Open access peer-reviewed chapter

Open access peer-reviewed chapter

Abstract

This chapter offers a detailed analysis of microinsurance (nowadays often called “inclusive insurance”), an innovative hybrid model combining grassroots initiatives with top-down approaches to reach populations not covered by government-operated social protection systems. With half of the global population, primarily in low and middle-income countries, lacking social protection, the chapter focuses on the potential of microinsurance to address this pressing issue. The commercial microinsurance attempts, often labeled as “insurance for the poor,” have been largely insufficient. An alternative lies in the “Collaborative and Contributive” (C&C) model of microinsurance, which harnesses social forces, typically more compelling than market forces in informal settings, to stimulate demand. The chapter evaluates microinsurance’s social and economic impacts, drawing insights from 25 years of progress. It underscores the need for policymakers, international development bankers, and the reinsurance industry to recognize the potential of the C and C model in providing comprehensive insurance to marginalized populations.

Keywords

- informal sector

- financial protection

- risk management

- affordable coverage

- insurance education

- microinsurance

1. Introduction

This chapter tackles a significant global development issue: the systemic exclusion of half the world’s population from vital social protection systems [1]. Such systems, encompassing crucial services like health insurance, social security, and social assistance, remain inaccessible to a large proportion of the global population. This widespread lack of access deprives numerous individuals of universal social protection coverage’s social and financial benefits. It hinders economic growth and equitable income and wealth distribution in various countries. A multitude of complex and interrelated factors drive this troubling situation.

In the early 1970s, Keith Hart’s seminal studies catalyzed discussions around informal employment [2]. Building upon this momentum, the International Labour Organization (ILO) soon introduced the ‘non-traditional insurance’ concept. Presented in their 1972 report [3], this foundational discourse on informal sectors and non-traditional insurance continued to gain traction in the 1980s and 1990s structural adjustment era. This idea took a definitive form in the 1990s, culminating in the term ‘microinsurance.’ Over time, microinsurance has further evolved and is now commonly referred to as ‘inclusive insurance’ to emphasize the aim of reducing exclusion [4].

Microinsurance is not confined to health risks; it can address various perils. However, in this chapter, the focus is primarily on health-related risks, aligning with the overall subject of this book, which is health insurance. This clarification ensures that the scope of the discourse on microinsurance within this work is understood. This term referred to community-based organizations connected to larger structures to facilitate risk pooling. Given that, in many contexts, the perceived incapacity of the state to provide adequate social protection to specific segments of society, this approach was seen as necessary.

The chapter begins by outlining the problem and its background before discussing how the definition and application of the microinsurance concept can provide possible solutions.

1.1 Impact of predetermination beliefs on risk analysis and preventive measures

Cultural norms and societal priorities deeply embedded at the individual level often deter specific groups from accessing insurance mechanisms. From the dawn of time, adverse events have often been attributed to predestination, divine will, or the result of personal actions. This perception, which is still persistent in many parts of the world, causes many to avoid risk analysis and, even more, not to take preventive measures to counteract, mitigate, or compensate for risks (for more details on risk perception, see [5]). An approach to understanding those perceptions requires sustained collective commitment.

1.2 Role of insurance in addressing unforeseen events and financial consequences

Insurance is a proactive tool designed to mitigate financial consequences from unpredictable events. While the broader patterns of these events are known, the exact timing, location, severity, and specific individual or asset at risk are uncertain [6]. At its core, insurance operates on the principle of risk pooling.

Wilkie’s seminal work [7] aptly differentiates between two primary forms of risk pooling:

In insurance and mutual organizations, “mutuality” traditionally denotes members’ shared benefits and burdens. Conversely, “solidarity” represents the foundational ethos of social insurance, where societal or group members collectively shoulder the cost of risk protection, irrespective of the individual risk they introduce.

However, many individuals, particularly those less affluent, less educated, or employed in the informal sector, perceive insurance as beyond their grasp, termed as “lack of agency.” This sentiment is especially strong towards commercial insurance among economically disadvantaged populations [8]. Similar sentiments are echoed in studies on microinsurance [9] and microfinance [10], where individuals feel challenged to manage predictable risks or maintain relationships with insurance providers.

1.3 Historical approach to government intervention in health insurance

Governments first ventured into (health) insurance regulation in the mid-nineteenth century. They expanded their involvement to include financing and provision in the twentieth century. We detail the four models [11] and then discuss the two that have proven more influential.

The initial efforts of European governments in insurance regulation in the nineteenth century were predominantly geared towards what can be termed as “private” insurance, based on the principle of mutuality, even if they were not always conducted through mutual associations in the modern sense. However, by the second half of the twentieth century, these models introduced more comprehensive systems, representing the nascent stages of what we now recognize as social insurance. As such, it’s crucial to differentiate between these early regulatory interventions and the more holistic, state-driven models of social insurance that followed.

1.4 Limitations and exclusions in these models, especially for the informal sector

The Bismarckian and Beveridge models are influential in many countries worldwide because they represent two distinct, well-established approaches to structuring social security and health insurance systems [17]. By contrast, the USA model is criticized for its complexity, high costs, and gaps in coverage [18]. And the Semashko model, accommodating the notion of unequal quality and quantity of care originating from the social order of the former Soviet Union, is now considered irrelevant to current debates on healthcare systems [16].

Why is there a pressing need for an additional model? The crux of the issue primarily lies in the top-down governance embedded in the four traditional models. These systems thrive on centralized decision-making and control, cultivating distinct command chains and potential efficiencies. But this centralization often propels these systems towards one-size-fits-all solutions, less suitable for context-specific governance [19]. Moreover, such systems are relatively volatile under unstable macroeconomic conditions [20]. And they strive to apply ‘one-size-fits-all’ solutions that may be unsuitable in numerous settings [21].

Moreover, many low- and middle-income countries have adopted a policy of attracting foreign investors to stimulate export-oriented manufacturing. These economies depend on exporting low-cost goods, which requires low-cost production, often leading to minimum wages for workers and slim business profit margins. Consequently, these countries frequently relax the requirements for foreign firms to provide social benefits, further lowering operating costs [22]. This approach stimulates export-oriented manufacturing with minimal workers’ wages and protection and can generate jobs and spur short-term economic growth. However, it often results in decreased tax revenues for the government. This strategy can be executed and scaled without requiring governments to implement extensive social protection models, not to mention the more comprehensive Bismarckian or Beveridgean systems.

1.5 Applicability of international labor standards on universal social protection coverage

The question may arise whether international labor standards might bind countries to provide at least minimal social protection. Although these matters have been acknowledged at various international conferences, there is no binding solution yet. The UN’s agency championing the evolution of social protection systems is the International Labour Organization (ILO). Before 2000, the ILO’s social security promotion focused on the formal economy [23]. The crux of the ILO’s strategy lay in advocating for the ratification and implementation of the Social Security (Minimum Standards) Convention, 1952 (No. 102) [24]. This convention, which outlines minimum standards for the principal branches of social security, reflects a Bismarckian approach, emphasizing contribution-based social insurance schemes.

Even before 2000, the ILO recognized that many nations could not apply the standards foreseen in Convention No. 102. Consequently, it supported a gradual expansion of coverage, considering national circumstances and stressing public consultation’s importance in determining suitable implementation strategies [25].

By the late twentieth century, it also became clear that a substantial segment of the global population remained excluded, particularly those in developing countries’ informal economies [26, 27].

Subsequently, the ILO began advocating for more flexible social protection models to reach underserved populations [28]. This shift resulted in the ILO’s 2012 Recommendation No. 202 [29], which promoted the idea of national Social Protection Floors (SPFs)—basic social security guarantees aiming to combat poverty, vulnerability, and social exclusion [30]. In addition to advocating for the realization of SPFs, the ILO supports formalizing informal employment and considering gender-specific risks in social protection design and implementation.

The World Health Organization (WHO) advocated for Universal Health Coverage (UHC), as well as microinsurance [31]. But its actions have been more declarative than practical. The 58th World Health Assembly (WHA) passed Resolution WHA58.33 in 2005, requesting member states to develop health financing systems capable of achieving and maintaining UHC. The 2010 World Health Report also focused on health financing, providing advice on raising funds, reducing dependence on direct service payments, and enhancing efficiency and equity.

Additionally, the United Nations General Assembly adopted a resolution in 2012 (A/RES/67/81), encouraging member states to progress towards providing UHC. This resolution has been reinforced by subsequent WHA resolutions and the inclusion of UHC as a target of the Sustainable Development Goals (SDGs) in 2015.

Consequently, while the UN and other international bodies have advocated for expanded health insurance access for marginalized populations, they have yet to enact any legally binding instruments to guarantee the realization of this objective. Furthermore, there is a lack of consensus on which entity should spearhead this mission.

2. Microinsurance: extending coverage to the informal sector

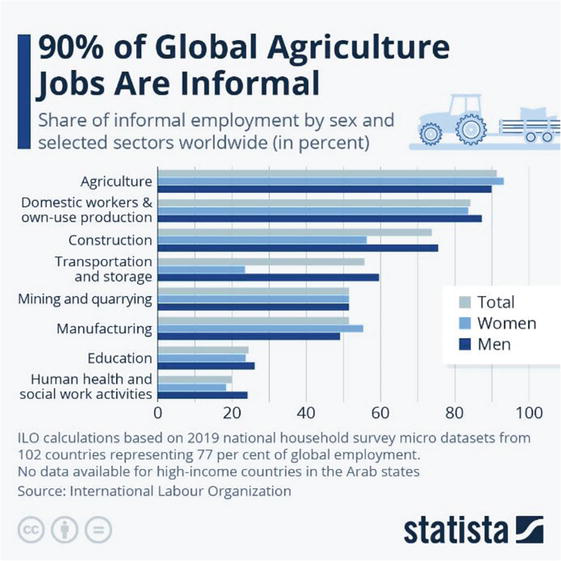

Microinsurance is a distinct insurance approach designed to meet the demand of often marginalized, underserved communities, focusing on needs identified and prioritized locally [32] (micro corresponds to local, meso to regional, and macro to national). Given that most uninsured individuals are engaged in the informal sector in Low and Middle-Income Countries (LMICs) and that many labor-intensive industries informally employ a significant portion of their workforce [ILO data; graph source [33]], it’s imperative to underscore the necessity of tailoring solutions to the unique circumstances of the informal sector (Figure 1).

Figure 1.

Hidden workforce: Informal employment in labor-intensive industries.

Later, we examine three interpretations of the term ‘inclusive insurance.’ In its original conception, the beneficiaries actively determine the insured risks based on their ability and willingness to pay premiums. Additionally, the insured group should participate in management and claim adjudication processes. This involvement reduces administrative costs, increases transparency, and nurtures trust. These unique characteristics distinguish it significantly from the operational models of traditional commercial or public insurance schemes.

2.1 Introduction to microinsurance as a non-mandatory social protection model

The International Labour Organization (ILO) introduced non-traditional coverage to offer social protection for informal and agricultural workers, often excluded from traditional pension and social security systems. This concept emerged during the structural adjustment era of the World Bank’s early exploration into index insurance [34]. However, attempts to expand social security to non-traditional workers during the 1970s and 1980s encountered significant funding challenges due to the withdrawal of government subsidies under structural adjustment policies [35, 36, 37].

During that period, the writings of Amartya Sen became particularly significant. His Capability Approach underscored the importance of individual agency and freedom in achieving developmental outcomes [38, 39]. Sen and Jean Drèze highlighted the importance of public participation in policymaking, advocating against top-down, overly simplified solutions to complex social problems [40].

By the late 1980s, the ILO, influenced by Sen’s emphasis on participatory development, suggested a novel approach: advocating for community-based social protection schemes using ‘traditional’ institutions [41]. This idea gained further traction in the 1990s, propelled by Elinor Ostrom’s groundbreaking work on managing common pool resources (CPR) [42]. Ostrom’s principles, advocating for local communities’ autonomy in managing common resources, resonated with the ethos of community-based social protection schemes that the ILO endorsed.

Influenced by Sen’s and Ostrom’s ideas, the ILO launched a project focusing on the informal sector in three major developing cities [43]. This project laid the groundwork for ‘microinsurance,’ introduced in 1999 [44]. Dror’s microinsurance model encapsulated community-driven organizations linked to larger structures for risk pooling. The model effectively merged Ostrom’s general approach to collective action and CPR management and Sen’s emphasis on participatory decision-making and freedom.

Dror’s model envisions communities collectively managing and distributing risks [45], supporting a locally organized and financed system that allows collective resource pooling and risk management. The model allows customization of insurance products to fit specific community needs and leverages existing social dynamics among the uninsured, offering affordable, context-specific, and demand-driven insurance packages.

However, during the early development of microinsurance, informal sector workers’ voices were often underrepresented, and consultation was insufficient, with empirical evidence of implementation lacking. The discourse was instead dominated by external parties from wealthier nations keen to pinpoint the defining features of microinsurance. Three principal perspectives emerged: one focused on the target population—“the poor” [46, 47]; another highlighted the product’s nature, characterized by “low cost and low coverage” [48, 49]; the third perspective centered on the type of insurance provider, whether mutual, social, or for-profit entities [50].

Commercial insurers found validation for their preference to sell insurance to individuals through agents in Thaler and Sunstein’s “nudge” concept [51], which advocates minor interventions to guide decision-making. While this concept aligns with Sen’s emphasis on freedom of choice [38], it lacks his emphasis on public discussion to enhance rationality [52]. Furthermore, it contrasts with Ostrom’s perspective on the capacity of local communities to self-govern common resources [42].

The blurred lines between “insurance for the poor” and “low-cost & low-coverage products” often resulted in both perspectives deviating from the original proposition of harnessing social dynamics [53, 54]. Additionally, low-cost products did not guarantee that “cherry-picking “practices1 would not leave protection gaps among the clients of these new products [55]. Several “low premium products” were developed without customizing to local risk exposure or sufficiently exploring the price sensitivity of the uninsured [56]. However, the lack of empirical evidence of implementation and clear evidence of benefits for target populations meant insufficient consultation among the poorest populations thwarted commercial success. The Micro Insurance Academy (founded by David Dror in New Delhi in 2007) focused on implementation support of the Micro Insurance Unit concept, embracing Sen’s and Ostrom’s theoretical foundations but with novel facilitation of ‘insurance education’ under the banner of the Collaborative and Contributive (C&C) microinsurance model, which underscores Sen’s emphasis on community participation, freedom, and collective engagement in tailoring solutions to specific local resource management [57, 58].

However, premiums had to be affordable. This begs the question: Are the uninsured interested in purchasing “cheap insurance for the poor”? [59]. The analysis of this vital issue forms the next point of discussion.

2.2 Price sensitivity: tailoring insurance plans based on economic status

Defining microinsurance as “insurance for the poor” insinuates two conditions: firstly, that such coverage exists outside the structure of a universal social protection system and, thus, contributory, but without government mandates. And secondly, the premiums should be low to suit the limited resources of poor people [60]. The first condition implies that microinsurance must be priced to compensate for the pure actuarial premium without subsidy [61]. Consequently, the cost of microinsurance could potentially exceed regular (subsidized) insurance, an outcome that is not typically deemed pro-poor. The second condition implies that low premium “insurance for the poor” could succeed if price sensitivity is high among the target group [62]. So, what concrete evidence is there to support this assumption?

Empirical evidence reveals that lowering the prices of microinsurance increases demand, but overall uptake is minimal [63, 64, 65]. Households with higher liquidity and easier access to credit are more likely to buy insurance, i.e., slightly less price sensitive [63, 66], and adjusted premium payment structures can ease liquidity constraints [67, 68]. Studies have highlighted the impacts of compound risk aversion and ambiguity aversion on insurance uptake [69, 70]. These studies suggest that the target population’s risk aversion and overall wealth level lead it to forego substantial premium discounts when the offer is insufficiently sensitive to specific demand drivers like income, education, age, household size, and health status. The effect of these demand drivers can vary significantly across different types of insurance [71, 72].

A crucial factor influencing demand is insured individuals’ out-of-pocket expenses on top of premiums when accessing healthcare. A qualitative study from Ghana [73] revealed that even insured clients of Ghana’s NHIS incur additional costs for consultations and medications, which should be covered by the scheme, primarily because of drug shortages and administrative fees. The study recommends eliminating these extra charges to enhance trust in the NHIS across all regions and facilities. A qualitative investigation in the USA [74], which has several laws to deliver “insurance for the poor,” points out that the lower out-of-pocket spending, the more likely the positive effect of premium subsidies2.

In the commercial microinsurance space, “insurance for the poor,” i.e., products that offer restricted coverage to maintain low premiums and profitability, or “freemium” coverage that conceals the insurance premium within the cost of mobile services but ignores other demand drivers, have struggled to achieve widespread acceptance and consistent renewal rates [53, 75, 76].

This situation is often encapsulated in the phrase “

Furthermore, it’s significant to them that their choices lead to widespread benefits for many group members. This underscores the desire to join voluntary and contributory Community-Based Health Insurance schemes (CBHIs) [78]. Through iterative rounds of an exercise named ‘Choosing Healthplans All Together’ (CHAT), we observed an enhanced level of consensus among participants. This repeated cycle of consultation and pricing adjustments led us to describe the process as ‘Collaborative and Contributive.’ Importantly, our evidence underscores that group consensus does not emerge spontaneously but necessitates a catalyst, as referenced in the source [79].

This notion resonates with the hypothesis suggesting that microinsurance becomes a viable business model tailored to match the affordability, needs, and priorities of groups within the informal sector [80]. The insurance industry is yet to fully accept the potential consequences of its ambition to harness and carve a market foothold at the base of the economic pyramid. This perspective provides a novel lens to understand how ‘micro’ insurance differentiates itself from traditional insurance. The following section delves further into this concept and presents empirical evidence.

2.3 Collaborative strategies to meet the requirements of low-income populations

The approach’s fundamental principles are rooted in historical wisdom and lessons from contemporary social movements. The first principle, captured by the rallying cry “No Taxation Without Representation” during the American Revolution, asserts that those contributing money should have a say in how to use it [81]. This democratic maxim is echoed in the “Collaborative and Contributive” (C&C) concept of microinsurance, underscoring the crucial link between citizen participation in governance and financial contributions [79]. This principle of collective-choice arrangements mirrors one of Elinor Ostrom’s design principles for managing common-pool resources [42], emphasizing that most individuals affected by the operational rules can participate in modifying the rules. Microinsurance distinguishes itself by focusing on customizing insurance offerings to local, regional, and national needs. Such customization is achieved through consultation and pooling resources among specific groups, echoing the principle of group solidarity [82, 83]. This principle, resonant with Ostrom’s ideas, promotes cooperative efforts and shared responsibility over isolated individual actions. At the core of solidarity is the spirit of cooperation, wherein individuals or groups band together to assist each other, particularly during challenging times, and work towards shared goals. This collective approach aligns with Ostrom’s design principle of congruence between rules and local conditions.

The belief that collective action and shared responsibility typically yield more fruitful outcomes than individual, isolated efforts has been demonstrated across various initiatives [84]. This ethos is a guiding principle from community-led social movements to cooperative economic models and microinsurance [85]. Drawing from Ostrom’s rules for clearly defined boundaries, the C&C approach to microinsurance defines the group as the unit to be insured, establishing a collaborative environment for managing shared risks.

Empirical evidence shows that addressing non-price barriers, such as trust issues and limited awareness, necessitates changes in contract designs, grassroots governance, and financial education [86, 87]. Reflecting Ostrom’s principle of monitoring, the C&C approach advocates for the insured group’s participation in managing the scheme, fostering transparency and trust.

The need for community involvement and education is increasingly emphasized [63, 88, 89]. Hence, microinsurance distinguishes itself from traditional insurance through a unique business process that interlinks customers’ contributions and active participation in decision-making. This participatory decision-making aligns with Ostrom’s principles for managing common-pool resources, underscoring the necessity of nested enterprises and minimal recognition of rights to organize. The C&C model recognizes the group’s right to organize and manage their insurance scheme, which can be nested within larger structures for greater risk pooling and resilience.

2.4 Actuarial techniques to meet the requirements of low-income populations

Bernards [90] emphasizes the concerted efforts of various entities to develop actuarial practices suitable for microinsurance operations, with a particular focus on non-agricultural sectors. Main contributors to these efforts include the International Association of Insurance Supervisors (IAIS), the International Actuarial Association (IAA), private consultancies, and the Microinsurance Centre (MIC).

Responding to encouragement from CGAP and the World Bank in the late 2000s, the IAA established the Microinsurance Working Group (MiWG) in 2010. In 2014, MiWG released an issue paper that suggested a proportional approach to regulations given the simpler nature, scale, and scope of microinsurance products [91].

Furthermore, in collaboration with IAIS and A2ii, the IAA created guidance and training materials to establish minimum actuarial standards in microinsurance operations [92]. The IAA also advocated for ‘formula-based approaches’ to actuarial calculations. This led to the creation of simplified pricing models for credit-life insurance and health microinsurance in 2012 and 2016, respectively [93, 94]. These models use accessible software platforms and publicly available data, allowing firms to set premium rates based on demographic data, country conditions, expected profit levels, expenses, and subsidies (if available).

Nevertheless, despite these strategic efforts, the impact on field operations remains limited. The primary barrier to effective implementation is not the lack of actuarial support but the prevailing socioeconomic dynamics among rural and informal sector workers.

3. The original idea of the ‘collaborative and contributive’ (C&C) model

The Collaborative and Contributive (C&C) model captures more than its “customer-centric” and “demand-driven” approach to group insurance. This model underscores that insurance is not merely a commercial product but an empowerment tool for communities and a safeguard for affiliated members. The C&C approach pivots around peer-to-peer dialogs, where local adults engage in discussions to determine which risks should be prioritized in that location for management and the acceptable cost calculated by external experts like actuaries. These collaborative discussions build consensus, fostering the willingness to join and pay.

The C&C strategy triggers demand, even among those typically excluded from or resistant to insurance, by converging three crucial aspects: the power of group discussions on prioritized risks, the importance of catalyzing consensus on cost and benefits, and the critical role of group members in administering the plan.

Regarding group discussions, these have proven to significantly broaden members’ understanding of the implications of insurance, empowering them and building their capacity to negotiate with insurers on behalf of the group. It fosters a sense of collective bargaining, a potent counterpoint to the feeling of powerlessness, or lack of agency an individual might experience when pitted against an imposing insurance company.

Concerning the package design, the C&C model champions a symbiotic relationship where the collective group acts as an ‘insurer’ while individual members are exposed to risk. This model greatly emphasizes customers’ active role in designing and pricing insurance packages that are context specific. Unlike the offering of low-cost, low-coverage products, this process leverages existing informal support and risk-sharing networks within the group, resulting in products tailored to their intimate knowledge of each other’s needs. Although we focus on health insurance, the C&C process has been successfully applied across various risk categories—including health, life, livestock, crop, and assets—employing indemnity and parametric models.

Local administrative participation provides three key advantages. First, it fills information gaps, mitigating the risk of failures. Second, it eases the claim submission process at the local level, aiding individuals who might struggle with form completion or providing required information. Finally, it delegates the disbursement of pooled funds to a committee selected from the group members, bolstering trust through this direct control over the group’s resources.

These three aspects significantly quell individual reticence, offering a more appealing alternative to the isolated experience of facing an insurance salesperson without a supportive network.

It’s important to note that the C&C model is distinct from Collaborative Learning Networks (CLN) [95] or “communities of practice” (CoP). The latter entails the exchange of insights, best practices, and new knowledge between individuals from different locations or even countries who share a common interest or concern. While these practices have been helpful in many fields and are gaining traction in global development as innovative technical assistance models, they fundamentally differ from the C&C approach. The focus of CLN or CoP is more on leveraging adult learning theories and social learning principles to develop sustainable systems. The C&C approach directly tackles the challenges of extending insurance coverage in a specific locality in a participatory manner.

3.1 The C&C model facilitates the transition from dormant to solvent demand

Dror ([89], chapter 1) advances that in the settings of poverty and informality, humans pursue the objectives and priorities of groups to which they belong, established through iterative exchanges to reach a consensus on “what a responsible adult does” [79, 80, 96]. This assumption posits that individuals align with their support group rather than conducting an individual risk assessment. This assumption challenges the centrality of Von Neumann and Morgenstern’s proposition that insurance offers a solution for personal risk aversion [97] or Kahneman and Tversky’s theory regarding

The margin of individual decision-making on financial matters is limited in quantity and scope. The limited quantity is a function of low disposable cash reserves. The limit in scope is that each spending comes at the expense of other alternatives, i.e., an exercise in rationing that can influence other household members and therefore requires prior consultation with the family, extended family, and the group that provides the support in case of need. Dror et al. [88] provide evidence of success in establishing the consensus that “insurance is what responsible adults in our setting/community do.” The flip side of this process is that when there is no consensus (or no discussion), many or most uninsured individuals in poverty and informality express dormant rather than solvent demand for insurance.

Dormant demand describes the attitude of consumers who do not consider the merits of the products on offer. Their battle cry is irrefutable: “

3.2 The transformative effect of the C&C model: nurturing dependability over dependency

Informal sector workers often develop a dependent mentality, anticipating the management of unexpected risks to fall upon others. For instance, during calamities such as epidemics, floods, droughts, or earthquakes, the larger population, including those in developing countries, expects the government to intervene using public funds. This expectation perhaps stems from the coexistence of public services (horizontal systems) and targeted programs for specific conditions (vertical programs), like control of HIV/AIDS, tuberculosis, malaria, COVID, and maternity issues. These horizontal systems and many vertical programs often offer services at no cost and occasionally provide monetary incentives for compliance.

This ingrained practice indicates that the government is responsible for risk mitigation, not the individual at risk. Shifting this paradigm requires moving from a dependency mentality to one of dependability. Community-Based Health Insurance (CBHI) initiatives exemplify such a shift’s effectiveness. Often burdened with caregiving duties without sufficient resources, women have been empowered through participation in the administration, governance, and oversight of pooled funds via CBHI schemes [101, 102]. Women involved in Self-Help-Groups and CBHI [103] emphasized the empowerment gained from having a say in their healthcare decisions for the first time. This transition from dependency to dependability, often expressed with immense satisfaction, can be seen as one of microinsurance’s most significant indirect benefits.

3.3 Insurance education as a catalyst for financial inclusion: insights from the C&C model

In the informal sector, it is difficult to start a dialog on any topic dealing with finance or insurance because most people associate those topics with exclusion rather than inclusion. Shifting the paradigm from exclusion to inclusion begins with people’s shared understanding that inclusion entails a benefit and that the terms to avail of that benefit are reasonable. Discussion, consensus building, and dialog lead to understanding the basic concepts [104]. A universe of discourse then leads to cultural acceptance of the financial instrument and only then to participation. Reaching this cultural acceptance requires insurance education and financial literacy, not a sales pitch [105]. However, to this day, there is no generalized recognition that it is necessary to impart insurance education to grassroots groups. Neither governments nor the insurance industry has invested the resources in developing the curriculum or the required institutional support to impart large-scale insurance education [106]. Governments, NGOs, or insurers wishing to improve financial inclusion should start by enhancing financial/insurance education [107]. Integrating insurance literacy into primary education could serve as a valuable strategy, allowing children to grasp and reinforce these essential concepts at home [108]. For adults, the group setting proves most effective for learning and accepting insurance literacy, particularly when engaging with community peers [63].

3.4 Impact of being insured

The impact of insurance signifies both the tangible and intangible shifts experienced by an insured individual, household, or community. It encompasses financial stability, risk management, improved health and well-being, poverty reduction, economic growth, and increased resilience to unexpected shocks or disasters. The impact is gauged through numerous indicators, among which the changes in financial status, service usage, socioeconomic variables, and overall quality of life stand out. A direct and significant metric is the claims ratio (loss ratio)—the percentage of premiums paid out as benefits.

The Landscape of Microinsurance Study 2022 [109] is the most extensive publication, with data from 253 insurance providers reporting on 935 diverse products in 34 countries across Africa, Asia, Latin America, and the Caribbean. The study presents a microinsurance landscape, providing insights into the market size, evolution, premiums, product development, social performance, reinsurance, and claims. The research reveals that total premiums have doubled from USD 1.1 billion in 2020 to USD 2.2 billion in 2021, although the number of people covered has decreased in the same period. The study highlights that microfinance institutions, financial institutions, and agents & brokers are the most active distribution channels.

In 2021, life and accident insurance products saw a median claims ratio of 22%, a slight rise from 18% the previous year, although with regional differences. Such low claims ratios could potentially heighten the insured’s vulnerability given the relative premium costs, contradicting the purpose of insurance. Agricultural products had a higher median claims ratio of 28%, which saw significant regional variations. Unfortunately, the study lacked information on the health microinsurance claims ratio.

Insurers typically aim to strike a balance in their claims ratio. If it’s too high, it might indicate underpricing of risks, potentially leading to financial challenges. Conversely, a meager ratio might suggest overpricing, delivering less value to policyholders, or possibly that policyholders aren’t claiming even when eligible. The observed claims ratios for the given year lean towards the lower end, prompting questions about allocating the unclaimed premium funds. It’s plausible (though not explicitly mentioned) that a portion of the premium income is set aside for “technical” and “solvency” reserves—both of which are crucial. It’s imperative to differentiate between profits and reserves transparently. Moreover, a longer-term accounting perspective is essential. However, if a significant portion of these funds is reserved as profits, it may indicate that the premiums are potentially overpriced, further exacerbating concerns about pricing and trust.

Another way to evaluate the impact of community-based health insurance (CBHI) is by analyzing empirical data on healthcare utilization and financial risk protection in low- and middle-income countries (LMICs). A recent systematic review [110] provided insights into this, examining 61 studies that represented the experiences of 221,568 households (equivalent to 1,012,542 individuals) across 20 LMICs. The key takeaway is that CBHI schemes have considerably boosted healthcare utilization, with a pronounced emphasis on outpatient services. Of the 43 studies reviewed, 24 identified a tangible improvement in financial risk protection due to CBHI. When collated, the data indicated that insured households leaned more towards healthcare utilization, outpatient services, and health facility deliveries. Yet, there was no significant uptick in inpatient hospitalizations. Financially, CBHI-affiliated households reported a decrease in out-of-pocket health expenses and a reduced likelihood of encountering catastrophic health expenditures, gauged at 10% of total household expenditures and 40% of non-food expenditures. To sum up, CBHI effectively enhances healthcare utilization in LMICs but offers inconsistent financial protection against unexpected health-related expenses.

4. Challenges in implementing the C&C model and ensuring scalability

4.1 Tackling the critical obstacles to microinsurance sustainability and scalability

The potential of the C&C Microinsurance model to extend social protection coverage for vulnerable and marginalized populations is substantial. However, to harness this potential effectively, it is vital to understand and address the model’s inherent challenges. Here are the primary hurdles:

4.1.1 Limited financial literacy and awareness

The complexity of insurance concepts and a lack of understanding of the benefits of microinsurance often inhibit its adoption. Financial education should aim at shaping decisions rather than just imparting information. Hence, targeted financial literacy initiatives, which lay the foundation for the ‘Collaborative’ aspect of C&C, should be introduced before premium solicitation. Such initiatives are most effective when they involve trusted community figures and peers, capturing hearts and minds.

4.1.2 Affordability

Affordability can be enhanced through innovative pricing structures, such as aligning certain payments with periods when farmers sell their produce instead of demanding upfront premiums. Additionally, devising group policies for entire communities and bundling various risk categories into a comprehensive approach may allow for cross-subsidization, further addressing affordability concerns.

4.1.3 Delivery and administration challenges

The large-scale implementation of microinsurance, especially in rural settings, brings significant logistical challenges. Partnering with local institutions, like microinsurance-focused village committees, can help mitigate these difficulties. At the same time, digitizing processes can improve operational efficiency, reduce paperwork and redundancies, and expedite response times. However, given the limited interest shown by finance capital [90], the onus of developing microinsurance markets falls mainly upon the initiating organizations. This emphasizes the need for intentional market creation and demand stimulation [88] over spontaneous evolution. High administrative costs, particularly during limited outreach, further compound these challenges. As an aside, it’s pertinent to note that the administrative costs associated with health insurance are frequently substantial, as underscored by studies like [111]. Similarly, Community-Based Health Insurance (CBHI) schemes also grapple with high administrative costs due to the group’s small size, rendering premiums insufficient to finance administrative costs in the early years of operation.

4.1.4 Risk of fraud or mismanagement of pooled funds

Microinsurance operators managing pooled funds face significant financial risks due to weak internal controls and governance [98]. However, establishing more effective controls often leads to increased costs.

4.1.5 Risk pooling and sustainability

Small or homogeneous risk pools can jeopardize the sustainability of the microinsurance program. The pooling of various groups, introducing diversified products, and including reinsurance [112] can help broaden and diversify the risk pool.

4.1.6 Regulatory environment

A supportive regulatory environment can propel the growth of microinsurance. It is incumbent upon governments to develop regulations that encourage innovation in the microinsurance sector while ensuring consumer protection.

4.1.7 Data availability and pricing

The lack of reliable granular data for local risk assessment and pricing can diminish the effectiveness of microinsurance. Collaborations between implementers and research institutions and using advanced technologies for local data collection and analysis can improve data management.

4.1.8 Product design

Microinsurance products must align with the specific needs of target populations. This necessitates a user-centric design process and ongoing feedback mechanisms for product refinement.

4.1.9 Low claims ratio

A low claims ratio may suggest the insured group is not reaping benefits commensurate with their premium payments. This might be due to restrictive policy conditions, a lack of awareness about the claims process, high deductibles that discourage individuals from making claims, and overly conservative risk assessments. Addressing these issues requires a reassessment of the terms to ensure they are fair and not overly restrictive and enhance transparency and simplicity in the claims process.

4.1.10 Dependence on continued external technical assistance

As highlighted by Schmidt et al. [113], dependency on external technical assistance presents a significant challenge. Ensuring a smooth transition to sustainable solutions without compromising technical performance standards constitutes a substantial task.

Addressing these challenges necessitates coordinated action from multiple stakeholders, including governments, microinsurance providers, NGOs, local community organizations, and insured groups. By confronting these issues, we can more effectively unlock the potential of the C&C Microinsurance model, thereby broadening its impact in extending social protection to those who need it most.

4.2 Long-term investment and reinsurance for scaling microinsurance

In the early stages of microinsurance development, proponents recognized that the advantages of small mutual aid groups also presented challenges in risk diversification and covariance. The solution suggested was “Social Reinsurance,” a concept to provide reinsurance for Micro Insurance Units (MIUs) [112].

The primary advantage of reinsurance is its ability to offer solvency protection. By distributing risk among multiple entities, reinsurance safeguards insurance providers from insolvency due to significant claim events, such as natural disasters [114].

In addition to this vital role, reinsurance’s value proposition lies in its capacity to extend coverage beyond insurers’ risk-bearing abilities, protecting a broader pool of clients [114]. In a commercial context, the stabilizing impact of reinsurance on underwriting results—achieved by reducing the variability of an insurer’s loss ratio—renders financial outcomes more predictable and appealing to investors [115].

Reinsurance also plays an essential role in capacity enhancement. By providing access to global reinsurance markets, insurers, particularly those operating in developing countries, can offer products and services that might otherwise exceed their risk-bearing capacity [116].

In commercial insurance contexts, additional benefits of reinsurance include capital management. It offers a form of contingent capital that can be mobilized in the event of substantial losses, thus reducing the amount of money required to underwrite insurance [115]. Furthermore, reinsurers often provide underwriting, pricing, and claims management expertise and support, which is particularly valuable for primary insurers in niche sectors where such expertise may be limited [116].

The proposed concept of Social Reinsurance intended to bolster Microinsurance Units (MIUs) did not materialize. A subsequent proposal about the role of reinsurance in microinsurance [117] also did not progress. A primary reason for this lack of advancement lies in the regulations governing reinsurance businesses in many countries, which permit only licensed insurance companies to cede risks to reinsurance, leaving community-based microinsurance entities unable to do so. This restriction raises an important question: how much capital is necessary for such schemes to scale their services? The answer to this question was sought in a 2019 research paper [118]. The researchers used algorithms to calculate capital requirements for expanding health microinsurance for poor rural populations.

They found that to offset early losses, a prototype plan serving 40,000 people in India would need an initial funding of USD 62,477 if long-term operating costs would not exceed 20% of the premium and the claims ratio would stabilize at around 70%.

Not surprisingly, when the confidence levels were decreased below 99.9%—meaning a greater level of risk was accepted that the prototype plan might not stay solvent throughout a year—the capital requirements diminished significantly. Based on the researchers’ calculations, a grace period of 5 years would be followed by a 15-year repayment period to compensate the investors who provided the initial funding entirely with an annual interest rate of 5% in USD.

Based on these findings, the study suggests that health microinsurance programs can achieve sustainability by providing the necessary initial capital as a loan and closely monitoring five key parameters: enrollment, premiums, operating costs, renewal rates, and the claims ratio.

The per-person, per-year capital requirement is strikingly low. The study’s assumptions of a 15-year loan period and a commercial interest rate imply that if investors could be attracted, it would be feasible to significantly scale up microinsurance as a development project, even without reinsurance. However, the ideal way to scale microinsurance for a more significant impact would be through reinsurance, which offers the advantage of capacity enhancement and other benefits. Yet, this opportunity likely depends on the support of governments or development banks like the World Bank and the engagement of the reinsurance industry to agree to transact with small insurance entities like MIUs.

5. Conclusion

The glaring issue that spurred the development of microinsurance is universally recognized: approximately half of the global population is bereft of access to social protection. The traditional top-down Bismarckian and Beveridgean models fail to make strides in most low- and middle-income countries due to evident and justifiable reasons. As the informal sector burgeons and several labor-intensive industries become hubs of informal employment, the call for an innovative operative model rings more urgent than ever.

While it’s evident that past efforts to frame and deliver microinsurance as “insurance for the poor” or “low-cost, low coverage” insurance have fallen short of their intended goals, these attempts have provided valuable lessons. They revealed the complex dynamics that shape the demand for microinsurance and its effectiveness, from financial constraints to customers’ risk priorities and other demand drivers, claims ratios, and renewal rates.

Despite the limitations of multilateral and international organizations in establishing robust insurance infrastructure in informal settings, their role in gathering insights from various pilots—successful or otherwise—cannot be understated. Even though such efforts, including the provision of ‘distance insurance literacy,’ have not yet fully reached or impacted the informal sector, they are steps in the right direction. Each effort brings us closer to realizing the potential of microinsurance in contributing to welfare gains at the grassroots level. The wealth of data and experience offers a significant foundation for building new strategies.

This strategic approach to scaling microinsurance, aka ‘anticipatory marketization,’ should include establishing more granular data sources, insurance education at the grassroots level, and adapting business practices by commercial insurers to better align with the needs of the community-based market.

Moreover, the few initiatives taken by some donors and philanthropic bodies have exposed a critical insight: microinsurance is more than just a financial transaction. It operates within a nexus of political and social dynamics, which must be considered for successful implementation.

Maintaining a positive outlook in the face of challenges is crucial. In an era where public trust in “the system” is eroding, the answer is not merely to preach faith in the benevolence of top-down or profit-driven insurers. The growing inequality in wealth, income, political influence, and access to justice underscores that simply declaring noble intentions is insufficient. Mandatory enrolment, a hallmark of the Bismarckian model, has not been well-received in many countries, proving it’s not the ultimate solution. Despite this, each field experience, whether failed or successful, has yielded valuable insights, shaping a more inclusive and effective microinsurance sector. This is indeed progress. Yet, much more must be done to stimulate appropriate investments in ‘anticipatory marketization.’

The way forward lies in the realization that when social forces are more potent and actionable than market forces, the fitting path forward involves leveraging these social dynamics to catalyze demand. Microinsurance, rooted in mutual aid, thrives in small group settings, fostering open dialog and consensus on risk insurance and resource allocation for risk management. The tireless efforts of pioneers and NGOs for a generation to validate an unconventional demand theory have led to an abundance of field pilots and evidence-backed publications. What does this collective wisdom tell us? A viable alternative path to reaching the uninsured does exist, one paved with the power of collaboration, cooperation, consultation, and consensus-building, fueling willingness to join and pay. Scaling this transformative model necessitates resources, regulatory backing, and institutional support, much like any groundbreaking development project. It’s high time we rally politicians, bankers, and reinsurers to pool their resources and ambitions and tether them to this pioneering social protection model.

The pursuit of developing microinsurance markets and the persistent efforts to troubleshoot and re-engineer those markets represent complex attempts to develop forms of social protection that do not necessitate substantial redistribution. Is this a deal-breaker?

The evidence suggests that the excluded groups neither expect nor demand that insurance delivers substantial income redistribution. However, they insist on participatory decision-making. This expectation can be met by applying the “Collaborative and Contributive” (C&C) microinsurance model. This approach emphasizes inclusion and empowerment of everyone—whether employed or not, engaged in formal or informal work, and residing in urban or rural areas—to participate in insurance decision-making. This represents a dramatic departure from the authoritarian style of state-owned schemes or the rigid and obfuscated operations of commercial insurance.

Despite its potential, the C&C model encounters several obstacles, including regulatory impediments like limitations on transferring risks to reinsurance and insufficient political and financial backing needed to generate impact on a large scale.

However, the past quarter-century has seen significant strides in evolving demand theory and establishing operational frameworks for mutual aid microinsurance schemes, such as Community-Based Health Insurance (CBHI). Thanks primarily to NGOs, pioneering practitioners, and a handful of countries that have adopted CBHI as the national system, these experiments have catalyzed a willingness to join, pay actuarially fair premiums, and participate in governance and administration. Now, it’s time for the academic community to examine microinsurance’s social and economic impacts, including its potential contribution to GDP growth by insuring informal workers and the welfare gains to the insured. Most importantly, it’s time for ‘development politicians’, prudent bankers—particularly international development bankers—and the reinsurance industry to back the C&C microinsurance model’s potential to extend insurance to all, using models that transcend Bismarck and Beveridge’s models.

Acknowledgments

The author would like to sincerely acknowledge the invaluable review comments offered by Prof. Martin Eling, Dr. Nihar Jangle, and Mr. John Woodall. Their constructive feedback has significantly enhanced the quality of this work. However, any assertions or conclusions drawn in this article are the sole responsibility of the author.

References

- 1.

International Labour Office. World Social Protection Report 2020-22. Vol. 1. Geneva: ILO; 2021, Online resource, 377 p. ISBN 978-92-2-031950-5. Available from: https://www.ilo.org/global/about-the-ilo/newsroom/news/WCMS_817653/lang--en/index.htm - 2.

Hart K. Informal income opportunities and urban employment in Ghana. The Journal of Modern African Studies. 1973; 11 (1):61-89 - 3.

International Labour Office. Employment, Incomes, and Equality: A Strategy for Increasing Productive Employment in Kenya. Geneva: ILO; 1972 - 4.

Point 2 of the FAQ Defines the Term “Inclusive Insurance.” Available from: https://a2ii.org/en/FAQs - 5.

Wachinger G, Renn O, Begg C, Kuhlicke C. The risk perception paradox—Implications for governance and communication of natural hazards. Risk Analysis. 2013; 33 (6):1049-1065 - 6.

Dionne G. Risk management: History, definition, and critique. Risk Management and Insurance Review. 2013; 16 (2):147-166. DOI: 10.2139/ssrn.2231635 - 7.

Wilkie D. Mutuality and solidarity: Assessing risks and sharing losses. Philosophical Transactions of the Royal Society of London. Series B: Biological Sciences. 1997; 352 (1357):1039-1044 - 8.

Banerjee AV, Duflo E. Good Economics for Hard Times. New York: Public Affairs; 2019 - 9.

Giesbert L, Steiner S. Client perceptions of the value of microinsurance: Evidence from southern Ghana. The Journal of Development Studies. 2015; 51 (7):869-884 - 10.

Mader P. Microfinance and financial inclusion. In: The Political Economy of Microfinance. Cham: Palgrave Macmillan; 2018. pp. 99-123 - 11.

Almgren G. Health care systems: Four basic models. In: Health Care Politics, Policy, and Services: A Social Justice Analysis. 3rd ed. New York: Springer Publishing Company; 2018. pp. 78-82 - 12.

Leisering L. Nation state and social policy: An ideational and political history. In: Social Policy in the Federal Republic of Germany. 2013. pp. 1-22 - 13.

Abel-Smith B. The Beveridge report: Its origins and outcomes. International Social Security Review. 1992; 45 (1-2):5-16 - 14.

Hills J, Sefton T, Stewart K, editors. Towards a more Equal Society? Poverty, Inequality, and Policy since 1997. Bristol: The Policy Press; 2009. Available from: https://publications.iadb.org/publications/english/document/Microinsurance-Risk-Protection-for-the-Poor.pdf - 15.

Hamel MB, Blumenthal D, Collins SR. Health care coverage and the affordable care act—A progress report. The New England Journal of Medicine. 2014; 371 :275-281. DOI: 10.1056/NEJMp1406857 - 16.

Rowland D, Telyukov AV. Soviet health care from two perspectives. Health Affairs. 1991; 10 (3):71-86. DOI: 10.1377/hlthaff.10.3.71 - 17.

Palmer N. The use of private-sector contracts for primary health care: Theory, evidence, and lessons for low-income and middle-income countries. Bulletin of the World Health Organization. 2000; 78 :821-829 - 18.

Oberlander J. The US healthcare system: An international perspective. Daedalus. 2003; 132 (3):32-41 - 19.

Ostrom E. Beyond markets and states: Polycentric governance of complex economic systems. American Economic Review. 2010; 100 (3):641-672 - 20.

Ruckert A, Labonté R. The global financial crisis and health equity: Early experiences from Canada. Globalization and Health. 2014; 10 (1):2 - 21.

Tumwine G, Palmieri J, Larsson M, Gummesson C, Okong P, Östergren PO, et al. ‘One-size doesn’t fit all’: Understanding healthcare practitioners’ perceptions, attitudes and behaviors towards sexual and reproductive health and rights in low resource settings: An exploratory qualitative study. PLoS One. 2020, 2020; 15 (6):e0234658. DOI: 10.1371/journal.pone.0234658 - 22.

Harrison A, Scorse J. Multinationals and anti-sweatshop activism. American Economic Review. 2010; 100 (1):247-273 - 23.

Barrientos A, Hulme D. Social protection for the poor and poorest in developing countries: Reflections on a quiet revolution. Oxford Development Studies. 2008; 37 (4):439-456 - 24.

International Labour Organization (ILO). Social Security (Minimum Standards) Convention. Vol. 102. Geneva: ILO; 1952 - 25.

International Labour Organization. Introduction to Social Security. Geneva: ILO; 1984 - 26.

ILO. World Labour Report 2000: Income Security and Social Protection in a Changing World. Geneva: International Labour Office; 2000 - 27.

van Ginneken W. Extending social security: Policies for developing countries. International Labour Review. 2003; 142 (3):277-294 - 28.

International Labour Organization (ILO). World Social Protection Report 2017-19: Universal Social Protection to Achieve the Sustainable Development Goals. Geneva: ILO; 2017 - 29.

International Labour Organization. Recommendation Concerning National Floors of Social Protection. Geneva: ILO; 2012. Available from: https://www.ilo.org/dyn/normlex/en/f?p=NORMLEXPUB:12100:0::NO::P12100_INSTRUMENT_ID:3065524 - 30.

International Labour Organization. The ILO’s Flagship Programme: Building Social Protection Floors for All. Geneva: ILO; 2016. Available from: https://www.ilo.org/global/topics/social-security/WCMS_490725/lang--en/index.htm - 31.

World Health Organization. Microinsurance for Health: A Unique Social Protection Measure. Geneva: WHO; 2017 - 32.

Dror DM. Demand for health insurance in emerging Asia. Health Economics, Policy and Law. 2018; 13 (3-4):408-429 - 33.

Usage and publication rights to content from the free infographics service are granted under a Creative Commons (CC) license. Available from: https://www.statista.com/chart/30347/share-of-informal-employment-by-sex-and-selected-sectors/ - 34.

Best J. Ambiguity and uncertainty in international organizations: A history of debating IMF conditionality. International Studies Quarterly. 2013; 57 (4):674-688 - 35.

International Labour Organization. Social Security Principles. Geneva: International Labour Office; 1977 - 36.

International Labour Organization. Extending Social Security Coverage. Geneva: International Labour Office; 1980 - 37.

International Labour Organization. Approaches to Social Protection: An International Review. Geneva: International Labour Office; 1989 - 38.

Sen A. Rights and agency. Philosophy & Public Affairs. 1982; 11 :3-39 - 39.

Sen A. Poor, relatively speaking. Oxford Economic Papers. 1983; 35 (2):153-169 - 40.

Sen A, Drèze J. India: Economic Development and Social Opportunity. Oxford: Oxford University Press; 1995 - 41.

Mouton Y, Gruat JV. Protection sociale dans les pays en développement: Alternatives pour les secteurs non structurés. Travail et Société. 1989; 14 (2):265-289 - 42.

Ostrom E. Governing the Commons: The Evolution of Institutions for Collective Action. Cambridge: Cambridge University Press; 1990 - 43.

van Ginneken W. Meeting social needs in developing countries. International Labour Review. 1996; 135 (6):615-625 - 44.

Dror DM, Jacquier C. Microinsurance: Extending health insurance to the excluded. International Social Security Review. 1999; 52 (1):71-97 - 45.

Dror DM, Piesse D. What is microinsurance? In: Radermacher R, Roth K, editors. A Practical Guide to Impact Assessments in Microinsurance. Luxemburg and New Delhi: Microinsurance Network and Micro Insurance Academy; 2014. pp. 24-39 - 46.

McCord MJ. The Microinsurance Product and its Pricing. Vol. 3. Appleton, Wisconsin, USA: Micro Insurance Centre Briefing Note; 2001 - 47.

Churchill C. What is insurance for the poor? In: Churchill C, editor. Protecting the Poor: A Microinsurance Compendium. Geneva: International Labour Office and Munich Re Foundation; 2006 - 48.

Roth J, McCord MJ, Liber D. The Landscape of Microinsurance in the World’s 100 Poorest Countries. Appleton, Wisconsin, USA: The Micro Insurance Centre; 2007 - 49.

Churchill C, McCord MJ. Current trends in microinsurance. In: Churchill C, Matul M, editors. Protecting the Poor: A Microinsurance Compendium. Vol. 2. Geneva: ILO; 2012. pp. 8-39 - 50.

Preker AS, Scheffler RM, Bassett MC. Private Voluntary Health Insurance in Development: Friend or Foe? Washington DC: The World Bank; 2007 - 51.

Thaler RH, Sunstein CR. Nudge: Improving Decisions about Health, Wealth, and Happiness. New Haven, CT: Yale University Press; 2008 - 52.

Sen A. Development as Freedom. Oxford: Oxford University Press; 1999 - 53.

Matul M, McCord MJ, Phily C, Harms J. The landscape of microinsurance in Africa. In: Microinsurance Innovation Facility Research Paper No. 4. Geneva: International Labour Organization; 2010 - 54.

Churchill C, Matul M. Protecting the Poor: A Micro Insurance Compendium. Vol. II. Geneva: International Labour Organisation; 2012 - 55.

Wipf J, Garand D. Performance Indicators for Microinsurance: A Handbook for Microinsurance Practitioners. 2nd ed. Luxemburg: ADA asbl, Microinsurance Network, and BRS; 2010 - 56.

Cohen M, Young M. Microinsurance: Innovating to meet the needs of the poor. In: Making Insurance Work for Microfinance. Washington, DC: Micro Finance Network; 2007. pp. 9-31 - 57.

Sen A. Commodities and Capabilities. Amsterdam: North-Holland; 1985 - 58.

Sen A. Gender and cooperative conflicts. In: Tinker I, editor. Persistent Inequalities: Women and World Development. Oxford: Oxford University Press; 1990 - 59.

McCord M, Osinde S. Reducing vulnerability: The demand for microinsurance. Journal of International Development. 2005; 17 (3):377-385 - 60.

Churchill C. Making Insurance Work for Microfinance: Institutions, Products, and Country Experiences. Geneva: ILO Microinsurance Innovation Facility; 2007 - 61.

Radermacher R, Brinkmann V. The Importance of Pricing in Microinsurance: Principles and Case Studies. Luxemburg: Microinsurance Network; 2011 - 62.

Cohen M, Young M. Microinsurance: The risks, perils, and opportunities. Small Business Economics (New York: Springer). 2007; 28 (1):113-116 - 63.

Cole S, Giné X, Tobacman J, Topalova P, Townsend R, Vickery J. Barriers to household risk management: Evidence from India. American Economic Journal: Applied Economics. 2013; 5 (1):104-135 - 64.

Thornton RL, Hatt LE, Field EM, Islam M, Solís Diaz F, González MA. Social security health insurance for the informal sector in Nicaragua: A randomized evaluation. Health Economics. 2010; 19 (S1):181-206 - 65.

Clarke DJ. A theory of rational demand for index insurance. American Economic Journal: Microeconomics. 2016; 8 (1):283-306 - 66.

Giné X, Townsend R, Vickery J. Patterns of rainfall insurance participation in rural India. The World Bank Economic Review. 2008; 22 (3):539-566 - 67.

Casaburi L, Willis J. Time versus state in insurance: Experimental evidence from contract farming in Kenya. American Economic Review. 2018; 108 (12):3778-3813 - 68.

Bauchet J, Morduch J. Paying in pieces: A natural experiment on demand for life insurance under different payment schemes. Journal of Development Economics. 2019; 139 :69-77 - 69.

Elabed G, Carter MR. Compound-risk aversion, ambiguity, and the willingness to pay for microinsurance. Journal of Economic Behavior & Organization. 2015; 118 :150-166 - 70.

Belissa TK, Lensink R, van Asseldonk M. Risk and ambiguity aversion behavior in index-based insurance uptake decisions: Experimental evidence from Ethiopia. Journal of Economic Behavior & Organization. 2020; 180 :718-730. Available from:https://www.sciencedirect.com/science/article/pii/S0167268119302380 - 71.

Dror DM, Hossain SAS, Majumdar A, Pérez Koehlmoos TL, John D, Panda PK. What factors affect voluntary uptake of community-based health insurance schemes in low- and middle-income countries? A systematic review and meta-analysis. PLoS One. 2016; 11 (8):e0160479. DOI: 10.1371 - 72.

Platteau JP, De Bock O, Gelade W. The demand for microinsurance: A literature review. World Development. 2017; 94 :139-156 - 73.

Akweongo P, Aikins M, Wyss K, et al. Insured clients’ out-of-pocket payments for health care under the national health insurance scheme in Ghana. BMC Health Services Research. 2021; 21 :440. DOI: 10.1186/s12913-021-06401-8 - 74.

Fung V et al. The affordability of individual-market health Insurance in California under the American rescue plan act, 2021. Health Affairs. 2023; 42/7 :1011-1020. DOI: 10.1377/hlthaff.2022.01419 - 75.

Leach R, Sitaram A. Micro-insurance in India: Insurance for the poor? The Journal of Alternative Perspectives in the Social Sciences. 2002; 4 (1):27-46 - 76.

Tellez CA, Zetterli P. Mobile insurance, savings, and credit. Focus Note. 2014; 96 :5-13 - 77.

Sundar A, Noseworthy TJ. Too exciting to fail, too sincere to succeed: The effects of brand personality on sensory disconfirmation. Journal of Consumer Research. 2016; 43 (1):44-67, Oxford University Press. Available from:https://ideas.repec.org/a/oup/jconrs/v43y2016i1p44-67..html - 78.

Dror DM, Panda P, May C, Majumdar A, Koren R. “One for all and all for one”: Consensus-building within communities in rural India on their health microinsurance package. Risk Management and Healthcare Policy. 2014; 2014 :139-153. DOI: 10.2147/rmhp.s66011 - 79.

Dror DM, Firth L. The demand for (micro) health insurance in the informal sector. The Geneva Papers on Risk and Insurance-Issues and Practice. 2014; 39 (4):693-712 - 80.

Dror DM. Financing Micro Health Insurance: Theory, Methods, and Evidence. Vol. 2. Singapore: World Scientific Publishing; 2018. p. 10944, World Scientific Series in Health Investment and Financing. ISBN 978-981-3238-47-3, 552 - 81.

Bailyn B. The Ideological Origins of the American Revolution. Cambridge, Massachusetts: Harvard University Press; 1992 - 82.

Kropotkin P. Mutual Aid: A Factor of Evolution. London: William Heinemann; 1902 - 83.

Ansell C, Gash A. Collaborative governance in theory and practice. Journal of Public Administration Research and Theory. 2007; 18 (4):543-571 - 84.

Lozano-Díaz A, Fernández-Prados JS. Young digital citizenship in #FridaysForFuture. Review of Education, Pedagogy, and Cultural Studies. 2022; 44 (5):447-468 - 85.

Birchall J, Ketilson LH. The Resilience of the Cooperative Business Model in Times of Crisis. Geneva: Sustainable Enterprise Programme, ILO; 2009 - 86.

Cai J, de Janvry A, Sadoulet E. Social networks and the decision to insure. American Economic Journal: Applied Economics. 2020; 2 (2):81-108 - 87.

Song C. Financial education and savings behavior: Evidence from a randomized experiment among low-income clients of branchless banking in India. Journal of Development Economics. 2020; 146 :102558 - 88.

Dror DM, Chakraborty A, Majumdar A. The effect of consensus on demand for voluntary micro health insurance in rural India. Risk Management and Healthcare Policy. 2018; 11 :139-158 - 89.

Dror DM. Health Microinsurance: Implementing Universal Health Coverage in the Informal Sector. Vol. 4. Singapore: World Scientific Publishing; 2020. World Scientific Series in Health Investment and Financing, ISBN 9789811208522 - 90.

Bernards N. Waiting for the market? Microinsurance and development as anticipatory marketization. Environment and Planning A: Economy and Space. 2022; 54 (5):949-965. DOI: 10.1177/0308518X221073986 - 91.

IAA. Actuarial Practices in Microinsurance. Ottawa: International Actuarial Association; 2014 - 92.

IAA. Actuarial Practices in Microinsurance. Ottawa: International Actuarial Association; 2018 - 93.

UKAP. Credit-Life Insurance Pricing Model. London: UK Actuarial Profession; 2012 - 94.

Milliman. Health Microinsurance Pricing Model. Seattle: Milliman; 2016 - 95.

Designing & Facilitating Collaborative Learning Net-works : A Toolkit. Published by Results for Development (Online). Available from: https://r4d.org/wp-content/uploads/R4D-Collaborative-Learning-Toolkit-DRAFT.pdf - 96.

Turner JC. Social Categorization and the Self-Concept: A Social Cognitive Theory of Group Behavior. Washington, DC: Psychology Press; 2010 - 97.

Neumann V, Morgenstern. Theory of Games and Economic Behavior. Princeton, NJ, USA: Princeton University Press; 1944. Republished by J. Wiley; 1967. ISBN 9780471911852, 0471911852 - 98.

Daniel K, Amos T. Prospect theory: An analysis of decision under risk. Econometrica. 1979; 47 (2):263-291. The Econometric Society. Available from:http://www.jstor.org/stable/1914185 - 99.

Sterne JA, Hernán MA, Reeves BC, Savović J, Berkman ND, Viswanathan M, et al. ROBINS-I: A tool for assessing the risk of bias in non-randomized studies of interventions. BMJ. 2016; 355 :i4919 - 100.

Hart SD, Michie C, Cooke DJ. Precision of actuarial risk assessment instruments: Evaluating the ‘margins of error’ of group v. individual predictions of violence. The British Journal of Psychiatry. 2007; 190 (S49):s60-s65 - 101.

Fletschner D, Kenney L. Rural Women’s access to financial services: Credit, savings, and insurance. In: Gender in Agriculture. Netherlands: Springer; 2014. pp. 187-208. DOI: 10.1007/978-94-017-8616-4_8 - 102.

Holtz J, Cox B, Cico A. Building Momentum for Universal Health Coverage: Communication and Advocacy in Action. Washington, DC: HFG Project, HFG Series: Advances in Health Finance & Governance; 2018. Available from: www.hfgproject.org - 103.

Mersland R, Nyarko SA, Szafarz A. Do social enterprises walk the talk? Assessing microfinance performances with mission statements. Journal of Business Venturing Insights. 2019; 11 :e00117. DOI: 10.1016/j.jbvi.2019.e00117 - 104.

Kumar N, Raghunathan K, Arrieta A, Jilani A, Hamza; and Pandey, Shinjini. The power of the collective empowers women: Evidence from self-help groups in India. World Development. 2021; 146 (2021):105579. DOI: 10.1016/j.worlddev.2021.105579 - 105.

Lusardi A, Mitchell OS. The economic importance of financial literacy: Theory and evidence. American Economic Journal: Journal of Economic Literature. 2014; 52 (1):5-44 - 106.

Lusardi A, Mitchell OS. Financial literacy around the world: An overview. Journal of Pension Economics & Finance. 2011; 10 (4):497-508 - 107.

Beyene HA. Factors affecting the sustainability of rural water supply systems: The case of Mecha Woreda, Amhara Region, Ethiopia [thesis]. Ithaca, NY, USA: Cornell University; 2012 - 108.

Lusardi A, Tufano P. Debt literacy, financial experiences, and over-indebtedness. Journal of Pension Economics & Finance. 2015; 14 (4):332-368 - 109.

Microinsurance Network. The Landscape of Microinsurance 2022. Luxembourg: Microinsurance Network; 2023. Available from: https://microinsurancenetwork.org/publications - 110.

Eze P, Ilechukwu S, Lawani LO. Impact of community-based health insurance in low- and middle-income countries: A systematic review and meta-analysis. PLoS One. 2023; 18 (6):e0287600. DOI: 10.1371/journal.pone.0287600 - 111.

Mathauer I, Nicolle E. A global overview of health insurance administrative costs: What are the reasons for variations found? Health Policy. 2011; 102 (2-3):235-246. DOI: 10.1016/j.healthpol.2011.07.009 - 112.

Dror DM, Preker AS. Social Reinsurance: A New Approach to Sustainable Community Health Financing. Washington DC and Geneva: World Bank and International Labour Office; 2002. A Review of the Book Appeared in Dror DM, Preker AS. World Development. 2002; 30 (2):209-225 - 113.

Schmidt H, Gostin LO, Emanuel EJ. Public health, universal health coverage, and sustainable development goals: Can they coexist? The Lancet. 2015; 386 (9996):928-930 - 114.

Cummins JD, Weiss MA. Convergence of insurance and financial markets: Hybrid and securitized risk-transfer solutions. Journal of Risk and Insurance. 2009; 76 (3):493-545 - 115.

Harrington SE, Niehaus G. Capital, corporate income taxes, and catastrophe insurance. Journal of Financial Intermediation. 2003; 12 (4):365-389 - 116.

Swiss Re. The Essentials of Insurance: Introduction to Reinsurance. Zurich: Swiss Re Institute; 2017 - 117.

Wiedmaier-Pfister M, Dror I. The role of insurers and reinsurers in the growth of microinsurance. In: Churchill C, editor. Protecting the Poor: A Microinsurance Compendium. Geneva: International Labour Organization; 2006 - 118.

Dror DM, Majumdar A, Jangle N. Estimating capital requirements to scale health microinsurance serving rural poor populations. Geneva Papers on Risk and Insurance: Issues and Practice. 2019; 44 :410-444. DOI: 10.1057/s41288-019-00126-w.+

Notes

- Cherry-picking in insurance refers to the practice where insurance companies selectively provide coverage only to low-risk individuals or groups, while avoiding or excluding those perceived as high risk. This practice, also known as “cream-skimming,” allows insurers to minimize their potential liabilities and maximize their profits. However, it can leave higher-risk individuals without affordable insurance options, most notably those who have become high-risk after many years of having been insured when they were considered low-risk.

- This recent investigation assessed the affordability of healthcare for individuals perceived as poor (those receiving unemployment benefits) within the context of California. Utilizing data from adult participants in on- and off-Marketplace individual plans in California in 2021, the study discovered that 41 percent of respondents declared incomes at or below 400 percent of the federal poverty level. Additionally, 39 percent lived in households receiving unemployment compensation. Strikingly, 72 percent of participants reported having no trouble affording premiums, and 76 percent stated that out-of-pocket expenses did not deter them from seeking medical care. These findings imply that ARPA (American Rescue Plan Act of 2021) extended access to insurance plans considered affordable, even though affordability concerns persisted.