Open Access is an initiative that aims to make scientific research freely available to all. To date our community has made over 100 million downloads. It’s based on principles of collaboration, unobstructed discovery, and, most importantly, scientific progression. As PhD students, we found it difficult to access the research we needed, so we decided to create a new Open Access publisher that levels the playing field for scientists across the world. How? By making research easy to access, and puts the academic needs of the researchers before the business interests of publishers.

We are a community of more than 103,000 authors and editors from 3,291 institutions spanning 160 countries, including Nobel Prize winners and some of the world’s most-cited researchers. Publishing on IntechOpen allows authors to earn citations and find new collaborators, meaning more people see your work not only from your own field of study, but from other related fields too.

To purchase hard copies of this book, please contact the representative in India:

CBS Publishers & Distributors Pvt. Ltd.

www.cbspd.com

|

customercare@cbspd.com

This manuscript provides a detailed analysis of the current landscape of mandatory health insurance in Uzbekistan, aiming to offer valuable insights and inform future discussions on the topic. It explores the benefits, challenges, and implications of health insurance for individuals and the healthcare system as a whole. By incorporating perspectives from policymakers, healthcare providers, insurance companies, and the general public, this study examines the opportunities and limitations associated with health insurance coverage. Furthermore, it investigates the impact of health insurance on access to quality healthcare services, financial protection, and overall health outcomes. Case studies, policy frameworks, and empirical evidence evaluate the effectiveness of different health insurance models in addressing the unique needs and challenges faced by Uzbekistan’s population. Additionally, this manuscript identifies strategies for overcoming barriers and improving the affordability, accessibility, and inclusivity of health insurance programs. It offers a comprehensive overview of health insurance in Uzbekistan, contributing to existing literature on health policy and serving as a resource for policymakers and stakeholders involved in designing and implementing sustainable health insurance schemes. Ultimately, this research aims to enhance healthcare systems and ensure equitable access to healthcare services for all individuals in Uzbekistan.

Institute for Macroeconomic and Regional Studies under the Cabinet of Ministers of the Republic of Uzbekistan, Uzbekistan, Tashkent

*Address all correspondence to: iqboljon.odashev@gmail.com

1. Introduction

“Health is a state of complete physical, mental and social well-being, and not merely the absence of disease or infirmity”

World Health Organization.

In this manuscript, we embark on a journey into the multifaceted world of health insurance in Uzbekistan. Our aim is to shed light on its functioning and impact on individuals and society. Health insurance plays a crucial role in ensuring access to quality healthcare services and protecting the well-being and financial stability of individuals and families. As Uzbekistan rapidly develops as a country in Central Asia, the landscape of health insurance has undergone significant changes in recent years. According to the World Bank’s “Europe and Central Asia Economic Update” report, Uzbekistan’s GDP has experienced considerable growth, reaching 5.7% in 2022. This growth can be attributed to factors such as remittances, consumption, and exports. Projections indicate that this economic growth will continue to rise, reaching an anticipated 5.1% by the end of 2023. Supporting our narrative are statistical data from reliable sources. The World Bank reports a decrease in the infant mortality rate in Uzbekistan, from 19.196 deaths per 1000 live births in 2022 to 18.787 deaths per 1000 live births in 2023. Additionally, the World Health Organization highlights an increase in life expectancy at birth in Uzbekistan, rising from 66 years in 2000 to 73 years in 2019. UNICEF reports consistently high immunization coverage for children in Uzbekistan, with over 90% of children receiving vaccinations against common diseases such as measles, mumps, and rubella. Moreover, the Asian Development Bank notes significant progress in access to improved sanitation facilities in Uzbekistan, increasing from 67% in 2000 to 94% in 2018. Lastly, the WHO acknowledges a decline in the maternal mortality ratio in Uzbekistan, from 41 deaths per 100,000 live births in 2000 to 29 deaths per 100,000 live births in 2017. These positive trends in health indicators are a testament to the well-implemented reforms undertaken by the Republic of Uzbekistan. Our manuscript aims to unravel the complexities surrounding this essential aspect of Uzbekistan’s healthcare system. As your helpful and patient assistant, I will guide you through the pages of this manuscript, exploring the perspectives of various stakeholders. These include policymakers, healthcare providers, insurers, and most importantly, the individuals who rely on mandatory health insurance for their medical needs. Through the examination of these diverse viewpoints, we seek to develop a comprehensive understanding of the current state of health insurance in Uzbekistan and identify areas for improvement. During our exploration, we will delve into topics such as the evolution of health insurance in Uzbekistan, examining its benefits and challenges. We will also analyze the government’s role in shaping health insurance policies, evaluate the influence of private insurers, and showcase the experiences of individuals who have utilized health insurance services. Our goal is to provide you with an insightful analysis that not only highlights the strengths and weaknesses of the system but also offers recommendations for enhancing the accessibility, affordability, and effectiveness of health insurance in Uzbekistan. By acknowledging the efforts made by policymakers, healthcare providers, and other stakeholders in achieving these significant improvements, we can further appreciate the importance of continued reforms and identify areas where further progress can be made to ensure a comprehensive and inclusive healthcare system for all Uzbekistan’s citizens. Our collective efforts aim to contribute to the ongoing discourse surrounding healthcare policy and its implications for the well-being of the Uzbek population. Together, let us explore the advantages and challenges of mandatory health insurance in Uzbekistan, with the ultimate aim of fostering a robust and equitable healthcare system for all.

Health insurance holds a crucial role in providing healthcare services and financial protection for individuals and families. As healthcare systems continue to evolve globally, understanding the complexities and implications of health insurance is vital for policymakers, healthcare providers, and patients. The objective of this literature review is to analyze and synthesize existing research on various aspects of health insurance, including its impact on access to care, cost containment, and quality of healthcare.

Several Uzbek scientists have investigated health insurance perspectives in the Uzbekistan insurance market. In the following Table 1, we can review how Uzbek scientists have investigated mandatory health insurance and its perspectives:

Researchers name

Year

Scientific findings and directions

1

Abdullaev, A.

2017

He examines the challenges and opportunities for health insurance in Uzbekistan, providing insights into the current state of the system and potential areas for improvement [1]

2

Khamraev, A., Karimov, S.

2018

They conduct an analysis of factors influencing the effectiveness of health insurance in Uzbekistan, offering valuable insights for policy-making and system improvement [2]

3

Mansurov, A., Ahmadjonov, I., Foezli, R.

2020

They analyze health insurance schemes in Uzbekistan, drawing lessons and providing recommendations to optimize their functioning and improve healthcare outcomes [3]

4

Norkulova, M., Karshibaev, A., Khalmirzaeva, D.

2019

They investigate the role of health insurance in improving healthcare access in rural areas of Uzbekistan, shedding light on the potential impact of insurance schemes on underserved populations [4]

5

Sharapova, M., Kasymova, M.

2019

They examine the implementation of public-private partnership in health insurance in Uzbekistan, assessing its effectiveness and discussing potential benefits and challenges [5].

Table 1.

The role of Uzbek scientists in investigating mandatory health insurance.

Based on the findings of the scientific research conducted by Uzbek researchers on mandatory health insurance, the following conclusions can be drawn:

The investigations carried out by Uzbek scientists on mandatory health insurance in Uzbekistan explore the challenges and opportunities associated with health insurance in the country. They offer valuable insights into the current state of the system and identify potential areas for improvement. The analysis of factors influencing the effectiveness of health insurance provides valuable information for policymaking and system enhancement. By analyzing health insurance schemes in the country, the researchers draw important lessons and provide recommendations to optimize their functioning and improve healthcare outcomes. The investigation into the role of health insurance in improving healthcare access in rural areas of Uzbekistan sheds light on the potential impact of insurance schemes on underserved populations. Furthermore, the examination of the implementation of public-private partnerships in health insurance assesses their effectiveness and discusses potential benefits and challenges. In summary, the scientific research conducted by Uzbek scholars on mandatory health insurance demonstrates their commitment to understanding and improving the healthcare insurance system in Uzbekistan. The research provides valuable insights that can serve as a basis for policy development and system reform to enhance healthcare outcomes for the entire population.

Moreover, it is necessary to emphasize the close cooperation of the WHO with the Ministry of Health of the Republic of Uzbekistan in a number of important issues in improving health care. In particular, the significant contribution of WHO experts is required in the development of the Concept for the Development of the Health Care System of the Republic of Uzbekistan for 2019-2025, which was approved by the Decree of the President of the Republic of Uzbekistan on December 7, 2018, “On Comprehensive Measures to Further Improve the Health Care System of the Republic of Uzbekistan.” Through the assistance of international experts, measures are being taken to improve the financial support of health care, establish mandatory medical insurance and introduce an electronic health care system, promote a healthy lifestyle and healthy eating habits, as well as combat non-communicable and communicable diseases [6]. Hussain [7] presents a case study of the development of health insurance in Central Asia, focusing on Uzbekistan and identifying key factors that shaped its implementation and effectiveness. Hussain is affiliated with the Institute of Health Policy and Management at the University of Central Asia [7].

Furthermore, other researchers worldwide have also contributed to the study of health insurance systems. Let’s review their scientific results, insights and achievements by the following Table 2:

Researchers name

Year

Scientific findings and directions

1

Wendt, C.

2019

They propose a social health insurance model for Europe, offering a framework that could enhance healthcare coverage and accessibility across the continent [8]

2

Anderson, G.

2003

They highlight the impact of pricing on healthcare costs in the United States compared to other countries, emphasizing the need for price regulation and cost management strategies [9].

3

Bärnighausen, T., Sauerborn, R.

2002

They analyze the lessons that middle- and low-income countries can learn from the German health insurance system, which has operated for over a century [10].

4

Carrin, G., James, C.

2005

They provide an economic perspective on revolving funds for health, exploring their potential as a financing mechanism to improve access to healthcare services [11].

5

Kutzin, J.

2013

They discusses concepts and implications of health financing for universal coverage and health system performance, highlighting the importance of well-designed financial schemes [12].

6

Kwon, S.

2015

They provide an international perspective on health insurance reform in South Korea, examining its implications and lessons that can be learned by other countries [13].

7

Liu, G.G.

2016

They present a comprehensive study on national spending on health in different countries, projecting trends between 2013 and 2040, offering valuable insights for policy planning and resource allocation [14].

8

McIntyre, D., Meheus, F., Røttingen, J.A.

2017

They explore the ideal level of domestic government health expenditure required to achieve universal health coverage, considering various economic factors and policy implications [15].

9

Moreno-Serra, R., Millett, C., Smith, P.C.

2011

They propose improved measurements for financial protection in health, aiming to strengthen health systems and ensure equitable access to healthcare services [16].

10

Musgrove, P.

1999

He examines financial mechanisms for integrating funds for health, highlighting the importance of coordinated financing approaches to strengthen healthcare delivery and resource allocation [17].

11

Savedoff, W.D., de Ferranti, D., Smith, A.L.

2019

They present the final report of the Transitions in Health Financing project, offering insights and recommendations for countries transitioning towards universal health coverage [18].

12

Scheil-Adlung, X.

2018

He reviews definitions, indicators, and pathways towards achieving universal health coverage, providing a comprehensive understanding of the concept and strategies for its realization [19].

Table 2.

Examining mandatory health insurance worldwide: Insights from international scientists.

In conclusion, these research studies offer valuable insights into medical insurance and its impact on healthcare systems. The suggested social health insurance model for Europe presents potential enhancements in coverage and accessibility. The researchers emphasize the importance of regulating prices to control healthcare costs, with particular attention drawn to the situation in the United States. Lessons from the German system can be applied to middle- and low-income countries to strengthen their healthcare insurance systems. The studies also explore the potential advantages of revolving funds for health as a financing mechanism to improve access to healthcare services. Additionally, the researchers delve into various concepts and implications of health financing aimed at achieving universal coverage and optimizing system performance. The analysis of health insurance reform in South Korea provides valuable insights that may be relevant to other countries. Moreover, the comprehensive study on national health spending offers significant data and insights for policymakers, highlighting the crucial role of reaching an optimal level of domestic government health expenditure while considering economic factors. Such action is vital for achieving universal health coverage. The researchers propose improved measurements for financial protection in health and stress the importance of strengthening health systems to ensure fair access to healthcare services. They also underscore the need for coordinated financing approaches to enhance healthcare delivery and resource allocation. The final report of the Transitions in Health Financing project provides further recommendations and guidance for countries transitioning towards universal health coverage. The review of definitions, indicators, and pathways for achieving universal coverage enhances our understanding of this concept and provides strategies for its attainment. Overall, this collection of research significantly contributes to the existing knowledge on health insurance and offers valuable insights for policymakers, healthcare providers, and researchers worldwide.

In Uzbekistan, also, Dr. Mukhammadjon Rasulov, a professor at the Tashkent Medical Academy, specializes in health economics and health insurance systems. His research examines the effectiveness and efficiency of health insurance schemes in Uzbekistan, as well as their impact on population health outcomes. Dr. Rasulov’s work has published in various scientific journals and has informed policy decisions related to health insurance in Uzbekistan.

Based on the scientific research mentioned above, as well as my experience as a general financial manager at Insurance Company Limited liability company “Alfa Invest” from 2008 to 2016 and a three-month practical internship at “Uzbekinvest” Export-Import Insurance Company, “Uzagrosugurta” Joint Stock Company, and the Insurance Market Development Agency under the Ministry of Finance and Economy of the Republic of Uzbekistan in 2017, directed by the Academy of Public Administration under the President of the Republic of Uzbekistan, I conducted an investigation into the history and current implementation of medical insurance globally and in Uzbekistan. My research aimed to identify solutions to address the challenges and potential of medical insurance in Uzbekistan. To achieve this, I conducted a SWOT analysis of medical insurance in Central Asian countries, presented methods for implementing medical insurance based on existing models, and outlined the stages of implementing medical insurance in the Republic of Uzbekistan.

3. A historical overview of health insurance: Global and Uzbekistan at a glance

The concept of health insurance can indeed be traced back to ancient times when mutual aid and assistance were practiced. However, modern health insurance as we know it today emerged in the late nineteenth century and has evolved significantly over time. An interesting historical academic aspect to consider is the development of health insurance in Germany. In the late nineteenth century, German Chancellor Otto von Bismarck introduced the pioneering social insurance program, known as the “Sickness Insurance Law” of 1883. This legislation marked the first government-led efforts to provide health insurance to the working class. The law mandated that certain workers contribute a portion of their wages to a sickness fund, while employers also made contributions. In return, these workers received medical coverage, sick pay, and access to healthcare services. This system laid the groundwork for the development of health insurance systems in other countries around the world. Returning to the United States, it’s fascinating to note that the roots of health insurance can be found in response to workplace accidents during the era of industrialization. Mutual benefit associations and fraternal organizations emerged in the late 1800s, offering financial aid to members during times of illness or injury. These early forms of health insurance relied on member contributions to cover medical expenses. The Franklin Health Assurance Company of Massachusetts holds the distinction of introducing the first official health insurance policy specifically covering injuries from train or steamboat accidents in 1850. This was followed by the establishment of other insurance companies that primarily focused on accident and injury coverage rather than general healthcare. Moving into the early twentieth century, the concept of employer-sponsored health insurance gained prominence. In 1929, a group of teachers in Texas created Blue Cross, a prepaid hospitalization plan that formed the foundation for modern health insurance. Blue Cross expanded nationwide, and in 1939, Blue Shield was created to cover physician services. Eventually, Blue Cross and Blue Shield merged to form the association we know today. Government involvement in healthcare took a significant step forward with the Social Security Act of 1935. This act laid the foundation for the introduction of Medicare and Medicaid in 1965, which provided healthcare coverage for elderly individuals, low-income individuals, and those with disabilities. These programs aimed to ensure access to necessary medical services for vulnerable populations. Over time, various reforms have shaped the healthcare industry. The Health Maintenance Organization (HMO) Act of 1973, for example, promoted cost-effective healthcare delivery through HMOs. These organizations gained popularity as a response to rising healthcare costs. Managed care organizations, such as Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs), became prominent in the healthcare industry during this period. In recent times, the Affordable Care Act (ACA), signed into law in 2010, aimed to increase access to health insurance and implement significant reforms in the industry. It introduced provisions such as guaranteed coverage for pre-existing conditions, the establishment of health insurance marketplaces, and subsidies to make coverage more affordable for individuals and families. Throughout history, health insurance has continuously evolved to meet changing needs and challenges in healthcare. Today, it remains a vital component of modern healthcare systems, offering financial protection and access to necessary medical services.

Now, let us explore the historical bases of the different models of medical insurance that have emerged around the world:

Socialized medicine: In the early twentieth century, various countries began adopting socialized medicine, where healthcare services are provided and financed by the government. Examples of countries with socialized medicine include the United Kingdom’s National Health Service (NHS), Canada’s Medicare system, and Sweden’s comprehensive healthcare system [20]. Socialized medicine aims to ensure equitable access to healthcare services for all citizens, regardless of their ability to pay [21].

Compulsory health insurance: Compulsory health insurance schemes require individuals to contribute a portion of their income towards healthcare coverage [22]. This model was implemented in Germany in the late nineteenth century, with the passing of the Health Insurance Act in 1883 [23]. Compulsory health insurance provides coverage for both employees and self-employed individuals, ensuring universal access to healthcare services [23].

Managed care: Managed care refers to a system where healthcare providers and insurers coordinate to deliver cost-effective healthcare while maintaining quality [24]. This model gained popularity in the United States in the late twentieth century as a response to rising healthcare costs [25]. Managed care organizations, such as Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs), became prominent in the healthcare industry [25].

Market-based health insurance: Market-based health insurance relies on private insurers competing in a market to offer coverage options to individuals [26]. It allows individuals to choose from a range of insurance plans that suit their needs and preferences [26]. Countries like Switzerland, the Netherlands, and Singapore have implemented market-based health insurance systems.

These various models of medical insurance reflect different approaches to financing and delivering healthcare services, each with its own advantages and limitations. The choice of model often depends on a country’s socio-political context and healthcare system goals. The conclusion of the historical overview of medical insurance worldwide provides a comprehensive overview of the history of health insurance, highlighting key milestones and developments. It is important to recognize that health insurance has evolved over time to meet the changing needs and challenges in healthcare. It also introduces different models of medical insurance that have emerged around the world, including socialized medicine, compulsory health insurance, managed care, and market-based health insurance. These models reflect different approaches to financing and delivering healthcare services, with each having its own advantages and limitations. The choice of model often depends on a country’s socio-political context and healthcare system goals.

The history of health insurance extends beyond the international scope, including Uzbekistan. Health insurance in Uzbekistan has its roots in the Soviet era when the healthcare system was primarily state-funded and centralized. During this time, the government provided universal healthcare coverage to all citizens. Following the dissolution of the Soviet Union, Uzbekistan underwent a transition towards a market-oriented economy. As a result, the healthcare system also underwent significant changes. The introduction of private medical institutions and the emergence of a private sector led to the need for health insurance options beyond the state-provided coverage. In the early 2000s, efforts were made to develop health insurance programs in Uzbekistan to complement the existing state-funded system. The government introduced compulsory social health insurance for certain population groups, such as public sector employees and workers in selected industries. These programs aimed to provide additional financial protection and access to healthcare services, particularly for those who sought care outside of the state-funded system. Over the years, the health insurance landscape in Uzbekistan has continued to evolve. The government has introduced various reforms and initiatives to expand health insurance coverage, including the establishment of voluntary health insurance programs for individuals and families. Today, health insurance in Uzbekistan plays an important role in providing access to healthcare services and ensuring financial protection for the population. It continues to be an area of focus for the government as it works towards enhancing the overall healthcare system and addressing the healthcare needs of its citizens.

It is impossible not to mention the great encyclopedic scientist, philosopher, and medical care provider, Ibn Sina. Ibn Sina, also known as Avicenna, was a Persian polymath who lived during the Islamic Golden Age in the tenth and eleventh centuries. His contributions to medicine were groundbreaking and have had a lasting impact. His full name was Hussain ibn Abdullah ibn Hassan ibn Ali ibn Sina. He was born around 980 in Afshana, near Bukhara, which was his mother’s hometown, in Greater Khorasan, to a Persian family. One of Ibn Sina’s most significant contributions was his renowned medical encyclopedia, “The Canon of Medicine.” This work became a central authority in the field of medicine for several centuries, both in the Islamic world and Europe. It covered various topics, including anatomy, physiology, pathology, and pharmacology. The Canon of Medicine served as a comprehensive guide to medical knowledge and practice at the time and greatly influenced medical education worldwide. Ibn Sina also made important advancements in understanding contagious diseases. He recognized that some diseases, like tuberculosis, are spread through the air, while others, like skin diseases, are spread through direct contact. His insights on contagion helped shape the field of epidemiology and laid the foundation for future developments in disease prevention and control. Additionally, Ibn Sina emphasized the importance of a holistic approach to healthcare, taking into account not only the physical aspects but also the psychological and spiritual dimensions of the patient. This approach, known as “holistic medicine,” is increasingly recognized and valued in modern medicine. Overall, Ibn Sina’s contributions to medicine were vast and diverse. His work in medical research, education, and patient care continues to be revered, making him one of the most influential figures in the history of medicine.

4. A comprehensive look at health insurance in present-day Uzbekistan

In recent years, the government of Uzbekistan has made significant efforts to improve the healthcare system and ensure access to quality healthcare services for all citizens. One crucial aspect of these reforms is the implementation of a comprehensive health insurance system. Health insurance has been in place in Uzbekistan since 1994, following the country’s independence from the Soviet Union. The government established a system of state mandatory health insurance to provide basic medical care for all citizens, which was later expanded to include additional benefits such as dental care and maternity services.

In 2019, Uzbekistan accepted the Law of the Republic of Uzbekistan on Compulsory Employer’s Liability Insurance, which introduced a new health insurance law aiming to improve the quality of healthcare and increase access to medical services. The law requires all employers to provide health insurance coverage for their employees, while individuals are also required to purchase health insurance if they are not covered by an employer.

Overall, the development and implementation of health insurance systems have been driven by the need to provide access to healthcare for as many people as possible, regardless of their financial situation or employment status. Currently, the government is in the process of implementing mandatory health insurance into practice. Through mandatory health insurance, every citizen of Uzbekistan can access a high profile of guaranteed medical services. The implementation process has been successfully realized in the Sirdarya region, and efforts are now underway to transfer the medical system of Tashkent city into the Government mandatory health insurance process.

The Ministry of Health manages the healthcare system, and there are also private healthcare providers available in Uzbekistan. In recent years, the government has made significant investments in the healthcare system, including the construction of new hospitals and clinics, as well as the development of new medical technologies and pharmaceuticals. However, there are still some challenges within the healthcare system, including limited access to specialized care, shortages of medical personnel and equipment in certain areas, and outdated infrastructure in some medical facilities. Despite these challenges, the healthcare system of Uzbekistan is continuously improving and has made significant strides in recent years to improve the health outcomes of its citizens.

The healthcare system in Uzbekistan is state-funded and provides free medical care to all citizens. However, the level of care can vary, and many people choose to take out private health insurance to supplement their government-funded healthcare. Private health insurance is not yet widespread in Uzbekistan but is becoming increasingly popular. Many international insurance companies offer comprehensive health insurance policies for individuals and families living in Uzbekistan. These policies typically cover a range of medical expenses, including hospital treatments, emergency medical care, and outpatient services. The cost of health insurance varies depending on the level of coverage required and the insurer. In general, premiums are relatively affordable and well worth the peace of mind that comes with knowing that you are covered in an emergency.

It should be noted that there are certain limitations to private health insurance in Uzbekistan. Some insurers may place restrictions on pre-existing conditions, and certain treatments and procedures may not be covered. Additionally, there may be deductibles or co-payments required for some types of treatment. Overall, private health insurance is a wise investment for those who want to ensure they have access to quality healthcare in Uzbekistan. As the country’s healthcare system continues to develop, we can expect to see more insurance products become available to meet the growing demand.

5. A statistical overview of the health system in Uzbekistan

Let us review some main health indicators of Uzbekistan based on the numbers provided by Statistics Agency under the President of the Republic of Uzbekistan. Health indicators play a vital role in assessing the overall well-being of a population and providing insights into the efficiency and effectiveness of a country’s healthcare system. By examining and analyzing the main health indicators in Uzbekistan, including the number of hospitals, availability of hospital beds, access to specialized clinics, and the presence of healthcare professionals, we can gain valuable insights into the strengths and weaknesses of the healthcare system, identify areas for improvement, and ultimately enhance the quality of healthcare services.

Based on the data presented in the Table 3, an analysis of the main health indicators in Uzbekistan reveals the following trends:

Indicators

2000

2005

2010

2015

2021

Number of hospitals

1162

1149

1158

1071

1281

Number of hospital beds, thousand

138.6

142.4

139.6

129.7

165.5

Population per hospital bed

179

185

209

243

213

Number of ambulatory polyclinics

4847

5507

5993

6220

6676

The capacity of outpatient clinics, visits per shift, thousand

391.5

401.7

422.5

407.0

461.3

Number of obstetrics and gynecology offices

2074

2370

2857

2752

1699

Number of children’s polyclinics (departments)

2519

2417

2341

1997

535

Number of doctors of all specialties, thousand

81.5

76.5

79.9

83.4

95.6

Population per doctor

304

344

356

379

369

Number of nurses, thousand

259.7

271.0

310.2

336.4

372.5

Population per average medical worker

96

97

92

94

95

Table 3.

Year-end assessment: Key health indicators of Uzbekistan.

The number of hospitals in Uzbekistan has increased from 1162 in 2000 to 1281 in 2021, indicating positive progress in providing accessible healthcare facilities for the population. The availability of hospital beds has fluctuated over the years, reaching a peak of 142.4 thousand in 2005 before rising to 165.5 thousand in 2021. However, the ratio of population per hospital bed has shown an upward trend, increasing from 179 in 2000 to 243 in 2015 but slightly decreasing to 213 in 2021. This highlights the importance of ensuring sufficient hospital bed availability to meet the healthcare needs of the population.

The number of ambulatory polyclinics has steadily risen from 4847 in 2000 to 6676 in 2021, indicating better access to outpatient care and preventive services, contributing to a healthier population. However, there has been a decrease in the number of specialized clinics, particularly in obstetrics and gynecology. Access to specialized clinics, such as obstetrics and gynecology, is crucial for addressing the specific healthcare needs of women.

Ensuring adequate access to healthcare services for children is crucial for their overall well-being and development. However, there has been a decline in the number of children’s polyclinics in Uzbekistan, decreasing from 2519 in 2000 to only 535 in 2021. This reduction can be attributed to the extensive healthcare reforms being implemented in the country. One significant aspect of these reforms is the Presidential Decree No. PD 6110, issued on November 12, 2020, titled “Measures to implement new mechanisms in the activities of primary medical and sanitary care institutions and further enhancing the effectiveness of reforms in the healthcare system.” This decree plays a crucial role in establishing a modern system for providing primary medical and sanitary care, preventing and early detecting diseases, preparing qualified medical personnel, and introducing new management approaches.

According to the decree, a schedule has been approved for the creation of family doctor practices and family polyclinics from 2021 to 2023, which includes children’s polyclinics. Additionally, the following will be established: 315 family doctor practices, with 100 in 2021, 105 in 2022, and 110 in 2023; 52 family polyclinics in rural areas, with 17 in 2021, 18 in 2022, and 17 in 2023; and 33 family polyclinics in cities, with 7 in 2021, 13 in 2022, and 13 in 2023. The funding sources for the establishment of these additional family doctor practices and family polyclinics include funds from the state budget of the Republic of Karakalpakstan, local budgets of regions and the city of Tashkent, charitable donations from legal and natural persons, and other sources not prohibited by legislation.

The availability of healthcare professionals has witnessed positive growth, with the number of doctors increasing from 81.5 thousand in 2000 to 95.6 thousand in 2021. However, the ratio of population per doctor has generally risen during the same period, suggesting potential challenges in accessing healthcare services. Similarly, the number of nursing staff has increased from 259.7 thousand in 2000 to 372.5 thousand in 2021, contributing to enhanced healthcare delivery.

In summary, while Uzbekistan has made improvements in certain areas of the healthcare system such as the number of hospitals, ambulatory polyclinics, and the healthcare workforce, challenges remain in terms of hospital bed availability, access to specialized clinics, and the ratio of population to healthcare professionals. Addressing these issues is crucial to ensure better healthcare provision and promote a healthier lifestyle for the population.

Table 4 provides detailed information on the number of hospitals in different regions of Uzbekistan between 2016 and 2021. It effectively highlights the transformations and patterns observed within the country’s healthcare infrastructure. To exemplify, in 2016, the Republic of Karakalpakstan had a total of 42 hospitals. This figure slightly declined to 41 in 2017 before gradually increasing each subsequent year, ultimately reaching 58 hospitals in 2021. This upward trend demonstrates a consistent dedication to enhancing access to healthcare services within the region. Similarly, the Andijan region began with 136 hospitals in 2016, maintaining that exact number in 2017. Subsequently, there was an incremental annual growth, culminating in 157 hospitals by 2021. Consequently, this indicates a steady expansion of healthcare facilities in Andijan. In the case of the Samarkand region, it initially possessed 89 hospitals in 2016. Over time, this number experienced fluctuations, yet ultimately surged to 120 hospitals by 2021. Such findings suggest ongoing investments in healthcare infrastructure aimed at accommodating the needs of the local population. Furthermore, the Khorezm region commenced with 38 hospitals in 2016. Gradually, the number of hospitals consistently rose each year, eventually reaching 72 in 2021. This significant increase reflects substantial improvements in the region’s healthcare infrastructure. Conversely, Tashkent city consistently maintained the highest number of hospitals throughout the designated period. Starting with 135 hospitals in 2016, the figure peaked at 161 in 2017 and subsequently decreased to 153 hospitals by 2021. Regardless of these minor fluctuations, the healthcare infrastructure in Tashkent city continues to deliver extensive services to the local population. Overall, this data clearly indicates the nation’s endeavors to enhance healthcare infrastructure and improve accessibility across various regions of Uzbekistan. Although certain areas witnessed temporary fluctuations in the number of hospitals, the general trend shows a positive increase in healthcare facilities. These efforts reflect the government’s unwavering commitment to providing its citizens with high-quality healthcare services.

Analyzing the data provided on medical personnel by profession in the Republic of Uzbekistan from 2007 to 2021, we can observe several trends and changes (Table 5), which are next explained:

Total number of doctors: The total number of doctors in Uzbekistan has been gradually increasing over the years. From 2007 to 2021, there has been continuous growth in the number of doctors, reaching a peak of 95.6 thousand in 2021. This suggests that Uzbekistan has been making efforts to expand its healthcare workforce and improve access to medical services for its population.

Doctors by specialization: Within the medical profession, different specializations have varying numbers of doctors. The therapeutic profile, which includes physicians in physical therapy and sports, experienced fluctuations over the years but saw a slight increase in recent years, reaching 23.1 thousand in 2021. The number of doctors in the surgical profile has also shown a gradual increase from 9.3 thousand in 2007 to 11.8 thousand in 2021. Obstetrician-gynecologists, pediatricians, ophthalmologists, otolaryngologists, phthisiatricians, neuropathologists, psychiatrists, narcologists, dermato-venereologists, dentists, radiologists, and oncologists have shown varying levels of stability or slight fluctuations in their respective numbers over the years.

Gender distribution: The data also reveals the proportion of male and female doctors in Uzbekistan. On average, the percentage of women among the total number of doctors has remained relatively stable at around 41–45% throughout the years.

Nursing staff: The number of nursing staff in Uzbekistan has shown a consistent increase over the years, with a steady rise from 280.3 thousand in 2007 to 372.5 thousand in 2021. This indicates a focus on strengthening the nursing workforce to support healthcare services and improve patient care.

Medical personnel by profession

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Doctors total

79.9

81.7

81.3

81.7

82.0

83.4

84.1

85.4

89.8

91.9

93.3

95.6

therapeutic profile

22.3

22.3

25.0

26.9

28.0

28.4

29.2

28.9

19.2

19.4

20.8

23.1

including physicians in physical therapy and sports

0.1

0.1

0.1

0.1

0.1

0.1

0.1

0.1

0.1

0.1

0.1

0.1

surgical profile

9.9

10.1

10.3

10.5

11.1

11.4

10.9

11.0

11.3

11.6

11.3

11.8

obstetrician-gynecologists

6.0

6.1

5.8

5.9

5.7

5.8

5.7

5.6

5.7

5.7

5.4

5.1

pediatricians

9.7

9.1

8.8

8.1

7.5

7.0

6.5

6.0

6.1

6.1

5.2

5.0

ophthalmologists

1.2

1.2

1.3

1.5

1.6

1.6

1.7

1.6

1.8

1.8

1.6

1.3

otolaryngologists

1.3

1.4

1.3

1.7

1.7

1.8

1.8

1.8

1.9

2.0

1.8

1.7

phthisiatricians

1.1

1.1

1.2

1.2

1.2

1.2

1.2

1.2

1.2

1.2

1.2

1.3

neuropathologists

2.3

2.3

2.0

2.5

2.6

2.7

2.7

2.7

2.9

3.0

2.8

2.7

psychiatrists

1.0

1.0

1.1

1.0

1.1

1.1

1.1

1.1

1.3

1.1

1.0

1.0

narcologists

0.4

0.4

0.4

0.4

0.5

0.4

0.5

0.5

0.5

0.4

0.4

0.4

dermato-venereologists

1.1

1.2

1.2

1.2

1.2

1.2

1.2

1.1

1.3

1.3

1.4

1.3

dentists

5.8

7.2

7.0

7.6

7.1

7.4

7.6

7.7

8.5

8.7

5.6

6.2

sanitary-epidemiological group

4.3

4.2

4.5

4.4

4.5

4.6

4.6

4.5

4.6

4.8

4.8

4.0

radiologists and radiologists

0.9

0.9

1.3

1.2

1.2

1.3

1.4

1.4

1.5

1.5

1.3

1.4

oncologists

0.6

0.6

0.7

0.9

0.8

0.8

0.7

0.8

0.8

0.8

0.4

0.5

of the total number of doctors, women

41.1

43.2

42.7

42.9

42.7

43.1

43.2

43.1

44.8

44.3

44.4

44.3

Number of nursing staff

310.2

319.7

324.6

327.4

332.4

336.4

341.3

348.2

356.7

365.7

369.8

372.5

Table 5.

Medical personnel by profession in the Republic of Uzbekistan (thousand people).

Overall, the data suggests that Uzbekistan has been investing in expanding both the doctor and nursing staff populations to enhance the country’s healthcare system. The increasing number of doctors reflects efforts to improve accessibility and quality of medical care, while the rise in nursing staff emphasizes the importance of a skilled workforce to support healthcare services. Furthermore, the relatively stable gender distribution among doctors indicates equal opportunities for both men and women in the medical profession in Uzbekistan.

The data presented represents the number of people utilizing contraception in various regions of Uzbekistan from 2015 to 2021. Contraceptive use is a crucial aspect of reproductive health, as it enables individuals to plan and space their pregnancies, leading to improved overall health indicators (Table 6).

Overall contraceptive use in Uzbekistan: The total number of people using contraception in Uzbekistan has shown a consistent increase over the years, starting at 3,828,362 in 2015 and reaching 4,274,655 in 2021. This upward trend signifies growing awareness and acceptance of contraception as an essential tool for family planning.

Regional variation in contraceptive use: There is notable variation in contraceptive use among different regions of Uzbekistan. Tashkent city consistently reports the highest numbers, with 309,099 people utilizing contraception in 2021. Other regions such as Andijan, Samarkand, Fergana, Namangan, and Kashkadarya also show significant numbers of contraceptive users. Smaller regions like Syrdarya, Karakalpakstan, and Surkhandarya report relatively lower numbers, although they still represent a considerable proportion of the population.

Importance of contraceptive use in health indicators: Contraceptive use plays a vital role in shaping various health indicators. It contributes to reducing maternal mortality rates by allowing women to plan their pregnancies, ensuring better access to healthcare services, and adequate intervals between pregnancies. Furthermore, contraception helps in controlling population growth and managing resources effectively. It also contributes to improving child health outcomes by enabling parents to focus on child-rearing and ensuring optimal care for each child.

Implications for reproductive health programs: The increasing numbers of contraceptive users in Uzbekistan indicate the success of reproductive health programs and their impact on raising awareness about family planning. These programs should be further strengthened and expanded to ensure access to a wide range of contraceptives and comprehensive sexual education. Special attention should also be given to regions with lower contraceptive use to address potential barriers and improve access to contraception. Overall, the data highlights the positive trend of increasing contraceptive use in Uzbekistan. It emphasizes the importance of effective family planning programs in improving health indicators, enhancing maternal and child health outcomes, and managing population growth. Policymakers should continue to prioritize and invest in reproductive health initiatives to sustain progress in this area and ensure the well-being of the population.

Regions

2015

2016

2017

2018

2019

2020

2021

Republic of Uzbekistan

3,828,362

4,188,042

4,191,924

3,789,161

3,930,052

3,993,356

4,274,655

Republic of Karakalpakstan

274,745

298,407

285,386

268,836

274,947

279,974

264,745

Andijan

352,007

315,158

352,352

365,871

374,284

368,117

379,702

Bukhara

228,240

278,122

366,882

531

108,896

66,177

86,891

Jizzakh

133,599

150,126

158,470

167,284

154,761

159,387

165,813

Kashkadarya

355,721

400,272

406,356

329,426

377,337

410,500

452,863

Navoi

133,282

145,388

143,958

150,374

153,254

163,135

169,159

Namangan

320,681

346,562

350,282

359,262

368,338

374,286

350,256

Samarkand

419,732

434,118

373,736

414,355

407,504

411,031

638,543

Surkhandarya

230,497

246,119

261,332

266,564

235,299

259,605

313,750

Syrdarya

109,804

112,894

124,232

105,989

104,235

108,667

104,392

Tashkent

318,213

359,360

358,563

348,683

357,238

363,977

368,045

Fergana

432,213

526,843

453,282

438,757

442,947

446,485

410,572

Khorezm

216,301

239,585

251,718

246,141

245,733

252,890

260,825

Tashkent city

303,327

335,088

305,375

327,088

325,279

329,125

309,099

Table 6.

Contraceptive use and its impact on health indicators in Uzbekistan (people).

6. Exploring the health systems of central Asian countries: A comparative study

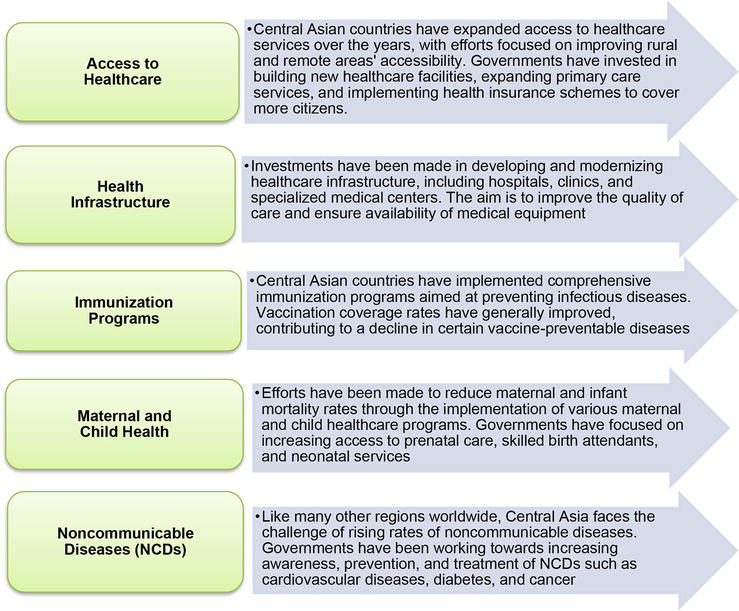

Studying the health systems of Central Asian countries is crucial for implementing State Mandatory Health Insurance (SMHI) in Uzbekistan. By examining the unique challenges and opportunities these countries face in healthcare provision, we can identify effective strategies to implement. Additionally, studying diverse health systems fosters international cooperation, allowing for knowledge sharing and improved healthcare outcomes globally. Understanding social determinants specific to the region aids in developing targeted interventions. Moreover, exploring different models contributes to evidence-based decision-making and the advancement of global health research and policy. In summary, studying the health system of Central Asian countries, specifically examining the advantages and challenges of SMHI in Uzbekistan, is relevant because it enables comparative analysis, facilitates policy learning, addresses regional needs, promotes equity and access, encourages international collaboration, and enhances the global understanding of healthcare systems.

Now, let us delve into some information about the health insurance practices in the bordering countries of Uzbekistan:

Kazakhstan: Kazakhstan has a mandatory health insurance system that covers basic healthcare services. The government also subsidizes the insurance premiums of certain groups, including low-income families, pregnant women, and children under 5 years old. This approach aims to ensure that vulnerable populations have access to essential healthcare services.

Kyrgyzstan: Kyrgyzstan has a universal health care system that covers all citizens and residents. The government provides free basic healthcare services, but the quality of care can be inconsistent. Efforts are being made to improve the overall quality of healthcare provision in the country.

Tajikistan: Tajikistan has a state-funded healthcare system that provides basic medical services at no cost to citizens. However, the quality of care is generally poor, and patients often have to pay for medications and specialized treatment. Improving the quality and accessibility of healthcare services is a major challenge in Tajikistan.

While conducting academic analyses on the healthcare systems and health insurance practices in Central Asian countries, it is crucial to review international organizations that provide individual and worldwide analyses in this field. One prominent organization in this regard is The World Health Organization (WHO), which has conducted numerous studies and assessments on healthcare systems in Central Asian countries. WHO’s Health Systems Performance Assessment, for instance, offers comprehensive analyses of the strengths and weaknesses of health systems in countries such as Kazakhstan, Kyrgyzstan, Tajikistan, and Uzbekistan. These assessments evaluate various aspects, including access to healthcare services, quality of care, financing mechanisms, and health system governance.

Additionally, The World Bank has also published reports and research papers that focus on healthcare in Central Asia. These publications often scrutinize health insurance practices in the region and analyze the effectiveness and efficiency of different models. The studies conducted by The World Bank shed light on the challenges faced by countries like Uzbekistan in implementing State Mandatory Health Insurance, while also providing recommendations based on international best practices.

Another notable organization is the Asian Development Bank (ADB), which conducts research and provides technical assistance to support healthcare reform in Central Asian countries. ADB’s publications and studies delve into topics such as healthcare financing, health insurance schemes, and strategies for improving healthcare accessibility and quality. These resources offer valuable information for policymakers and researchers seeking to understand the dynamics of health systems in the region. In addition to international organizations, academic institutions and research organizations also contribute significantly to our understanding of Central Asian health systems. For example, universities and think tanks may conduct studies on specific aspects of health insurance in countries like Kazakhstan, Kyrgyzstan, and Uzbekistan. These academic publications explore various topics, including the impact of health insurance on healthcare utilization, financial protection for vulnerable populations, and policy implications for achieving universal health coverage.

To summarize, international health organizations such as the World Health Organization, World Bank, and Asian Development Bank, in conjunction with academic institutions, play a critical role in providing analytical and academic insights into health insurance practices and healthcare systems in Central Asian countries. Their research, reports, and studies assist policymakers and researchers in gaining a deeper understanding of the challenges and opportunities associated with implementing health insurance schemes. As a result, evidence-based decision-making for healthcare reform is facilitated.

It is important to note that while Central Asian countries have mandatory health insurance systems, there can be significant variations in the quality and coverage of healthcare services. Conducting a SWOT analysis (Strengths, Weaknesses, Opportunities, and Threats) can provide further insights into the health insurance practices in these countries. By comparing the medical care systems of different nations, we can identify best practices and areas for improvement.

In conclusion, exploring the health systems of Central Asian countries, including their health insurance practices, allows us to gain valuable knowledge that can inform policy decisions, promote collaboration, address regional needs, and enhance the understanding of healthcare systems globally (Figure 1).

Figure 1.

Several reasons why we highly need to study the health system of central Asian countries. Source: Author.

The SWOT analysis for health insurance in Central Asian countries highlights several important factors that have an impact on the sector. While there are strengths and opportunities that present favorable conditions, there are also weaknesses and threats that need to be addressed for the continued growth and success of health insurance.

One of the key strengths identified is the growing demand for health insurance as the healthcare infrastructure improves in Central Asian countries. This indicates an increasing awareness of the importance of accessing quality healthcare services and presents an opportunity for insurers to cater to this demand. Government support is another strength, as governments in Central Asian countries are recognizing the significance of health insurance and taking steps to promote and regulate the sector. This support can help overcome barriers and facilitate the expansion of health insurance coverage. The competitive market in Central Asia is also a strength, as multiple insurance providers foster competition, leading to more affordable and innovative insurance options for consumers. This can drive market growth and improve the accessibility of health insurance (Table 7).

Strengths

Weaknesses

Growing demand: As the healthcare infrastructure improves in Central Asian countries, there is an increasing demand for health insurance to access quality healthcare services.

Government support: Governments in Central Asian countries are recognizing the importance of health insurance and are taking steps to promote and regulate the sector.

Competitive market: The presence of multiple health insurance providers fosters competition, leading to more affordable and innovative insurance options for consumers.

Development assistance: International organizations and donor countries often provide financial support to develop and strengthen the health insurance systems in Central Asian countries.

Limited coverage: Health insurance coverage is still limited in many areas, with rural populations and vulnerable groups having less access to affordable insurance options.

Underdeveloped infrastructure: The healthcare infrastructure in some Central Asian countries is still developing, which can limit the availability and quality of services covered by health insurance.

Lack of awareness: A lack of awareness and understanding about the benefits and importance of health insurance among the general population can hinder its uptake and utilization.

Financial constraints: Limited financial resources and affordability issues may prevent individuals from purchasing health insurance, leading to a large uninsured population.

Opportunities

Threats

Market growth potential: With the increasing recognition of the importance of health insurance, there is significant potential for market growth in Central Asian countries.

Innovation and digitization: Advances in technology and digital platforms provide opportunities for insurers to offer convenient and user-friendly health insurance products and services.

Partnerships: Collaboration between health insurance companies and healthcare providers can lead to improved healthcare access and better coverage options for policyholders.

Customization: Tailoring health insurance programs to meet the specific needs and preferences of different population segments, such as young adults or elderly individuals, can attract more participants.

Regulatory challenges: Frequent changes in regulations and policy frameworks can pose challenges to health insurance providers operating in Central Asian countries.

Cost inflation: Rising healthcare costs can increase the financial burden on health insurance providers and policyholders, potentially leading to increased premiums or reduced coverage.

External economic factors: Global economic fluctuations may indirectly affect the purchasing power and spending capacity of individuals, potentially impacting their ability to afford health insurance.

Table 7.

SWOT analysis for health insurance in central Asian countries.

Source: Author.

However, there are weaknesses that need to be addressed. Limited coverage, particularly in rural areas and among vulnerable groups, poses a challenge in ensuring equitable access to affordable insurance options. Underdeveloped healthcare infrastructure also limits the availability and quality of services covered by health insurance. Lack of awareness among the general population about the benefits and importance of health insurance is another weakness. Efforts to educate and raise awareness among the public will be crucial in increasing the uptake and utilization of health insurance. Financial constraints present another challenge, as limited resources and affordability issues may prevent individuals from purchasing health insurance, resulting in a large uninsured population. Finding ways to address these financial barriers is essential.

Opportunities exist for market growth, driven by the increasing recognition of the importance of health insurance. Innovation and digitization offer avenues for insurers to offer convenient and user-friendly products and services. Partnerships with healthcare providers can lead to improved access and better coverage options. Customization of insurance programs to meet specific population segments’ needs can attract more participants.

There are threats that need to be considered as well. Regulatory challenges, such as frequent changes in regulations and policy frameworks, can pose obstacles for health insurance providers. Rising healthcare costs can increase the financial burden on both insurers and policyholders, potentially impacting premiums and coverage. External economic factors, including global economic fluctuations, may indirectly affect individuals’ purchasing power and their ability to afford health insurance (Figure 2).

Figure 2.

Several common trends in healthcare across the central Asian countries. Source: Author.

In conclusion, while there are favorable conditions and opportunities for the growth of health insurance in Central Asian countries, addressing weaknesses and mitigating threats will be crucial to ensuring the sustainability and effectiveness of health insurance systems in the region.

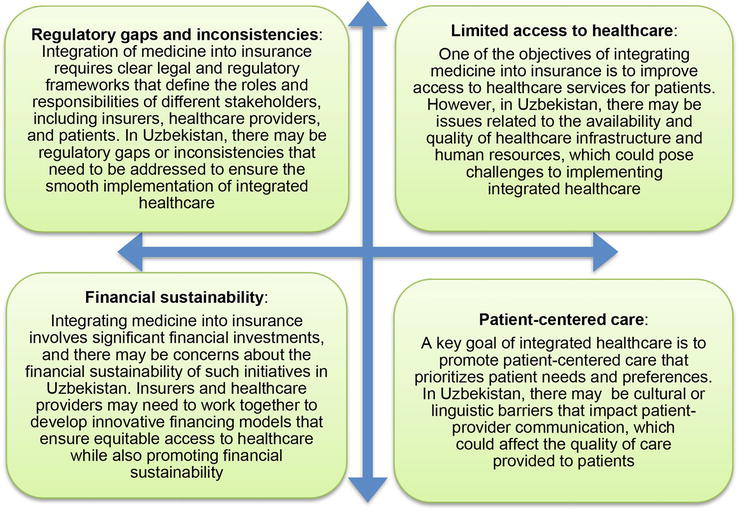

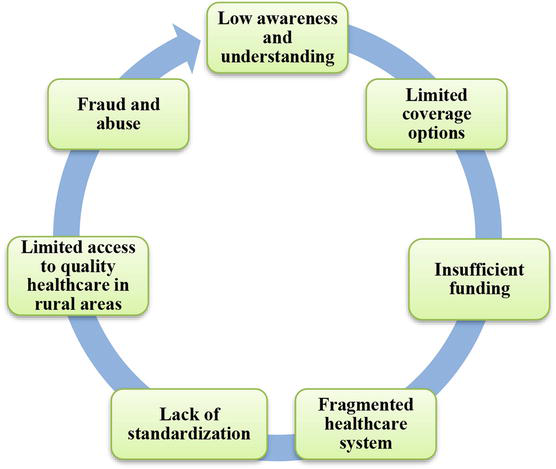

This analysis is just a general assessment and may vary depending on specific country circumstances within Central Asia. Central Asian countries such as Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan, and Uzbekistan have made significant progress in improving their healthcare systems since gaining independence in the 1990s. Each country has its own unique circumstances, based on the SWOT analysis we can see that there are several common trends in healthcare across the region, such as those described by Figure 3.

Figure 3.

Possible challenges that may arise during the integration process medical care with health insurance in Uzbekistan. Source: Author.

7. An overview and analysis of various health insurance models

The objective of this section is to provide a comprehensive review of various health insurance models and their implications for healthcare systems. By understanding the different types of health insurance models implemented worldwide, policymakers and stakeholders can make informed decisions to improve access, affordability, and the quality of healthcare. This review will explore the historical development of health insurance, examine key features of different models, and highlight case studies that showcase their real-world applications.

Health insurance plays a pivotal role in ensuring individuals have access to necessary healthcare services while mitigating financial risks associated with medical expenses. The evolution of health insurance models has been influenced by historical, economic, and social factors, leading to a diverse range of approaches adopted globally. In this section, our aim is to provide a comprehensive review of these health insurance models, shedding light on their origins, characteristics, and impact. To grasp the evolution of health insurance models, it is crucial to delve into their historical roots. Health insurance traces its origins back to ancient civilizations, where early forms of mutual aid societies emerged to provide financial support during times of illness or injury. Over time, healthcare financing mechanisms transformed to accommodate societal changes and emerging healthcare needs. Understanding this historical context will enable us to appreciate the environment within which contemporary health insurance models operate.

Health insurance models vary significantly worldwide, reflecting the diverse approaches different countries take to finance and deliver healthcare. Here are some commonly observed health insurance models:

Socialized medicine: This model, prevalent in countries like the United Kingdom and Sweden, involves government ownership or control of healthcare facilities. The government funds healthcare through taxes and provides services directly to citizens, aiming to ensure equal access for all [27, 28].

National health insurance: Countries like Canada and Taiwan have adopted this model. It involves a single-payer system where the government finances healthcare through a universal insurance program. Healthcare providers remain private, but the government acts as the sole insurer and pays for covered services [29, 30].

Bismarck model: Named after Germany’s chancellor Otto von Bismarck, this model is followed by several European countries such as France, Germany, and the Netherlands. In this system, health insurance is provided by multiple nonprofit, heavily regulated sickness funds. The funds are financed through contributions from employers and employees, ensuring universal coverage [31, 32].

Beveridge model: Similar to socialized medicine, this model is found in countries like Spain and Italy. The government runs healthcare facilities and employs healthcare professionals. Healthcare is financed through general taxation, providing free or low-cost services to all citizens [33, 34].

Managed care: Common in the United States, managed care involves private health insurance companies negotiating contracts with healthcare providers to deliver care to policyholders. These insurers closely manage healthcare utilization and costs, often employing networks of preferred providers [25].

Market-based insurance: Predominantly seen in countries like the United States, Switzerland, and the Netherlands, this model emphasizes competition among private insurance companies. Individuals purchase private health insurance plans, which are regulated to ensure a minimum benefit package. Governments often play a role in subsidizing insurance premiums for low-income individuals. These models represent different approaches to achieve universal healthcare coverage, control costs, and ensure access to quality healthcare. Each has its own advantages, challenges, and variations within specific countries. Ongoing research and policy debates continue to explore the effectiveness and efficiency of these models in different healthcare systems worldwide.

These different models offer various advantages and drawbacks, reflecting the diverse ways countries structure their healthcare systems. By examining and understanding these models, we can gain insights into what works well in different contexts and utilize this knowledge to inform policy decisions aimed at improving healthcare systems globally. In terms of socio-economic efficiency, each model has different advantages and disadvantages. By investigating every model, we can conclude that the National Health Insurance Model and the Bismarck Model allow for more private sector involvement and individual choice, but they tend to be more expensive due to higher administrative costs. The Social Health Insurance Model and Beveridge Model are more cost-effective, but they may have longer wait times for treatment. Ultimately, each country must consider its unique cultural, economic, and political circumstances when deciding which health care model is best suited for them. It is important to note that the advantages and disadvantages can vary within each model, as countries implement them differently based on their specific healthcare systems, socio-political contexts, and population needs (Table 8).

Advantages

Disadvantages

Socialized medicine

Provides equal access to healthcare services for all citizens, regardless of income or social status

Potential for long waiting times and limited choice of healthcare providers

Lower administrative costs due to a single-payer system

Higher tax burden on individuals and businesses

Can negotiate lower prices for medications and services

Limited private sector competition and innovation

National health insurance

Universal coverage ensures access to healthcare services for all citizens

Potential for longer wait times for specialized care

Simplified billing process as there is a single insurer

Limited choice in healthcare providers

Reduced administrative costs compared to a multi-payer system

High tax burden to fund the insurance program

Bismarck model

Equal access to healthcare services, irrespective of income or employment status

Limited choice of healthcare providers

Centralized control facilitates efficient resource allocation

Longer waiting times for non-urgent treatments

Lower administrative costs compared to multiple payer systems

May face issues with underfunding and strain on resources

Managed care

Emphasizes preventive care and coordination of services

Limited choice of healthcare providers outside the network

Cost containment through managed utilization and negotiated pricing

Potential for increased bureaucracy and administrative complexities

Flexibility in choosing healthcare providers within the network

Difficulty in balancing cost control measures and quality of care

Market-based insurance

Promotes competition among insurance providers, potentially leading to better services and prices

Affordability challenges, especially for lower-income individuals.

Offers a variety of insurance plans, allowing individuals to choose based on their needs

Risk of coverage gaps and disparities between different insurance plans

Emphasizes individual choice and autonomy in healthcare decision-making

May not guarantee universal coverage or equitable access to healthcare services

Table 8.

Pros and cons of health insurance models worldwide.

Source: Author.

The government of Uzbekistan has recently introduced a healthcare reform program called “Healthy Mother and Child” to enhance access to quality healthcare services for all citizens, particularly women and children. This program includes the integration of health insurance and medicine. In Uzbekistan, there are two main types of health insurance: state-funded insurance and voluntary insurance. The state-funded insurance is available to all citizens and covers basic medical services like doctor consultations, laboratory tests, and some medications. On the other hand, voluntary insurance is provided by private insurance companies and covers additional medical services such as hospitalization, surgeries, and more medications that are expensive. To integrate health insurance and medicine effectively, the government has implemented various measures. Firstly, the Ministry of Health is collaborating closely with the Ministry of Finance and the State Health Insurance Fund to revise the current list of basic medical services covered by the state-funded insurance. This revision aims to include more comprehensive medical services and improve patient care quality. Secondly, the government is promoting the involvement of private insurance companies in healthcare provision. The Ministry of Health is establishing partnerships with private insurance companies to offer affordable and comprehensive health insurance plans that cover a wider range of medical services. In summary, the ongoing integration of health insurance and medicine in Uzbekistan requires cooperation between different government agencies and private insurance companies. The ultimate goal is to enhance access to quality healthcare services for all citizens, regardless of their financial status.

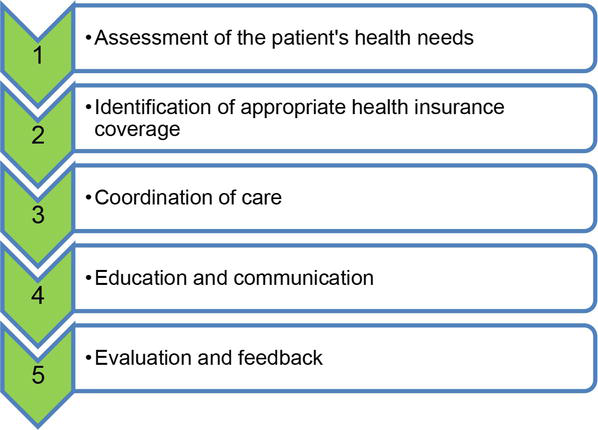

In practice there are several main proved steps involved in integrating health insurance with medicine:

The first step is to assess the patient’s health needs, including their medical history, health status, and any chronic conditions they may have. Based on the patient’s health needs, appropriate health insurance coverage must be identified, taking into account factors such as coverage type, premiums, deductibles, and co-payments. Once health insurance coverage is identified, coordination of care between health insurers and healthcare providers is necessary to ensure that patients receive the appropriate care and that insurance claims are processed efficiently. Patients must be educated about their health insurance coverage and how to use it effectively, including understanding their benefits, accessing network providers, and filing claims. Finally, regular evaluation and feedback are necessary to identify areas for improvement and ensure that the integration of health insurance and medicine is successful in improving patient outcomes and reducing costs (Figure 4).

Figure 4.

The main steps of health insurance realization into practice. Source: Author.

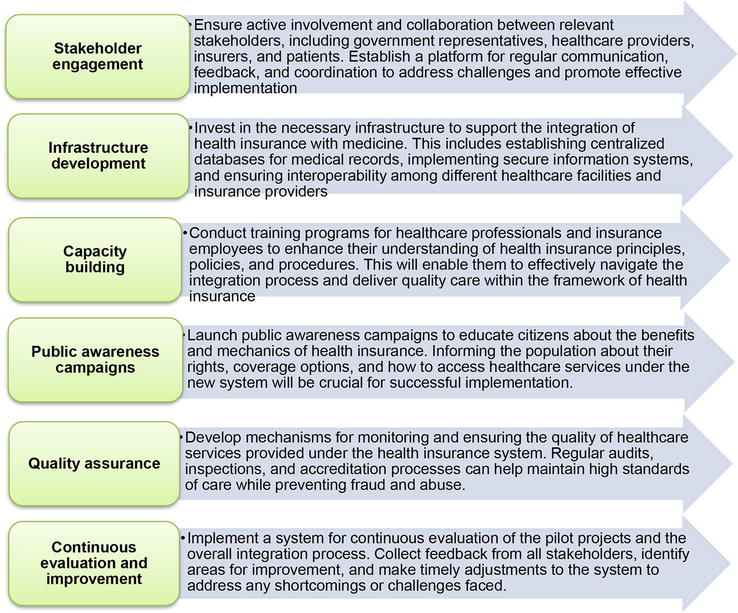

Based on the main steps of integrating health insurance with medicine in Uzbekistan, there are several directions and strategies that can effectively facilitate the implementation of these steps. It is important to note that this project is the first of its kind in the history of Uzbekistan’s medical care system. Therefore, it is recommended to thoroughly analyze all aspects of the medical infrastructure, the level of medical development, and the medical culture of the Uzbek people before implementing these steps. To support the implementation of the integration process, it is highly recommended that these supportive directions and methods are considered at every step of the realization of health insurance. Figure 5 shows some directions and guidelines to support the integration process of Uzbekistan’s medical care system:

Figure 5.

Some supportive guidelines for the integration of health insurance into Uzbekistan’s medical care system. Source: Author.

These recommendations are general in nature and should be adapted to the specific needs and context of Uzbekistan’s healthcare system. It is essential to engage local experts and stakeholders to develop a comprehensive strategy tailored to the country’s unique circumstances.

8. Understanding the complexities of health insurance realization in Uzbekistan: Opportunities, challenges, and problems

Over the years, Uzbekistan’s medical care system has undergone significant improvements, with the government prioritizing healthcare and implementing various reforms to enhance the quality and accessibility of medical services. One such reform is the draft law “On Compulsory Medical Insurance” which is a legislation that aims to ensure access to quality healthcare services for all residents of Uzbekistan which was stated in the resolution of the Cabinet of Ministers “On approval of the program on development of draft laws and their introduction to the Legislative Chamber of Oliy Majlis of the Republic of Uzbekistan in 2019”. The law establishes a comprehensive system of compulsory health insurance and its fund, which covers the cost of necessary medical services. The law emphasizes principles of equality, fairness, transparency, and efficiency in the provision of healthcare services and outlines the rights and responsibilities of insured individuals, healthcare providers, and insurance organizations. These efforts prioritize improving overall health and well-being by ensuring universal coverage and affordability of healthcare services. Large-scale reforms are planned to create conceptually new models for organizing and financing healthcare, significantly improving the efficiency, quality, and accessibility of medical care. Singapore, South Korea, Japan, France, Germany, Estonia, Norway, Latvia, Turkey, Russia, Azerbaijan, and Kazakhstan have been studied throughout the preparation of the draft law. Despite advancements, challenges remain, including outdated equipment and inadequate resources in some areas, reducing waiting times, improving efficiency, and patient satisfaction. Uzbekistan has expanded its healthcare infrastructure with modern medical facilities equipped with state-of-the-art technology, invested in training and professional development for healthcare workers and made efforts to decentralize medical care through regional medical centers and clinics. Telemedicine initiatives have also been introduced, allowing patients to consult with doctors remotely.