental insurance that includes extra benefits like adult dental treatment that are not included in the standard package. By limiting possibilities for profit or loss by choosing a particular health risk, insurance market regulations and oversight, such as risk equalization funds, aim to concentrate insurance competition on quality and cost performance (value). Each insurer determines its rate, which cannot be affected by enrollment, health, or any other factors. Individuals enrolling through collective agreements, such as employer groups, may receive discounts from insurers of up to 10%. About half of overall expenses are covered by income-based premiums, while the remaining four-fifths are put into the insurance fund by the government out of general revenues for child coverage [32]. Through a national premium credit scheme, people with lower incomes are given a healthcare allowance to assist in paying the flat premium. An estimated 40% of households are eligible for this help [31].

3.2.5 Health insurance system in Macedonia

The Health Protection Law (1), which was amended in 1993 (2) and 1995 (3), inaugurated the Republic of Macedonia’s present system of health insurance in 1991 (3). This law specifies three different types of health insurance: mandatory, supplementary mandatory, and optional insurance for specific categories of medical care.

Obligation, reciprocity, and solidarity are the cornerstones of mandatory health insurance. Every insured individual has unlimited access, as needed, to the healthcare and rights provided by their health insurance, including the essential healthcare rights protected by the law’s mandated health insurance. On the other hand, continuing to make contributions toward health insurance is a requirement for all employees or other insurance holders. Regardless of the level of pay or income, frequency, or amount of health services utilized on account of the health insurance funds, the contribution rate is the same for everyone [33].

There is supplemental mandatory insurance available for certain risks or different demographics. In cases of workplace injuries and occupational diseases, it uses preventive and screening methods as well as medical care. The insured’s further agricultural, manufacturing, or other endeavors are also covered. For medical services that were not covered by required health insurance, voluntary health insurance was developed. It covers the use of a few certain medical services as well as those that are provided at a better standard or level of comfort than those provided by mandatory health insurance, i.e., standards set by the Ministry of Health.

The state budget covers the costs of healthcare services for Republic of Macedonia residents who are not Fund insured in the following circumstances: healthcare for (a) children and teenagers up to the age of 18, students and pupils up to the age of 26, and those over the age of 65; (b) women’s healthcare relating to pregnancy, delivery, motherhood, and contraception; and (c) the treatment of infectious diseases, mental illnesses, complications from rheumatic fever, cancer, diabetes, chronic dialysis, progressive nervous and muscular diseases, cerebral paralysis, multiple sclerosis, cystic fibrosis, similar diseases, epilepsy, alcoholism, and drug addiction [33].

3.3 Africa

Exploring social health insurance’s potential to improve access to and affordability of healthcare in Africa is currently a topic of great interest. Various strategies are currently being tested in a number of nations [34, 35].

3.3.1 Health insurance systems in sub-Saharan Africa

Literature analysis suggests that an increasing number of nations are adopting health insurance plans to satisfy the healthcare needs of their populations [6, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23, 24, 25, 26, 27, 28, 29, 30, 31, 32, 33, 34, 35, 36]. Social health insurance (SHI) and community-based health insurance (CBHI) are more frequent in Asia and Africa than National Health Services. Developed countries in Europe are more likely to have national health insurance systems (NHIS) (Physicians for a National Health Program (2010). However, private health insurance (PHI) plans flourish in sub-Saharan Africa [8] because of the inability of public health systems to cover the needs of the entire population. Therefore, private employers provide their employees with health insurance policies. The following elements play a strong role in African countries toward the adoption of social or community-based health insurance systems.

Healthcare sector underfunding [8, 36]: most African nations spend less than US $10 per person per year, despite the World Health Organization’s recommendation of US $27 per person annually. Additionally, although African leaders pledged in the 2001 Abuja Declaration to devote 15% of their annual budgets to health, annual health spending in the area rarely reaches an average of 5% of gross domestic product (GDP) [35].

Inequitable and inefficient allocation of the few resources are allocated to the public health sector [9, 35]. This frequently leads to regional inequalities in the distribution of healthcare infrastructure between rural and urban areas and low-quality health services [37]. Health issues are almost always worse in areas with few resources and access to care for those who need it the most.

A poverty scenario: the rate of absolute poverty in sub-Saharan Africa is about 54%, there is a large illness load, and many people die. Malnutrition, HIV/AIDS (human immunodeficiency virus/acquired immunodeficiency syndrome), and other diseases like malaria that can be prevented [38], additionally diarrhea, and respiratory tract infections are the major causes of death, on top of other mortality causes like injuries from accidents, violence, and war.

Lack of human resources in the health sector is primarily the result of brain drain, which is brought on by subpar working and pay conditions, subpar healthcare infrastructure, and subpar medical technology. Other issues include the shortage of medical professionals in some nations and the overcrowding of medical professionals in a few urban areas at the expense of rural communities [35, 39].

Inadequate, outdated, underfunded, and data-reporting health systems that overlook traditional, religious, and other nonmedical services of care that can supplement conventional medical care [35, 40].

In addition to these characteristics just described, the following traits spur nations in the region to implement social health insurance:

The idea of being one’s brother’s keeper is one that Africans generally respect and value. This complies with the social health insurance premise of from each according to his capacity, to each according to his need.

Even without direct government engagement, an increasing percentage of Africa’s private sector, especially the urban private sector, is adopting joint health insurance programs for its employees [35].

Due to rising poverty, there is a growing army in Africa of the unemployed, the underemployed, and the unemployable (who received substandard education and want jobs whose demands they cannot cope with) and the destitute, who need access to healthcare as human beings. In the face of dwindling government resources, reduced healthcare funding, rising health inequalities, and other concerns of foreign donors who have been contributing to healthcare in Africa, social health insurance would be appropriate for sub-Saharan Africa [35].

More importantly, public or universal social welfare systems are not yet developed in many African countries. Therefore, the expanded African interpretation of the concept of “family” (in terms of determining appropriate beneficiaries) would make whole-scale adoption of Western health financing systems problematic for Africans [8].

3.3.2 Health insurance systems in Ghana

Ghana’s National Health Insurance Act (Act 650) was enacted into law in 2003, however implementation (in terms of benefit access) did not start until the fall of 2005 [41]. Membership (either through the District Health Management Information System (DHMIS) or through a private insurance policy) is required. Employees in the formal sector are subject to Social Security and National Insurance Trust (SSNIT) payroll deductions that are not their choice. The informal sector is assessed for paying premiums, which ought to be based on income. There is a 6-month waiting period before being eligible for benefits at first. In order to control the market, the National Health Insurance Authority (NHIA) was created [41]. This includes accrediting providers, settling on contribution rates with plans, resolving disagreements, running the National Health Insurance Fund (NHIF), and approving cards. Benefits cannot be transferred across district plans, unless each district has a DMHIS with a minimum of 2000 members. Every DHMIS must submit annual reports to NHIA and have its financial records audited on a yearly basis [41].

The National Health Insurance Authority does not offer subsidies to private MHIS. Every 2 years, the NHIA and license programs are overseen by the National Health Insurance Council (NHIC), the Executive Secretary of the NHIA, as well as officials from the Ministry of Health, Ghana Health Service, governing bodies, consumers, and other key stakeholder organizations [42]. The president appoints the chair and executive secretary. The NHIC submits a funding formula for yearly approval to Parliament and submits an annual report to Parliament on the usage of money. A board oversees each DHMIS. For managing complaints against providers or schemes, rules are set.

The National Health Insurance Levy (NHIL), which accounts for 2.5% of value-added tax (VAT) and 2.5% of employees’ salaries in the formal sector, provides funds for the program. Additionally, DHMIS receives funding from premia for participants in the informal sector, which are determined in accordance with the National Health Insurance Authority (NHIA). However, hybrid forms of SHI are also fairly common, in which the government pays payments for people who would otherwise have trouble doing so, such as the unemployed and the destitute. However, it differs from other approaches, in that it distributes the responsibility for healthcare financing among individuals and the private sector as well, rather than relying solely on public funding [34, 43].

3.3.3 Health insurance systems in Zambia

Healthcare has long been offered in Zambia by public, religious, and commercial organizations. The Health Professions Council of Zambia (HPCZ) oversees and issues licenses to all healthcare facilities in the nation. Primary healthcare (PHC) services, such as health posts, health centers, and level-1 hospitals, make up the public health system. Hospitals at levels 2 and 3 offer specialized treatments like obstetrics, internal medicine, and surgery. In public health institutions, user fees were completely eliminated at the PHC level by the government in 2012. These healthcare centers are designed to offer free treatment to everyone. In addition, free medical care is meant to be provided to patients who are sent from these PHC clinics to level-2 and level-3 hospitals. This regulation reduced out-of-pocket costs for households [44, 45]; however, the widespread scarcity of medicines and insufficient support for the healthcare industry spurred the creation of a national health insurance scheme [45].

Recently, Zambia introduced health insurance, in 2018, when it passed its National Health Insurance (NHI) Act to provide “universal access to quality health services” [46]. The National Health Insurance Management Authority (NHIMA), a semiautonomous organization presently in charge of obtaining services from various healthcare facilities, paying residents’ contributions, and distributing benefits to beneficiaries, was founded by the Act. The existing statutory instrument mandates that employees contribute 1% of their monthly salary, with employers matching that amount [47]. Self-employed people who work in the informal economy are required to contribute 1% of their declared monthly income, with a minimum contribution of 60 kwacha (US$4) per month. In the formal sector, deductions from wages started in October 2019, while payments to healthcare institutions started in February 2020. As of February 2022, there were 1.35 million principal members and 500,000 secondary registered beneficiaries, respectively. Principal members are allowed six beneficiaries under their membership [48]. Contributions are not required of individuals over the age of 65, or those who are physically or mentally impaired. It is crucial to understand the consequences of health insurance’s purchasing functions and predict how they will affect access to high-quality treatment in the future since the industry is still in the early stages of implementation.

4. Public policy as key driver for public health and social health insurance

For many countries, both developed and less developed, the need for inclusive healthcare services appears to be driven largely by public policy instruments by governments. The degree of government attention and prioritizing in effecting health improvement has been noted by various academics as a crucial driver [31, 49]. The concept of the “public sphere” encompasses all facets of daily life or activity that are thought to need governmental oversight, involvement, or regulation [50, 51]. Public policy is concerned with the general population and its issues, and it will probably represent “how, why, and to what extent governments pursue particular courses of action or inaction” [8, 52]. As a result, public policy makes an effort to discuss the nature, reasons for, and consequences of governmental action or inactivity with an emphasis on the welfare of its citizens [49]. As a result, public health addresses important scientific, social, economic, environmental, and political issues that have an impact on the well-being of the overall populace [53, 54]. The concern for the population, whose interests the government was established to defend and develop, is a key relationship between public health and public policy [55].

5. Factors affecting uptake of health insurance

Numerous factors, including institutions, healthcare orientation in rural communities, and household-specific characteristics, have been identified in the literature as influencing the acceptance of medical health insurance among the population in developing nations.

5.1 Institution factors

Individuals may establish their own opinions on the ability of the public health system to deliver quality care in the setting of health insurance based on their own experiences with the healthcare system and media reporting. Their willingness to sign up for national health insurance may be influenced by how confident they are in both public and private healthcare providers. People who have limited financial resources and believe they will not require medical care in the future may even be less willing to sign up for a health insurance plan [45]. Other social science studies have found that confidence in institutions influences decision-making [56].

For example [57], asserted that there are critical experiences that influence the uptake of health insurance at the community level. Good experiences with health insurance for local and rural people will build confidence in the uptake of health insurance.

5.2 Healthcare in rural communities

Rural residents often encounter barriers to healthcare that limit their ability to obtain the care they need. Access to healthcare implies that healthcare services are available and obtainable in a timely manner. Yet, rural residents often encounter barriers to healthcare access. Even when an adequate supply of healthcare services exists in the community, there are other factors that may impede healthcare access. For instance, to have healthcare access, rural residents must also have:

Financial resources to cover the cost of services, such as accepted health or dental insurance by the providers.

Means to reach and use services, such as transportation to services that may be located at a distance, and the ability to take paid time-off of work to use such services.

Confidence in their capacity to communicate with healthcare professionals, especially if they do not speak English well or do not have a lot of health literacy.

Belief that they may use services without having their privacy being violated.

Belief that they will obtain high-quality treatment [58].

Health insurance systems therefore need to account for these community dynamics to be able to manage and meet the health needs. Otherwise, the rural communities risk missing even the government policy-driven health insurance systems [59, 60].

5.3 Household-specific factors

Many scholars have indicated that the level of awareness of health insurance determines the uptake of health insurance [61]. As much as health insurance is seen as an option for inclusive health for all, it all comes down to the household itself, understanding its importance and health insurance investment options [62]. According to some studies, the main determinants of health outcomes are social and economic variables, sometimes known as social determinants of health, and individuals’ health habits are influenced by social and economic factors [63]. Even as the government and private sector may provide supportive options, households have a critical role in picking up the opportunities. In the developed countries, citizens are fully aware of their right to health services and take the lead in ensuring that they are covered by health insurance systems. The health system mechanisms are clear for the citizens to decide on various options based on their abilities [64, 65]. An extensive body of economic and social research has examined how people make decisions in the face of uncertainty, including choices about health insurance [56]. In neoclassic theory, models explaining the demand for health insurance show how rational agents evaluate their expected utility with insurance compared to their expected utility without insurance [66, 67].

6. Discussion

Based on a survey of the literature, different governments in both developed and developing countries employ different health insurance systems. There is not a single paradigm that applies to all health insurance system designs. Priorities, populations, development, governmental structures, and other aspects differ widely among nations. This heterogeneity has given nations seeking reforms a range of experience to take into account [22]. However, government policy plays a key role in setting the agenda for how to achieve universal health. For many countries, both developed and less developed, the need for inclusive healthcare services appears to be driven largely by public policy instruments by governments. The degree of government attention and prioritizing in affecting health improvement has been noted by various academics as a crucial driver [31, 49]. The different countries reviewed point out the different strategies of health insurance policies. In the case of developed countries with functionally competitive private insurance markets, they play a key role in ensuring health insurance is provided through them, with the government ensuring low- and middle-income citizens are taken care of. In developing countries, the government takes up a lead role through health insurance policies that compel all employed salaried employees to contribute toward the health insurance to cater for the poor and vulnerable families, though they are also supposed to contribute to the schemes.

After an extensive review of the different countries’ health insurance systems, governments put up different measures to ensure universal health insurance systems. Critical to the functional health insurance systems are the funding and revenue mechanisms the country has put in place. In some countries, the government has a national health insurance system that covers 100% of the population. However, the target group is not using publicly funded health services in many nations where the government aims to pay for and provide free, or virtually free, treatments for rural inhabitants and the poor. The government’s funding of primary care at the village and township levels is inefficient, according to thorough research conducted in low-income nations. While funds allotted for the procurement of drugs and supplies are insufficient, public funds are typically used to sustain the salaries of health personnel, regardless of whether they are providing satisfactory services or not. Therefore, rather than producing an efficient system for delivering healthcare, this strategy develops a public employment program. As a result, it appears that the supposedly “free” treatments may actually increase in cost as individuals are forced to pay for their own medications and other medical supplies [10]. Thus, health insurance systems become key to meeting the health needs of the people. Achieving universal health insurance requires dynamic government policies that also consider the private sector’s involvement and contribution toward achieving universal health objectives. The analysis of a few examples from the Asia and Africa regions highlighted a number of actions that governments may take to increase and improve human healthcare systems. This included creating connections with established healthcare networks, subsidizing contributions for the underprivileged, and offering technical support to enhance a scheme’s administrative capabilities.

Health insurance systems appear to be lacking in rural communities. The majority of nations attempt to actively provide for their rural populations by running public clinics, although it is frequently challenging to fill them with skilled medical professionals. People who respond to this advertisement usually work irregular hours and offer subpar services. Pharmaceuticals and other medical supplies are sometimes lacking inside the institutions. People who fall ill are frequently obliged to turn to home remedies recommended by traditional healers and pharmacists as their first line of treatment. The majority finally seek treatment from the few rural public and nonprofit hospitals for serious sickness episodes [10]. Even in the public sector, patients receiving care in hospitals frequently have to make an official copayment or unofficial price. As a result, many people are forced to decide between ruining their families and paying for necessary medical care. According to studies, more women and children than men are forced to forego medical care. Furthermore, studies show that even when the government offers free or almost free services, disadvantaged households nevertheless spend a sizeable portion of their income on unofficial fees [10]. Up to 80% of all healthcare costs in low-income nations are covered directly out of pocket by patients. Large medical expenses (such as inpatient hospital services and expensive outpatient medications) are a significant contributor to poverty, according to studies in numerous countries. Reaching out to rural health facilities with insurance systems requires both awareness creation for the rural people as well as funding mechanisms that should support or subsidize for the rural and informal people.

7. Conclusion and recommendation

Health insurance systems take different strategies from different governments and countries with a focus on inclusive health. Poor communities and farmers are at risk of compromised health. This has multiple implications for the farmers’ health, agriculture production risk, food security risk, and economic risk. Therefore, the health systems that are responsive to the different levels of society are key to the total well-being of the people. Inclusive health remains key for economic and social development. Information on the health system is key if people are to adopt health insurance products and services.

The fundamental causes of many current health issues in low-income nations are frequently well understood; there are frequently effective and reasonably priced medications, operations, and other therapies. Potentially beneficial policies and programs, however, frequently fall short of reaching the homes and communities that most require them due to a number of issues with resource mobilization, risk sharing, resource allocation, and purchasing arrangements, as well as issues with the delivery of goods and services to rural and low-income populations. Hence, well-functioning health insurance systems may be the answer to edging out and protecting the rural poor. This must be supported by concrete public policy driven by governments.

Infrastructures for health services and sufficient financial mechanisms are essential for advancing the goal of universal health coverage worldwide. Social and national health insurance programs, whether they are run by numerous or single payer, are crucial to raising the standard of healthcare and ensuring equal access for all residents. However, putting ideas into practice is difficult and calls for continual adjustments to a situation that is rapidly changing. The key issues shared by all population groups are reaching them through insurance-based methods, an aging population, addressing the rise in medical care demand, and securing sustainable financial resources. The importance of various issues and the approaches taken to address them vary by nation. However, the demands of the populace must always serve as the primary criterion for creating effective healthcare systems. The premiums should be tailored to individual levels to aid the less fortunate members of the community, and enrollment centers should be established in each town for convenient accessibility.

Conflict of interest

There is no conflict of interest in this study, whether financially, nonfinancially, or otherwise. Therefore, we, the authors, declare no competing interests.

Author contributions

Joshua Munkombwe: Production of the first draft, review, and editing of writing, as well as ideation, methodological development, data analysis, and writing.

Dr. Jackson Phiri: Production of the first draft, review, and editing of writing, as well as ideation, methodological development, data analysis, and writing.

Declaration of competing interest

The authors affirm that they have no known financial or interpersonal conflicts that would have appeared to have an impact on the research presented in this study.

Ethical approval

Our article is a narrative review of the literature. It does not involve human participants or animal subjects. Therefore, it did not require the approval of an Ethics Committee.

References

- 1.

Moghaddasi H, Hosseini A, Asadi F, Esmaeili M. Problems of health insurance systems and the need for implementation of a reform approach. Journal of Health Administration (JHA). 2011; 14 (44):71-80 - 2.

World Health Organisation. Moving Towards Universal Coverage Series. Geneva: WHO; 2006 - 3.

Xu K, Evans D, Kawabata K, Zeramdini R, Klavus J, Murray C. Household catastrophic health expenditure: A multicountry analysis. Lancet. 2003; 362 :111-117. DOI: 10.1016/S0140-6736(03)13861-5 - 4.

ILO. Social health protection. An ILO strategy towards universal access to health care. Social security policy briefings. In: Paper 1/ International Labour Office, Social Security Department. Geneva; 2008 - 5.

World Health Organization. Everybody business: strengthening health systems to improve health outcomes: WHO’s framework for action. Geneva: WHO; 2017 - 6.

Fusheini A, Eyles J. Achieving universal health coverage in South Africa through a district health system approach: Conflicting ideologies of health care provision. BMC Health Services Research. 2016; 16 :558. DOI: 10.1186/s12913-016-1797-4 - 7.

World Bank Group. International Finance Corporation (IFC) Annual Report. I am Opportunity: Main Report (English). Washington, DC: World Bank Group; 2011. Available from: http://documents.worldbank.org/curated/en/583971468331056156/Main-report - 8.

Olugbenga EO. Workable social health insurance systems in sub-Saharan Africa: insights from four countries. Africa Development. 2017; 42 (1):147-75. eISSN: 0850-3907 - 9.

Kutzin J. Health financing for universal coverage and health system performance: Concepts and implications for policy. Bulletin of the World Health Organization. 2013; 91 :602-611 - 10.

Preker AS. Health Financing for Poor People: Resource Mobilization and Risk Sharing. Washington DC: World Bank; 2004 - 11.

Boyce T, Brown C. Economic and social impacts and benefits of health systems. Economic and social impacts and benefits of health systems. SBN 978-92-890-5395-2. Available from: http://www.euro.who.int__data/assets/pdf_file/0006/395718/Economic-Social-Impact-Health-FINAL.pdf 2019 - 12.

Kruk ME, Gage AD, Arsenault C, Jordan K, Leslie HH, Roder-DeWan S, et al. High-quality health systems in the sustainable development goals era: Time for a revolution. Lancet Global Health. 2018; 6 (11):e1196-e1252. DOI: 10.1016/S2214-109X(18)30386-3. Epub 2018 Sep 5. Erratum in: Lancet Glob Health. Sep 18; Erratum in: Lancet Glob Health. 2018 Nov;6(11):e1162. Erratum in: Lancet Glob Health. 2021 Aug;9(8):e1067 - 13.

Mupedziswa R, Malenga T, Ntshirang PT. Standard of living, wellbeing and community development. The Case of Botswana. 2021; 2021 :65-79 DOI: 10.5772/ intechopen-97680 - 14.

Ahlin T, Nichter M, Pillai G. Health insurance in India: What do we know and why is ethnographic research needed. Anthropology & Medicine. 2016; 23 (1):102-124. DOI: 10.1080/13648470.2015.1135787 - 15.

Ministry of Healthy. Zambia National Health Strategic Plan 2022-2026. Lusaka: Zambia: Ministry of Health; 2022. Available from: https://www.nfnc.org.zm/download/2022-2026-strategic-plan-national-health-towards-attainment-of-quality-universal-health-coverage-through-decentralization/ - 16.

Kolié D, Van De Pas R, Codjia L, et al. Increasing the availability of health workers in rural sub-Saharan Africa: A scoping review of rural pipeline programmes. Human Resources for Health. 2023; 21 :20. DOI: 10.1186/s12960-023-00801-z - 17.

ISSA. Improving Health Insurance Systems. Geneva, Switzerland: Coverage and Service Quality; 2021. Available from: https://www.issa.int/analysis/improving-health-insurance-systems-coverage-and-service-quality - 18.

Katsuma Y. Global Health diplomacy to combat communicable diseases and to promote universal health coverage in achieving the sustainable development goal 3. In: Urata S, Kuroda K, Tonegawa Y, editors. Sustainable Development Disciplines for Humanity. Sustainable Development Goals Series. Singapore: Springer; 2023. DOI: 10.1007/978-981-19-4859-6_2 - 19.

Cieza A, Causey K, Kamenov K, Hanson SW, Chatterji S, Vos T. Global estimates of the need for rehabilitation based on the Global Burden of Disease study 2019: a systematic analysis for the Global Burden of Disease Study 2019. The Lancet. 19 Dec 2020; 396 (10267):2006-17. pp 1-12 DOI: 10.1016/S0140-6736(20)32340-0 - 20.

Nunn R, Parsons J, Shambaugh J. A dozen facts about the economics of the US health-care system. The Hamilton Project, Economic Facts. Mar 2020 10.1775. NW, Washington DC: Massachusetts Ave; 2003; 6 (202):797-6279. Available from:https://www.brookings.edu/wp-content/uploads/2020/03/HealthCare_Facts_WEB_FINAL.pdf - 21.

World Health Organization. Everybody business: strengthening health systems to improve health outcomes: WHO’s framework for action. 2007. Geneva, Switzerland: WHO; 2017.Available from: http://www.who.int/healthsystems/strategy/everybodys_business.pdf - 22.

Hussey P, Anderson. GF. Health Policy and Management. Baltimore, MD: John Hopkins University; 2003. DOI: 10.1016/S0168-8510(03)00050-2 - 23.

Preda A, Popescu M, Drigă I. The impact of covid-19 on global insurance market. InMATEC Web of Conferences EDP Sciences. 2021; 342 :08012. doi: 10.1051/matecconf/202134208012 - 24.

Bambra C. Cash versus services: The decommodification of cash benefits and health care services. Journal of Social Policy. 2005; 34 :195-213 - 25.

Mulenga J, Mulenga MC, Musonda K, Phiri C. Examining gender differentials and determinants of private health insurance coverage in Zambia. BMC Health Services Research. 2021; 21 (1):1-11 - 26.

Kim DS. Introduction: Health of the health care system in Korea. Social Work in Public Health. 2010; 25 :127-141 - 27.

Kim KS, Lee YJ. Developments and general features of national health insurance in Korea. Social Work in Public Health. 2010; 25 :142-157 - 28.

Sohn M, Jung M. Effects of public and private health insurance on medical service utilization in the National Health Insurance System: National panel study in the Republic of Korea. BMC Health Services Research. 2016; 16 :503. DOI: 10.1186/s12913-016-1746-2 - 29.

AbAbel-Smith B, Rawal P. Can the poor afford ‘free’ health services? A case study of Tanzania. Health Policy and Planning. 1 Dec 1992; 7 (4):329-41. Available from: doi: /10.1093/heapol/7.4.329 - 30.

Leu RE, Rutten FF, Brouwer W, Matter P, Rütschi C. The Swiss and Dutch health insurance systems: universal coverage and regulated competitive insurance markets. The Commonwealth Fund. Jan 2009; 104 :1-40. Available from:https://search.issuelab.org/resources/11352/11352.pdf - 31.

Basaza R, Kyasiimire EP, Namyalo PK, Kawooya A, Nnamulondo P, Alier KP. Willingness to pay for community health insurance among taxi drivers in Kampala City, Uganda: A contingent evaluation. Risk Management and Healthcare Policy. 2019; 12 :133-143. DOI: 10.2147/RMHP.S18487 - 32.

VWS (Ministry of Health, Welfare and Sport). Health Insurance in the Netherlands: The New Health Insurance System from 2006. The Hague: VWS; 2006 - 33.

Donev DM. Health insurance system in the Republic of Macedonia. Croatian Medical Journal. 1999; 40 (2) - 34.

Witter S, Garshong B. Something old or something new? Social health insurance in Ghana. BMC International Health Human Rights. 2009; 9 :20 - 35.

Kaonga O, Masiye F, Kirgi M. How viable is social health insurance for financing health in Zambia? Results from a National Willingness to Pay Survey. 2022; 2022 . DOI: 10.1016/j.socscimed.2022.115063 - 36.

Hanson E et al. The Lancet Global Health Commission on financing primary health care: Putting people at the Centre. 2022. 10.1016/S2214-109X(22)00005-5 - 37.

Siankwilimba E, Hiddlestone-Mumford J, et al. COVID-19 and the sustainability of agricultural extension models. International Journal of Applied Chemical and Biological Sciences. 2022; 3 (1):120. Available from:https://identifier.visnav.in/1.0001/ijacbs-21l-05003/ - 38.

Olugbenga EO. Workable social health insurance systems in sub-Saharan Africa: Insights from four countries. Africa Development. 2017; 42 (1):147-175 - 39.

Atte F. The moral challenges of health care providers brain drain phenomenon. Clinical Ethics. 2021; 16 (2):67-73 - 40.

Kaseje D. Health care in Africa: Challenges, opportunities and an. 2006 - 41.

Mordi DO, Eghan K, Rankin J. The impact of Ghana's National Health Insurance Scheme median pharmaceutical pricing methodology and reimbursement policy on the pharmaceutical system. Journal of Pharma Policy and Practise. 2015; 8 (Suppl. 1):P5. DOI: 10.1186/2052-3211-8-S1-P5 - 42.

Boateng D, Awunyor-Vitor D. Health insurance in Ghana: Evaluation of policy holders’ perceptions and factors influencing policy renewal in the Volta region. International Journal for Equity in Health. 2013; 12 :50. DOI: 10.1186/1475-9276-12-50 - 43.

Carrin G, Doetinchem O, Kirigia J, Mathauer I, Musango L. Social health insurance: How feasible is its expansion in the African region?. Dev issues. 2008. Available from: http://www.iss.nl/layout/set/print/content/view/full/12939 - 44.

Lépine A, Lagarde M, Le Nestour A. How effective and fair is user fee removal? Evidence from Zambia using a pooled synthetic control. Health Economics. 2018; 27 (2018):493-508 - 45.

Afriyie DO, Masiye F, Tediosi F, Fink G. Confidence in the health system and health insurance enrollment among the informal sector population in Lusaka, Zambia. Social Science & Medicine. 2023; 321 :115750 - 46.

Government of Zambia. The National Health Insurance Act Lusaka (2018) [No. 2 of 2018]. 2018 - 47.

Government of Zambia. The National Health Insurance Act Lusaka (2018) [No. 2 of 2018]. Lusaka, Zambia: Ministry of Justice; 2018. Available from: https://zambialii.org/akn/zm/act/2018/2/eng@2018-04-11/source.pdf - 48.

National Health Insurance Management Authority. Lusaka, Zambia: Accreditation of Healthcare Providers NHIMA; 2022. Available from: https://www.nhima.co.zm/health-care-providers - 49.

Venkateswaran S, Slaria S, Mukherjee S. Political motivation as a key driver for universal health coverage. Frontiers in Public Health. 2022; 2022 :3707 - 50.

Parson J, Ryan N. A dozen facts about the economics of the U.S. health care system. 2019 - 51.

Kraft ME, Furlong SR. Public Policy: Politics, Analysis, and Alternatives. 7th Edition. USA, Green Bay: University of Wisconsin, Cq Press; 2019:544. Available from: https://us.sagepub.com/en-us/nam/public-policy/book259264 - 52.

Dewey J. The Public and its Problems. New York: Holt; 1927 - 53.

Green L, Ashton K, Bellis MA, Clemens T, Douglas M. ‘Health in all policies’—A key driver for health and well-being in a post-COVID-19 pandemic world. International Journal of Environmental Research and Public Health. 2021; 18 (18):9468 - 54.

Mwiinde AM, Siankwilimba E, Sakala M, Banda F, Michelo C. Climatic and environmental factors influencing COVID-19 transmission—An African perspective. Tropical Medicine and Infectious Disease. 2022; 7 (12):433 - 55.

Agyepong AI, Adjei S. Public social policy development and implementation: A case study of the Ghana National Health Insurance Scheme. Health Policy and Planning. 2008; 23 :150-160 - 56.

Schneider P. Trust in micro-health insurance: An exploratory study in Rwanda. Social Science Medicine. 2005; 61 :1430-1438 - 57.

Social protection and Public Finance management. New SP&PFM project launched in Zambia to extend social health insurance coverage to the poor and vulnerable. 2023. Available from: https://socialprotection-pfm.org/new-sppfm-project-launched-in-zambia-to-extend-social-health-insurance-coverage-to-the-poor-and-vulnerable/ - 58.

Rural Health Information Hub. US Department of Health and Human Services. 2022 - 59.

Rural Health Information Hub. US Department of Health and Human Services. 2022. Available from: https://www.ruralhealthinfo.org/ - 60.

Jaiswal J. Whose responsibility is it to dismantle medical mistrust? Future directions for researchers and health care providers. Behavioral Medicine. 2019; 45 (2):188-196 - 61.

Shrestha MV, Manandhar N, Dhimal M, Joshi SK. Awareness on social health insurance scheme among locals in Bhaktapur municipality. 2020 - 62.

Raphael D. Social Determinants of Health: Canadian Perspectives. USA: Canadian Scholars’ Press, University of NewYork; 2016:PP 648. ISBN-10: 1551308975, ISBN-13: 978-1551308975 - 63.

Rietkerk S. Feb 21, 2023 Internal/External Posting# HC01-23-02 Occupational Therapist–RISE Community Health Centre. 2023 - 64.

Ma M, Tian W, Kang J, Li Y, Xia Q , Wang N, et al. Does the medical insurance system play a real role in reducing catastrophic economic burden in elderly patients with cardiovascular disease in China? Implication for accurately targeting vulnerable characteristics. Globalization and Health. 2021; 17 :1-13 - 65.

Jung HW, Kwon YD, Noh JW. How public and private health insurance coverage mitigates catastrophic health expenditures in Republic of Korea. BMC Health Services Research. 2022; 22 (1):1-12 - 66.

Kirigia JM, Sambo LG, Nganda B, Mwabu GM, Chatora R, Mwase T. Determinants of health insurance ownership among south African women. BMC Health Services Research. 2005; 5 (1):1-10 - 67.

Spaan E, Mathijssen J, Tromp N, McBain F, Have AT, Baltussen R. The impact of health insurance in Africa and Asia: A systematic review. Bulletin of the World Health Organization. 2012; 90 :685-692