Open Access is an initiative that aims to make scientific research freely available to all. To date our community has made over 100 million downloads. It’s based on principles of collaboration, unobstructed discovery, and, most importantly, scientific progression. As PhD students, we found it difficult to access the research we needed, so we decided to create a new Open Access publisher that levels the playing field for scientists across the world. How? By making research easy to access, and puts the academic needs of the researchers before the business interests of publishers.

We are a community of more than 103,000 authors and editors from 3,291 institutions spanning 160 countries, including Nobel Prize winners and some of the world’s most-cited researchers. Publishing on IntechOpen allows authors to earn citations and find new collaborators, meaning more people see your work not only from your own field of study, but from other related fields too.

To purchase hard copies of this book, please contact the representative in India:

CBS Publishers & Distributors Pvt. Ltd.

www.cbspd.com

|

customercare@cbspd.com

Eight years following the first democratically elected government in South Africa in 1994, most public sector employees remained unable to access private health insurance and care due to high cost. In 2002, the Parliamentary Cabinet approved a policy framework on a restricted medical insurance scheme for public sector employees. This policy centered around the principles of equity, efficiency, and differentiation. Employees would have access to essential healthcare benefits across different option plans under equitable remuneration structures based on their health needs. The establishment of the Government Employees Medical Scheme (GEMS) was approved by the Cabinet in 2004 and was then registered and operationalised in January 2005. This chapter aims to describe the evolution of GEMS as the largest closed medical insurance scheme within South Africa over the past 18 years, and how it improved access to care by embracing Universal Health Coverage (UHC) principles. We present the socio-demographic evolution of the Scheme and how it and the employer have provided affordable contributions and expanded healthcare benefits to universally cover members, their immediate and extended families during their active working years and retirement. We also expand on member-centric benefit design and the critical role of organised labor and government, as both employer and policy maker.

Government Employees Medical Scheme, Pretoria, South Africa

Mapule Letshweni

Government Employees Medical Scheme, Pretoria, South Africa

Mabatlo Semenya

Government Employees Medical Scheme, Pretoria, South Africa

Boldwin Moyo

Government Employees Medical Scheme, Pretoria, South Africa

Carmen Whyte

Government Employees Medical Scheme, Pretoria, South Africa

Jolene Bultinck-Human

Government Employees Medical Scheme, Pretoria, South Africa

Stanley Moloabi

Government Employees Medical Scheme, Pretoria, South Africa

*Address all correspondence to: selaelo@gems.gov.za

1. Introduction

South Africa has made substantial progress in developing its healthcare system since 1994. Universal access is a fundamental principle in the Constitution of the Republic of South Africa, and health sector policies and outcomes have improved on aggregate. However, health inequalities remain a significant challenge facing the country [1]. South Africa has a two-tiered system. The government health services mainly serve 84% of the population, with the majority from low- and middle-income strata. In contrast, private facilities mainly service the smaller (16%) subset of wealthier households and take up a significant share of the overall health spending [1, 2]. The public sector is funded through taxes and the private sector through out-of-pocket payments and voluntary private health insurance, known as medical schemes in South Africa [1, 2].

A framework policy on restricted (closed) medical schemes was approved by the Cabinet in 2002 for further development by an interdepartmental working group (Departments of Public Service and Administration, National Treasury, Health, Education, Correctional Services, and the South African Police Service), and is centered in equity, efficiency, and differentiation. Equity is defined as “where employees have equal access to the most extensive set of equal basic benefits under equitable remuneration structures, subject to affordability”.. Efficiency focuses on the delivery and costs of benefits. Differentiation takes place when an employee chooses a more extensive cover and has equal access to higher benefits subject to their needs [3].

Income Inequality and disparities in healthcare are intricately linked. The history of apartheid or healthcare segregation in South Africa has a long history dating back to the 18th Century when the African people and European people received different levels of care. The debates for a white civil servants’ medical scheme started way before the implementation of apartheid (segregation policy by National Party in 1948.) The inadequate provision of medical care led to the establishment of voluntary medical insurance for white government employees, the Civil Servant’s Medical Benefit Association (CSMBA) [4]. This medical scheme only covered the wives of Civil servants and their children under the age of 18; white servants of members could be included at a fee.

The debates for National Health Services in South Africa started with the publication of the Beveridge Report in 1940, which formed the basis of the current British Health National System (NHS). Between 1942 and 1944: the Gluckman Commission advocated for a unitary national health service and free medical care to all South Africans [5]. When the National Party came into power in 1948, this was abolished. Then the Civil Society Medical Scheme Benefit was born in 1967 [6]. This was contributory medical insurance that only covered state employees. Its rapid expansion and lack of underwriting led to the scheme’s demise.

This chapter describes the evolution of the Government Employees Medical Scheme (GEMS) as the largest closed medical insurance scheme within South Africa over 18 years and how it improved access to qualifying government employees by embracing UHC principles. The chapter will present the socio-demographics evolution of the Scheme and how the Scheme and the employer have provided affordable contributions and expanded healthcare benefits to universally cover the members during their active working years and in retirement.

2.1 History of South African apartheid, health, and inequality

In 1994, the African National Congress (ANC) won elections against the then-ruling National Party, which had ruled the country since 1948. The National Party developed a health care system sustained through the years by promulgating racist legislation. The net result has been a system that was fragmented, biased towards curative care, inefficient, and inequitable. The ANC abolished the Apartheid system and developed an inclusive constitution that stated health as the right of citizens and those who live in the country [7]. When the ANC took over, governing the country in 1994, South Africa had a very poor Human Development Index (HDI) of 0.66 [8]. This indicator gauges the socio-economic progress of a nation. It considers factors such as the average number of years spent in education, the anticipated number of years spent in school, life expectancy at birth, and gross national income per capita. In 1993, the infant mortality rate (IMR) during that time was 46 per 1000 live births, life expectancy was 63 years old and a Gini- coefficient of 59.3 [9, 10, 11]. These indicators have since increased, and in 2020, just before COVID-19, the HDI was 0.73, the IMR was 27 per 1000 live births, the Gini-coefficient was 63, and life expectancy peaked at 65 years [8, 10, 11, 12]. These indicators improved along with the GDP (Gross Domestic Profit), which almost doubled from 2004 to 2022 [13].

In 1994, the ANC implemented the Reconstruction and Development Programme (RDP) to address disparities in the country’s social and economic maladies, as well as the National Health Plan [14, 15]. This was followed by the 1997 White Paper on the Transformation of the Health System, which intended to develop an equitable and unified health system capable of delivering quality health care through primary health care with constitutionally enshrined rights [16].

Healthcare financing reforms included promulgating the Medical Schemes Act (MSA) of 1998 as a steppingstone towards Social Health Insurance (SHI) [17, 18]. Before the promulgation of the MSA, medical insurance could discriminate based on gender, race, or ill health. The act intended to promote equitable access to health care, efficient utilisation of resources, and protection of individuals against financial catastrophe using principles of social solidarity. The pillars of the act include open enrolment (anybody wishing to apply could apply), community rating (not determining contributions based on health risks), and prescribed minimum benefits (PMBs), which mandated a full cover for chronic conditions and a list of 270 plus conditions subject to the designated service provider, managed care protocols and defined medicine lists. Apart from the list of chronic diseases, the Medical Schemes Act’s PMBs promoted in-hospital care. The Health Market Inquiry (HMI) found that these provisions led to market failures by promoting supplier-induced demand, lack of competition, and insufficient considerations for health outcomes [2].

The Medical Schemes Act prevented all forms of discrimination, including race, gender, age, or ill health. Members on the same option plan had to receive similar benefits, although contributions could be income-based [17]. To protect members against anti-selection, that is, members choosing to buy cover only when health needs arise, the Act allowed a three-month general waiting and twelve-month condition-specific waiting period. The fourth pillar, mandatory participation, is unlikely to be implemented due to changes in healthcare financing policy.

Before 2004, the South African Government Advanced Social Health Insurance (SHI) as mandatory health insurance. The Healthcare Finance Committee of 1994 recommended that the core membership of arrangements to expand coverage to other groups over time should consist of formally employed individuals and their immediate dependents [19]. It was at the peak of these debates that GEMS was born.

The ANC resolved to introduce the National Health Insurance (NHI) in 2007. The proposed NHI aims to achieve equal access to healthcare and universal financial risk protection. The NHI policy papers have been developed, and the NHI Bill is presented at the National Council of Provinces (NCOP) Parliament [20, 21, 22, 23]. The Bill addresses the role of medical schemes as complementary once NHI is implemented. It is envisaged that NHI will take some time to be fully implemented.

2.2 GEMS demographics

GEMS was established as a voluntary private health insurance in 2005, the first member to join was a male 52 years old, together with his wife and 2 children effective from 1 January 2006. Since the Scheme was and still is voluntary, government employees could choose not to belong to the medical scheme. The Scheme is a closed medical scheme as it only caters to government employees and their families. GEMS members can enrol their immediate families, i.e., spouses and children. Cover can be extended to relatives, e.g., parents, grandparents, nephews, nieces, and anyone financially dependent on the member. The wide family coverage is in harmony with the moral theory of Ubuntu (African philosophy of you are because I am) and filial obligation (duty of care to one’s parents). In the GEMS context, enabling families to support their extended family echoes Ubuntu and social solidarity principles at a family level where the value of relationships is for the wellbeing of the immediate and extended family. Ubuntu is also a means to equity. Ubuntu, as a principle of equity, means that well-off family members often support the members who have no means for the collective well-being of the immediate and extended family. It should be noted that these principles were not adequately articulated in the law, and GEMS had to respond to the societal norms and practices in its design [24].

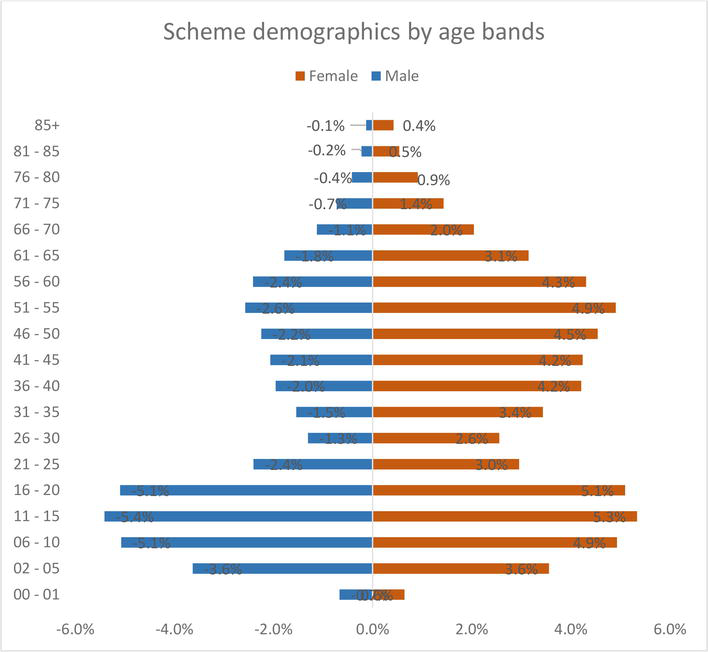

Since implementation, the scheme has grown to over 818 thousand members, covering 90.52% of public sector employees and over 2.1 million beneficiaries. Figure 1 shows the member gender age distribution. Currently the Scheme has 461,082 (21.1%) adult dependents and 907,971 (41.5%) child dependents. The member to dependency ratio is 1.67. The average family size is 2.67. Amongst the principal members 60% are females.

Figure 1.

Scheme demographics by age.

In 2017, the Council for Medical Schemes (CMS) reported that only restricted schemes had shown growth, and this growth is mainly attributed to GEMS [25]. While the entire industry showed attrition in membership during the Covid-19 period, GEMS membership increased by 10.9% between January 2020 and 31 December 2022, at the pick of the pandemic [25, 26].

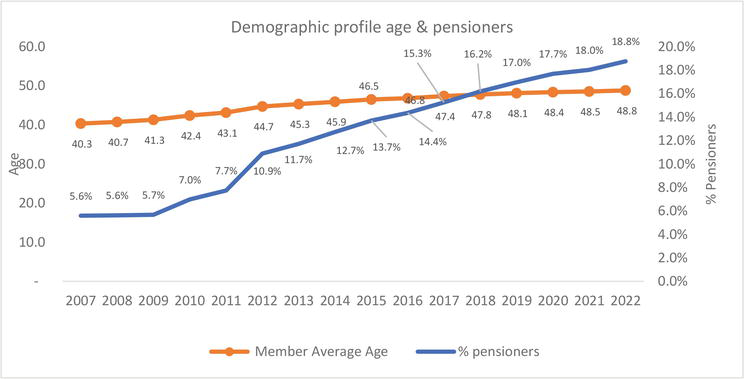

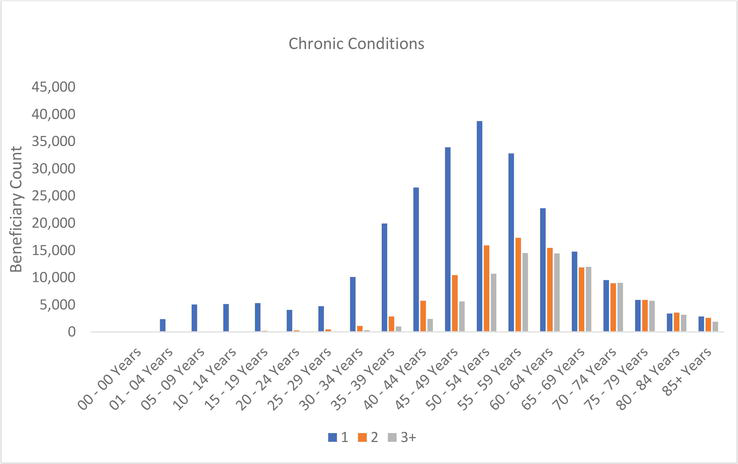

The average age of beneficiaries of the scheme is 32.9 years, and pensioner ratio (>60 years) is 19.1%. A total of 527,138 (24.1%) beneficiaries have at least one chronic disease. Figure 2 shows average age trend for the principal members and the proportion of pensioners (>60 years), and Figure 3 outlines the multiple comorbidities by age group. Figure 3 shows that the probability of developing two or more chronic conditions increases with age. The majority of members aged 60 years and older have at least two or more chronic conditions. The Scheme has an HIV prevalence of 6.8%, which is lower than the SA prevalence of HIV, which is 18.3% [27].

Figure 2.

Trend in the average age of the scheme and > 60 years the ratio.

Figure 3.

Beneficiary counts by chronic disease status and age:

2.3 Benefit design

Benefit design is decisions made about the funding (fully or partially) of health services and goods. Over the last few years, benefit design has evolved to embrace the UHC principles and Tanzanite one was developed as an essential basic benefit package. The ix plans which are, in increasing order of benefit richness: Tanzanite One, Beryl, Ruby, Emerald, Emerald Value (EVO), and Onyx. As required by legislation, all our plans cover essential health care, including PMBs.

Two options, Tanzanite One and EVO, are the flagship options, and EVO is an efficiency discounted option of the Emerald option. These options were developed during the period of the Health Market Inquiry. In return for making use of a network of healthcare providers, general practitioner (primary healthcare) nomination, and strict referral to specialists, members can pay 16% less in contributions for the same benefits on EVO as on the Emerald option. Membership of this option grew rapidly, from 19,000 members in 2017 at the introduction to over 100,000 at the end of 2021; this represents a 425% growth in five years [28].

GEMS, together with Public Service Co-ordinating Bargaining Council (PSCBC), established the Tanzanite One option in January 2020. PSCBC was established in terms of Section 35 of the Labour Relations Act, No. 66 of 1995 as amended to provide a platform for the State as the Employer, and the Public Service Unions as social partners to engage constructively over matters of mutual interest. In December 2017 PSCBC made a resolution to review resolved [29]. This resolution was amended in the PSCBC Resolution 1 of 2018 to develop a benefit product specifically for members earning on salary levels 1–5 (lowest income bands) that will enhance continuous medical cover.

Tanzanite One aims to provide members with comprehensive access to care at an affordable cost. The Tanzanite One option is intended to function as a template for the Basic Benefits Package as envisaged in the NHI policy papers, and as recommended by the HMI, while still noting that the option is contained by the confines of the MSA [1, 14, 15]. Tanzanite One has been designed to offer a broad spectrum of benefits, a comprehensive preventative package, unlimited primary healthcare, private hospitalisation, pathology, radiology, dental and optical benefits. The option also provides an essential medicine list at all levels of care. The benefits are also structured so that they address the prevention and treatment of the quadruple burden of disease in South Africa, namely: infectious diseases, chronic diseases of lifestyle, injuries, and maternal and child health. The option plan also considers the needs of vulnerable populations, defined as children, the elderly and people living with disabilities. And hence includes a modest package of assistive devices as well. In Tanzanite One, care coordination and network contracting make membership affordable, with an average contribution of R 100 monthly, equivalent to five United States dollars.

Since the establishment of Tanzanite One, the option has grown from 55,000 members in 2020 to 96,000 members in 2021, a 75% growth. In 2022, 93% of Tanzanite One members were satisfied with the option plan and considered it value for money. The Scheme has shifted from being hospicentric, dealing with only the seriously ill at a hospital level, over the years with appropriate funding of a preventative and primary healthcare package. The Scheme’s strategy is to further enrich access to health care by the Lancet Commission report, as Primary Healthcare (PHC) is the engine for UHC, PHC provides the programmatic approach in our context [30].

2.4 Affordability and efficiency

Affordability refers to how much GEMS contributions are cheaper than other medical schemes. GEMS contributions for an average family in 2023 are 25% lower when compared to the average contribution for competing schemes, as shown on Table 1. When accounting for the government subsidy on contributions, however, the contributions are 66% lower. The highest differences are noted for the Scheme’s flagship plan options, Emerald Value and Tanzanite One, due to the inherent efficiency built into these options by design. The Emerald Value and Tanzanite One plan options are designed as efficiency discount options (EDOs) in that only a list of healthcare service providers who are comparatively efficient in their healthcare delivery activities are included as part of the network providers to service these plan options. These efficiencies are then shared between the members of the Scheme through lower contributions and the healthcare service providers through an increased number of patients incentivised to use their services [31].

Option

% difference between GEMS average family contribution and average family contribution of competing schemes before subsidy

% difference between GEMS average family contribution and average family contribution of competing schemes after subsidy

Tanzanite One

38%

97%

Beryl

17%

70%

Ruby

5%

61%

Emerald

24%

59%

Emerald Value

34%

72%

Onyx

25%

53%

All

25%

66%

Table 1.

GEMS average affordability in 2023.

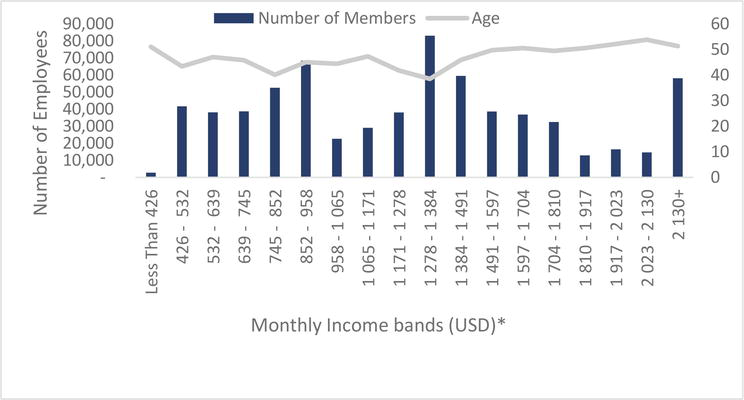

While GEMS members are spread across all income levels, there is, however, a higher proportion of members in low-income earners and middle-income earners, specifically Level 1–5, constituting 221,834 (27.1%) of all GEMS members, as shown on Figure 4. These low-income earners are spread across all options, with the majority in Tanzanite One plan option for affordability reasons. GEMS option plans are accessible for all government employees, a demonstration of a commitment to increase access to universal health coverage [32].

Figure 4.

Income distribution of public servants.

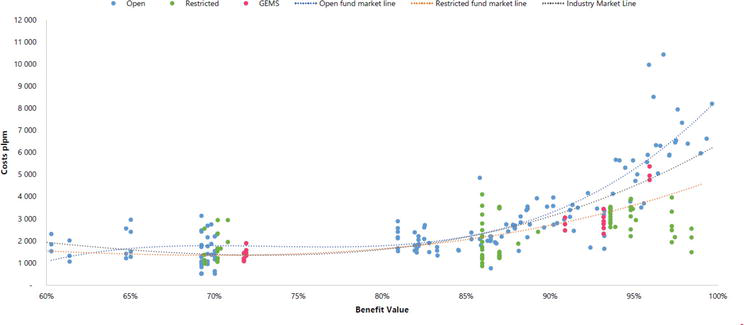

In addition to affordability, GEMS still manages to provide competitive plan options. The value for money offered by GEMS plan options is either better than or on par with the medical schemes industry. Figure 5 shows the results from an actuarial review of the benefit richness and cost comparison to medical industry shows that two thirds (specifically 4 out of 6) of GEMS plan options are performing better than the industry [33].

Figure 5.

Benefit value and costs PLPM 2023.

In addition to providing higher benefit value and affordable plan options, GEMS has managed to maintain efficiency in operations and return on investment. For every one Rand received in contributions the Scheme paid an average of R0.89 in healthcare costs for the members, thus translating into a claims loss ratio of 89%. This means that there is, on average, R0.11 left to cover the non-healthcare expenditure such as administrative fees (overhead costs) and retain some as reserves. The Council for Medical Schemes requires that all medical schemes keep in reserve at least 25% of annual contributions amount. The non-health expenditure for the Scheme remained very low at 4.81% compared to the industry of 8.66%, thus demonstrating administrative or operational efficiency [25]. CMS measures the industry solvency ratio.

The solvency ratio is the calculated level of reserves, or accumulated funds, needed by a medical scheme as a percentage of gross annualised contributions. At the end of 2021, GEMS had a solvency ratio of 46.44% compared to the industry average of 46.73% [25]. However, the scheme has not always met the statutory solvency ratio of 25%. In 2016 the Scheme had an all-time lowest reserve ratio sitting at 6.5%. The biggest driver of unsustainable coverage was found to be adverse selection. Interventions introduced included underwriting to reduce adverse selection. Underwriting was successfully submitted but limited to applying a general three-month and a twelve-month condition-specific waiting period, limited to principal members and beneficiaries who cancel membership and later wish to rejoin in the absence of termination of employment. The Scheme significantly improved the reserve ratio from 6.5% in 2016 to 46.1% by December 2021 [28].

2.5 Quality of healthcare and value

Health Quality Assurance (HQA), a non-profit organisation, assesses quality in healthcare by medical schemes annually. Such assessments aim to assist decision-makers to evaluate and improve the quality of care received by members [34]. The Scheme’s 2022 Annual Integrated Report outlined that about 82% of the healthcare quality outcomes were established to be above the industry average on predetermined Health Quality Assessment metrics. In 2020, GEMS showed an improvement in its primary health quality scores and was above the industry average in antenatal, chronic disease, and HIV management scores [34]. Not surprisingly as the GEMS basic benefit design prioritises coverage for the quadruple burden of disease in South Africa namely, chronic diseases care, maternal and child health, HIV program and all serious injuries are mostly included.

GEMS also has the most extensive HIV programs in the private health sector. As part of this HIV disease management programme, the Scheme aims to achieve what is termed the 90–90-90 targets. That is, 90% of Scheme’s members living with HIV must know their HIV status, and 90% of Scheme’s HIV positive members must be on antiretroviral therapy (ARTs) and 90% of Scheme members receiving ARTs must have viral suppression. Against these targets the Scheme is performing at 90%, 91.2% and 92.2% respectively.

In conclusion, South Africa’s health system, although making tremendous advancements over the past twenty years regarding UHC, remains two-tiered and inequitable. As a medical scheme, GEMS has followed a process of evolving towards providing improved and affordable access to healthcare to its members and their families over the past 18 years. The Scheme has embraced UHC principles and is preparing itself for the inevitable and eventual implementation of the NHI through the effective benefit design and influencing transformation of the health system towards the one that promote equitable universal access to health care. As a closed scheme, GEMS is continuously working towards improving access and affordability to qualifying members and closing the gap of past disparities. Based on findings discussed within this report such as a Scheme growth of 90.52% since implementation and a 75% growth on the Tanzanite one option just between 2020 and 2021 at a 93% satisfaction rate, the Scheme’s efforts are working, and also managing to maintain efficiencies in operations and return on investment.

1.James C, Gmeinder M, Rivadeneira AMR, Vammalle C. Health financing and budgeting practices for health in South Africa. OECD Journal on Budgeting. 2018;17(3):95-126

2.Competitions Commissioner of South Africa. Health Market Inquiry Report. South Africa. 2019. Available from: https://www.compcom.co.za/wp-content/uploads/2020/01/Final-Findings-and-recommendations-report-Health-Market-Inquiry.pdf

3.Government Employees Medical Scheme. The Introduction of GEMS South Africa. South Africa. 2023. Available from: https://www.gems.gov.za/en/About-Gems/Overview

4.Coovadia H, Jewkes R, Barron P, Sanders D, McIntyre D. The health and health system of South Africa: Historical roots of current public health challenges. The Lancet. 2009;374(9692):817-834

5.Phillips HT. The 1945 Gluckman report and the establishment of South Africa’s health centers. American Journal of Public Health. 1993;83(7):1037-1039

6.Verhoef G. From friendly society to compulsory medical aid association: The history of medical aid provision in South Africa’s public sector, 1905-1970. Social Science History. 2006;30(4):601-627

7.The Constitution of the Republic of South Africa. 1996

8.South Africa - Human Development Index - HDI [Internet]. 2021 [cited 1 August 2023]. Available from: https://countryeconomy.com/hdi/south-africa

9.Gini index - South Africa [Internet]. 1993 - 2014 [cited 1 August 2023]. Available from: https://data.worldbank.org/indicator/SI.POV.GINI?end=1994&locations=ZA&start=1993

10.Life expectancy at birth, total (years) [Internet]. 1960-2021 [cited 1 August 2023]. Available from: https://data.worldbank.org/indicator/SP.DYN.LE00.IN?end=1993&locations=ZA&start=1990

11.Mortality rate, infant (per 1,000 live births) - South Africa [Internet]. 1974-2021 [cited 1 August 2023]. Available from: https://data.worldbank.org/indicator/SP.DYN.IMRT.IN?end=2021&locations=ZA&start=1974

12.20 countries with the biggest inequality in income distribution worldwide in 2021, based on the Gini index [Internet]. 2021 [cited 01 August 2023]. Available from: https://www.statista.com/statistics/264627/ranking-of-the-20-countries-with-the-biggest-inequality-in-income-distribution/

13.World Bank Open Data [Internet]. 2022 [cited 31 July 2023]. Available from: https://data.worldbank.org/?cid=ECR_GA_worldbank_EN_EXTP_search&s_kwcid=AL!18468!3!665425039372!b!!g!!world%20bank%20projects&gclid=Cj0KCQjwn_OlBhDhARIsAG2y6zNycx65GB2zfdd9k1XVmpv8BuMUknX3VdGhWVifCmeHd-J7aC2eTowaAgqmEALw_wcB

14.African National Congress. National Health Plan. 1994

15.African National Congress. African National Congress A basic guide to the Reconstruction and Development Programme. 1994

16.National Department of Health. White Paper for the Transformation of the Health System in South Africa. 1997

17.South African Government. Medical Schemes Act. No. 131 of 1998. In: Department of Health, editor. South Africa. 1998

18.Harrison S. Medical schemes. South African Health Review. 2003;2003(1):291-298

19.Parliamentary Monitoring Group. NHI Timeline: Key dates and events. 2019

20.National Department of Health. White Paper on National Health Insurance. 2015

21.National Department of Health. National Health Insurance Green Paper. 2011

22.McIntyre D. Private Sector Involvement in Funding and Providing Health Services in South Africa: Implications for Equity and Access to Health Care. EQUINET, Harare: Health Economics Unit; 2010

23.NHI Timeline: Key dates and events [Internet]. 2023 [cited 31 July 2023]. Available from: https://pmg.org.za/blog/NHI%20Timeline:%20Key%20dates%20and%20events

24.Bennett TW. Ubuntu: An African equity. Potchefstroom Electronic Law Journal. 2011;14(4):30-61

25.Council for Medical Schemes. Annual Report 2021/22. South Africa; 2022. Available from: https://www.medicalschemes.co.za/cms-annual-report-2021-22/

26.Government Employees Medical Scheme. Annual Integrated Report. South Africa: Government Employees Medical Scheme; 2021

27.Prevalence of HIV, total (% of population ages 15-49) - South Africa [Internet]. 2022. Available from: https://data.worldbank.org/indicator/SH.DYN.AIDS.ZS?locations=ZA

28.Whyte C, Mametja S, Semenya M, Bultinck-Human J, Matoti L, Moyo B, et al. Primary healthcare: Addressing financing reforms for universal health coverage. South African Health Journal. 2023:3-7

29.Public Service Co-ordinating Barganing Coucil. PSCBC Annual Report: 2021/2022. 2022

30.Hanson K, Brikci N, Erlangga D, Alebachew A, De Allegri M, Balabanova D, et al. The lancet Global Health Commission on financing primary health care: Putting people at the Centre. The Lancet Global Health. 2022;10(5):e715-ee72

31.Government employees medical scheme. Affordability Report. 2023

32.Government Employees Medical Scheme. Income bands report. 2023

33.Government Employees Medical Scheme. Signal Model Results. 2023

34.Health Qualtity Assessment. 17th Annual Industry Report on the Quality of Healthcare in South Africa. 2021

Written By

Selaelo Mametja, Mapule Letshweni, Mabatlo Semenya, Boldwin Moyo, Carmen Whyte, Jolene Bultinck-Human and Stanley Moloabi

Submitted: 04 August 2023Reviewed: 06 August 2023Published: 31 October 2023

Open access peer-reviewed chapter

Open access peer-reviewed chapter