Abstract

Japan is a forest-rich country, with forests covering approximately 70% of its land. It is a well-known fact that forests have a wide range of public functions, including prevention of global warming, conservation of national land, and cultivation of water sources. However, owing to low prices for domestic timber due to cheap imports, a decline in forestry workers, a lack of funds, and an aging population, poorly maintained and degraded forests have become a nationwide problem. Since the 1990s, several local governments have established funds for water resources for forest replenishment as a gesture of gratitude to upstream regions that provide a safe water supply. Furthermore, in 2003, 37 of Japan’s 47 prefectures imposed a forest environment tax on prefectural residents, starting with Kochi Prefecture. In 2019, the law of forest environment tax and forest environment transfer tax was enacted, and due to be levied as a national tax in 2024. A unique initiative in the world is a Japanese fund for forest replenishment that began out of gratitude to the upstream regions that provide water. This paper examines the funds and taxes for forest cultivation in Japan, focusing on how they were introduced, accumulated, and collected.

Keywords

- forest environment tax

- forest environment transfer tax

- water source fund

- forest conservation

- forest management

1. Introduction

The United Nations Strategic Plan for Forests (UNSPF) 2017–2031, which aims to promote the forestry sector’s contribution to international goals like the 2030 Agenda, including the sustainable development goals (SDGs), was implemented by the United Nations General Assembly in Ref. [1]. The UNSPF identifies the global forest goals to be attained by 2030 and further targets the details of the goals, which list the specific SDG targets that every global forest goal contributes to.

According to the Global Forest Resources Assessment mentioned in Ref. [2], the global forest area accounts for approximately 4.06 billion hectares (31%) of land area, representing 0.52 hectares per person. The overall rate of net forest loss has significantly decreased between 1990 and 2020 due to the decline in deforestation in several countries and additional afforestation and natural forest growth in other countries. Since then, however, approximately 178 million hectares of forest, approximately five times Japan’s area, has been lost due to deforestation.

Japan’s forest coverage rate is approximately 70%, which ranks third among the 37 OECD (Organisation for Economic Co-operation and Development) countries after Finland and Sweden, and seventh in the world in planted forest area as given in Ref. [3].

Over the past 50 years, Japan’s forested areas have remained unaltered, despite the decline in global forest acreage; thus, encouraging Japan to make the most of its forests could significantly affect the SDGs. Furthermore, planted and natural forests have been increasing annually. Of these, 40% of the total planted forests are fully utilized and older than 50 years, which is the primary cutting period; currently, they are in full-scale utilization. However, the sustainability of using forests is accompanied by the equivalent replacement and growth representing an appropriate maintenance and renewal of trees. Therefore, Japan must prepare sufficient financial resources to contribute to the SDGs. The global warming tax, also known as the “global warming countermeasures tax,” was introduced in Japan in 2012; however, it did not incorporate measures to mitigate forest warming. In light of this, imposing a national forest environment tax to raise funds for this endeavor makes sense. Japanese people should pay this tax, whether in the country or abroad.

The structure of this paper is as follows: Section 2 provides the background to introducing funds and taxes for forest cultivation. Section 3 comprehensively describes water source funds from around the country. Section 4 provides an overview of the forest environment tax before developing the national tax. Section 5 presents the forest environment tax as a national tax, which is the focus of this paper. For more information on Section 5, please refer to Ref. [4].

2. Background to establishing the forest environment tax and the water source fund

Forests can enhance people’s lives and support national economic growth in many ways. These are considered to be the diverse roles that forests play. The Science Council of Japan contends that forests impact 35 elements in eight categories as given in Ref. [5]. The report aims to quantify the functions; however, the annual monetary estimate of these effects is estimated at 70 trillion yen per annum. Considering that Japan’s general account budget for fiscal year 2023 is 114.4 trillion yen, the importance of forest resources is evident.

Following World War II, the Japanese government essentially planned the forestry sector. Massive amounts of hardwoods were felled for munition and rebuilding during and after the war. Additionally, the government implemented an expansion policy of afforestation in cedar and cypress for construction timber. However, the economic liberalization of 1964 enabled timber imports before the trees were old enough for the primary cutting season.

After this long period of stagnation, Japan’s forestry industry is finally showing a slightly upward trend. However, the value of forestry output is only one-third of its peak in 1980, the value of standing timber for cypress, cedar, and pine is only approximately one-fourth, and the number of people engaged in forestry and households owning one hectare or more of forest are declining. Due to the long-term slump in the forestry industry, many forests are poorly maintained and fail to meet the functions of the public interest, for example, water source recharge for national land conservation and preventing global warming.

Securing forest absorption capacity is a global trend, and securing financial resources for this purpose was inevitable. Although it is not well known, the government was considering a same-style tax on the water resource fund. Accordingly, the Forestry Agency introduced the “water source tax” in the 1980s. Initially, the rate was 1 yen per 1 m3 of water used, similar to Toyota City, Aichi Prefecture, which will be described later. Moreover, the Ministry of Land, Infrastructure, Transport and Tourism (formerly known as the Ministry of Construction) introduced a “running water fee.” In 1986, these taxes and fees were unified, to enact a bill that would impose a tax of 2.5 yen per 1 m3 of water used for forest and river maintenance. However, this plan was rejected by the business sector, the Ministry of Finance, Economy, Trade and Industry, and the Ministry of Health, Labour and Welfare. Although the need for forest management was acknowledged, justifying the increased tax burden was difficult because it was unclear who benefited from the public interest function of forests.

Japanese forest ownership was small scale and scattered. Owners’ interest in forests decreased due to the long-term stagnation of forestry and changes in ownership over several generations. Hence, forests suffered from mismanagement. For instance, it was common that new trees were not planted after logging. Only 83% of municipalities had many private forests under their control. Other problems included the lack of a land registry, ambiguous property rights, and undefined borders. To achieve the industrialized growth and appropriate management of forests, the “forest management law” was enacted in May 2018, and the corresponding “forest management policy” was established. The forest management system, formally launched in April 2018, aimed to ensure the consolidation and utilization of forests to enhance the growth of the forestry industry and preserve public interest functions through regular maintenance.

Under these circumstances, social interest in the environment has increased, and water source funds have been established in municipalities nationwide. Moreover, the forest replenishment fund was initiated not based on the polluter-pays or the beneficiary-pays principle, but as a gesture of gratitude to the upstream regions that provide water for downstream users. These funds, which have spread throughout Japan, reflect the national character of the Japanese people and are probably unique in the world. Furthermore, the prefecture with the highest forest rate introduced a forest environment tax at the prefectural tax level, and many of Japan’s other 47 prefectures followed suit. After 15 years, it was finally decided that a national forest and environmental tax would be established, which would begin to be levied and collected in fiscal 2024, 6 years later.

3. Water source funds

Numerous municipal government organizations have created water source funds since the 1990s. Growing public interest in the environment, particularly the need for a steady supply of pure drinking water, has made this legislation easier. This section will first introduce the tap water source conservation fund of Toyota City, Aichi Prefecture, the first attempt at such a fund in Japan.

3.1 Toyota city tap water source conservation fund

Toyota City, located in the northern part of Aichi Prefecture, is known worldwide as the home of Toyota Motor Corporation. With a total length of 117 km, the Yahagigawa River is the major river that flows through Toyota City’s center and has helped revitalize the area. Since ancient times, this mother river has supported life, has been used in transportation and logistics, and has provided agricultural water to people and industry. Its source is high in the mountains of Nagano Prefecture and flows through Nagano Gifu and Aichi Prefectures. Toyota City is situated in the center of the Yahagigawa River.

Upstream of the Yahagigawa River, forests cover 87% of the area, approximately 60% of which is planted forest. The Yahagigawa River provides Toyota City with over 70% of its raw water needs. In addition, the upstream Yahagigawa Dam supplies water for power generation, agriculture, industry, and pure drinking water.

Nevertheless, the aging population, migration of residents, and drop in timber prices due to imports have all contributed to a major decline in the forestry sector. In the Yahagigawa River basin, afforestation was actively pursued following the war; however, over 50% of the planted forests in the water source basin were neglected, even during periods of thinning. Consequently, rough forests became noticeable throughout the region, despite efforts by forestry officials and local residents to preserve the public interest functions of forests. It is considered desirable that the people who live there, as well as local governments and businesses that benefit from these functions, contribute to these efforts.

Since the early days, the Japanese have worked to protect the water quality and purify the Yahagigawa River basin, believing that “a community with the same basin has the same destiny.” The Yahagigawa River water source fund, including 20 towns and villages in the Yahagigawa River basin and Aichi prefecture, was established in 1978. These preconditions enabled the Toyota City tap water source conservation fund to be the first of its kind in the country.

In addition to the city’s water charges for upstream forest conservation projects, Toyota City established a tap water source conservation fund in 1993, at a rate of yen per 1 m2 of used water. The charges of the fund began in 1994. To carry out the project, the city grouped five towns and one village in the upstream area in 2000. Residents perceived the Toyota City Fund as a token of appreciation to the upstream region for providing clean potable water. This project aimed to enhance the water source’s replenishment function, which required thinning the planted forests as a main priority.

However, in 2005, the five upstream towns and villages that the fund covered were all merged into Toyota City, and the residents of those towns and villages were also forced to pay for the fund themselves, losing the original meaning of the fund.

This fund was established as an expression of gratitude, not as an obligation to those who live in the downstream areas of the rivers that provide them with pure, potable water, nor as a burden on the beneficiaries. Adopting approach by several local governments has attracted the attention of people nationwide.

3.2 Establishment of multiple water source funds

In 2001, the Ministry of Health, Labour and Welfare and the Forestry Agency surveyed the status of tap water source conservation efforts. The Ministry then conducted a questionnaire survey in 2007 to follow up on water services, investigating distinct initiatives and water utilities involved in conserving potable water sources. Establishing funds, participating in water source forests, forming and organizing watershed councils, aiding upstream wastewater treatment facilities, and establishing ordinances on water source protection were also covered.

There are approximately 35 funds across the country. They are particularly abundant in the Chubu region of Toyota City. The “Gamagori City Tap Water Source Fund” (Aichi Prefecture), “Tap Water Source Environmental Conservation Tax” by the Aichi Chubu Water Supply Corporation1, the “Misakubo Town Water Source Forest Development Fund” (Shizuoka Prefecture), and “Tap Water Source Environmental Conservation Fund/Kiso Forest Conservation Fund” by the Kiso Wide Area Union2 have the same purpose and method of accumulation as the Toyota City’s fund.

4. Forest environment tax

The country of Japan consists of 47 prefectures. The 47 prefectures are made up of several municipalities called cities, towns, and villages. These municipalities are only differentiated by population and have almost the same functions. If the national government is at the first level, the 47 prefectures are at the second level and the municipalities are at the third level. Thus, Japan has a three-tier administrative system, where each municipality, prefecture, and country can levy taxes independently.

In this section, forest environment taxes levied by the national government are defined as national taxes, those levied by prefectures as prefectural taxes, and those levied by municipalities as city taxes. Note that the fund introduced by many municipalities, such as Toyota City, described in the previous section, is not a tax. However, the purpose of the fund is forest recharge, which is the same as a forest environment tax.

4.1 Prefectural tax

The 1990s saw a growth in the decentralization movement, resulting in financial and administrative reforms, most notably the 1999 “law concerning the development of related laws to promote decentralization.” In 2003, Kochi Prefecture became the first region in Japan to impose a tax on forest environments. The decentralization law has allowed local governments to impose taxes independently and significantly streamline the traditional non-statutory ordinary tax. Moreover, low timber prices, a decline in forestry workers, an aging population, and a lack of funding have contributed to the issue of inadequate maintenance of forests that local government bodies manage. The public benefits only from robust forests. Thus, local governments began enacting a forest environment tax using the decentralization law to aid forest restoration.

Kochi Prefecture’s forest coverage rate is 74%, ranking first among prefectures in Japan. In addition, Kochi’s planted forest per capita is the highest in Japan, approximately six times the nation’s average. Thus, 40% of Kochi Prefecture’s land was negatively affected, raising concerns about the potential loss of forests’ public utility function. In addition, with the lowest financial strength index in the nation, Kochi Prefecture’s fiscal situation was tight; therefore, new funding sources were required to prevent the destruction of forests.

Against this backdrop, Kochi Prefecture became the first in the nation to adopt a forest environment tax in 2003. In 2004, Okayama Prefecture imposed the Okayama Forest Building Prefectural Tax, followed by Tottori’s Forestry Environmental Protection Tax, Shimane Prefecture’s Tax for Creating Forests with Water and Greenery, Yamaguchi Prefecture’s Yamaguchi Forest Creation Prefectural Tax, Ehime Prefecture’s forest environment tax, Kumamoto Prefecture’s Tax for Creating Forests with Water and Greenery, and Kagoshima Prefecture’s forest environment tax in 2005. Figure 1 shows that of Japan’s 47 prefectures, 37 have adopted a forest environment tax under different names.

Figure 1.

Prefectures that have introduced substantial forest environment tax (shaded area). Created by the authors based on Ref. [

A forest environment tax can be defined as a system where local governments enforce an additional tax burden to conserve or recharge forests. However, no tax falls under the forest environment tax category. The introduced forest environment tax used the per capita approach that provides the necessary funds to safeguard forests through a taxation surcharge on inhabitants (prefectural or municipal taxes) mandated by the local tax law. Accordingly, the residence tax is a regular tax collected without a stated goal. Forest conservation initiatives are financed with funds equal to the tax surcharge collected as a forest environment tax.

Most prefectures impose an excess tax of forest environment tax at a fixed rate per capita on corporations, where the amount is determined according to specific criteria such as capital, and a flat excess tax rate on individuals’ per capita residential tax rate. Kochi Prefecture, in contrast, levied a flat tax surcharge on the per capita rates of individuals and corporations. The annual burden per individual in most prefectures is 500–1,000 yen. The Kochi Prefecture charges the minimum rate.

Prefecture-introduced forest environment taxes have specific characteristics: Since 2003, every local government has rapidly moved toward making such taxes law. Second, the method of tax collection necessitates a fair and moderate tax burden for all prefecture residents. Notwithstanding some variances, the tax is only as high as what residents can bear. Third, most local governments work toward reforestation using thinning where appropriate for the surrounding environment and local areas. However, there are variations in the other projects that have been chosen.

The forest environment tax differs slightly from other environmental taxes because it is local. It is not an incentive scheme in which a polluter assumes the environmental burden by paying the costs of the amount of damage inflicted. Nor does the beneficiary burden principle apply, in which the policy’s beneficiaries must pay the bill. In what is known as the joint burden or the participation principle, the current forest environment tax requires residents to share the cost of a certain amount of tax surcharge.

4.2 City tax

Yokohama City, located in Kanagawa Prefecture, has a unique city tax: the “Yokohama Green Tax,” which, introduced in 2009, promotes the “Yokohama Green-Up Plan” to green the city and ensure its sustainability continues to the next generation. Individuals will be charged 900 yen per year, and corporations will be charged an additional amount equivalent to 9% of the annual per capita corporate municipal tax.

Considering the forest environment tax, not the forest and forestry fields, many discussions exist in environmental economics, law, finance, and other areas. Despite this, the results from the resident questionnaire survey indicate that the prefecture’s forest environment tax is generally considered positive.

4.3 National tax

The government has been working and collaborating with pertinent stakeholders for several years to secure funding to preserve and enhance public interest activities. In this context, the Kyoto Protocol was approved at the third session of the 1997 Conference of the Parties (COP3) and was enacted in 2005. At the 17th session of the Conference of the Parties (COP17) held in 2011, a path toward a future framework was also agreed upon. This implies that to meet its greenhouse gas emission reduction target, Japan must protect its forests and acquire funding for initiatives such as thinning. The Ministry of Agriculture, Forestry and Fisheries has requested a tax to fund forest sink initiatives since 2004.

Nevertheless, every region also appealed to the national government to provide funding. Since 2006, local council members have advocated for a forest environment tax through the National Federation of Parliamentarians for the Promotion of Forest Environment Tax Creation and the National Federation for Promotion of Forest Environment Tax Creation, founded by municipalities with extensive forests. The Kochi Prefecture led 34 organizations in implementing the forest environment tax by 2014. This local tax aimed to raise funds for an additional inhabitant tax for forests. Furthermore, a new international framework to address global warming was adopted in 2015 with the Paris Agreement. Then, with public support for forest preservation growing, the 2018 Tax Reform Charter finalized the implementation of the forest environment tax. The Tax Reform Charter stated that the Ministry of Agriculture, Forestry and Fisheries considered building a forest management system and that the forest environment tax will be imposed in the fiscal year 2024, while the forest environment transfer tax began in fiscal year 2019. Additionally, it requested that funding be allocated to cover forest thinning, securing leaders, human resource development, and maintenance of forests, encouraging the use and distribution of wood, public education for municipalities and prefectures, and promotion costs, with prefectures supporting municipalities that maintain their forests. The Cabinet approved the general guidelines for tax reform in 2018, and in 2019, the forest environment and forest environment transfer taxes were passed. It was partially implemented in April of that year.

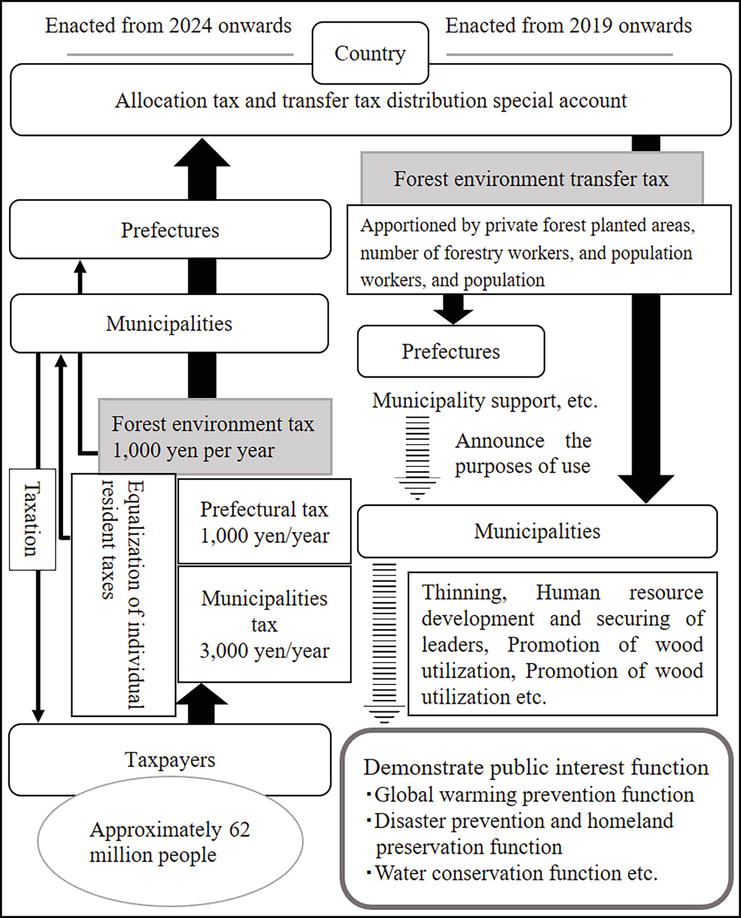

Commencing in 2024, municipalities will impose a national tax of 1,000 yen per year for the forest environment, which will be based on the individual inhabitant tax per capita rate. Additionally, the forest environment transfer tax, financed by the allocation tax and borrowings in the forest management system, was introduced in response to the pressing need for forest maintenance. Transfers began in September and March of the fiscal year 2019. Municipalities and prefectures are assumed to receive a proportionate share of these funds, with 20% going to forestry workers, 30% to the population, and 50% to privately owned forests. However, municipalities must declare the purpose of the forest environment transfer tax to ensure the tax is applied appropriately (refer to Refs. [7, 8]). Figure 2 shows an overview of the forest environment tax and forest environment transfer tax described in this section.

Figure 2.

Mechanism of forest environment tax and forest environment transfer tax. Created by the authors based on Ref. [

Stakeholders oppose treating the forest environment tax as a national tax. One reason is the overlap between the prefectural and forest environment taxes. In the future, it will be necessary to clearly differentiate the use of national and prefectural taxes.

The rationale of the tax is the next thing to think about. Numerous studies contest the tax’s foundation. Even though the forest is also used for greenhouse gas absorption, it makes sense that the beneficiary will pay a fee if the objective is to secure the forest’s water source to guarantee a drinkable water supply. Many people are calling for businesses that emit emissions to be subject to “polluter pays” taxes. Furthermore, it has been pointed out that the policy effects aimed at tax increases are highly unclear.

There is a massive criticism of excessive taxation. A frequent concern is that there will be double taxation in 37 prefectures. Yokohama City and Kanagawa Prefecture are the sources of the Yokohama green tax and the water source environment tax; therefore, residents of Yokohama are subjected to triple taxation. A similar phenomenon occurs in areas where prefectural forest environment taxes and funds have been introduced, like Toyota City. The forest environment tax employs a taxation surcharge method for the inhabitant tax, which reduces resistance and is more straightforward for locals to understand than other taxes. However, it is questionable if a tax this simple to administer is fair and equitable.

Finally, we discuss the transfer standard for the forest environment transfer tax. In fiscal year 2019, the first year, approximately 20 billion yen were allocated to prefectures, approximately 4 billion yen, and to municipalities, approximately 16 billion yen. However, when looking at the amount allocated to Yokohama City, Kanagawa Prefecture ranked first, followed by Hamamatsu City, Shizuoka Prefecture, and Osaka City, Osaka Prefecture. Seven ordinance-designated cities were included in the top 10 local governments. Since the population accounts for 30% of the concession criteria, the amount granted to Kurihara City, which has an area of approximately 10,000 hectares of privately owned artificial forests, is the same as the amounts granted to Osaka City, Setagaya Ward, Tokyo, and Nerima Ward, Tokyo, which have no privately owned forests. The amount was less than the amount granted. This phenomenon has occurred across the country where large amounts of land are given to urban areas, while less is given to areas with large forest areas.

There are 792 cities in Japan (as of October 1, 2022), but designated cities must have the same administrative and financial capabilities as prefectures, so they currently have a population of approximately 70. Twenty cities with a population of over 10,000 people have been designated by government ordinance, and their population accounts for approximately 20% of the total population. Total tax payments are scheduled to increase yearly, exacerbating people’s dissatisfaction in forested and depopulated areas.

According to a government report, approximately 84 billion yen have been allocated to municipalities nationwide in the 3 years since the system began in 2019. However, 47% of that amount, or 39.5 billion yen, is not being utilized. In August 2023, the Forestry Agency announced that the forest environment transfer tax accounted for 40 billion yen in fiscal 2022 (municipal portion: 34.1 billion yen, prefecture portion: 5.8 billion yen), and the utilization rate of the transfer amount is 80%. Nearly 50% of the forest environment transfer tax was used, and 20% remains unused in fiscal year 2022 because the amount is destined for urban areas with large populations under the current allocation standards. Therefore, in the 2024 tax reform, the government is adjusting the distribution standards to allocate more to local governments with large forest areas.

5. Concluding remarks

Forest recharge is essential to contribute to the SDGs and requires sufficient financial resources. In Japan, Toyota City was the first to establish a fund for forest recharge in 1993, and this municipal-level initiative has expanded nationwide. In 2003, Kochi Prefecture introduced a forest environment tax at the prefectural level. Currently, 37 of the 47 prefectures have also introduced it. From 2024 onwards, a forest environment tax will also be levied as a national tax. The system of collecting funds for recharging forests at each administrative level is unique to Japan as a forest-rich country.

From fiscal 2024, a “forest environment tax” will be collected as a national tax of 1,000 yen per person from those living in Japan, in addition to the resident tax. If there are approximately 62 million taxpayers, tax revenue is expected to reach 62 billion yen per year. The tax revenue will be distributed to all prefectures, towns, and villages nationwide as a “forest environment transfer tax.” Although problematic factors have been identified in the forest environment tax, there is no doubt that it will contribute to maintaining the forests’ public functions as a financial resource for forest recharge, along with the forest environment tax as a prefectural tax and water resource recharge throughout the country. In the future, I hope that Japan’s unique forest environment tax will become a model for forest cultivation worldwide, as it continues to make improvements, including reviewing the concession criteria and resolving issues.

References

- 1.

United Nations. United Nations Strategic Plan for Forests, 2017-2023 [Internet]. 2017. Available from: https://www/un.org/esa/forests/wp-content/uploads/2016/UNSPF_AdvUnedited.pdf [Accessed: December 25, 2023] - 2.

FAO (Food and Agriculture Organization of the United Nations). Global Forest Resources Assessment 2020 Key findings. [Internet]. 2020. Available from: http://www.fao.org/3/ca8753en/CA8753EN.pdf [Accessed: December 25, 2023] - 3.

FAO. Global Forest Resources Assessment 2020: Main Report. Rome, Italy: FAO; 2020. 184p - 4.

Nakayama K. A Forest Environment Tax Scheme in Japan – Toward Water Source Cultivation. Singapore: Springer Singapore; 2022. 126p. DOI: 10.1007/978-981-16-9352-6 - 5.

The Science Council of Japan. Types of Multifunctional Forest Functions and Examples of Quantitative Assessment (in Japanese) [Internet]. 2001. Available from: https://www.scj.go.jp/ja/info/kohyo/pdf/shimon-18-1-1.pdf [Accessed: December 25, 2023] - 6.

Kohsaka R, Uchiyama Y. Forest environmental taxes at multi-layer national and prefectural levels: Comparisons of 37 prefectures survey results in Japan. Journal of the Japanese Forest Society. 2019; 101 :246-252. DOI: 10.4005/jjfs.101.246 - 7.

Forestry Agency. Annual Report on Forest and Forestry in Japan, Fiscal Year 2018 (Summary) [Internet]. 2018. Available from: https://www.maff.go.jp/e/data/publish/attach/pdf/index-170.pdf [Accessed: December 25, 2023] - 8.

Forestry Agency. Annual Report on Forest and Forestry in Japan, Fiscal Year 2022 (Summary) [Internet]. 2022. Available from: https://www.maff.go.jp/e/data/publish/attach/pdf/index-193.pdf [Accessed: December 25, 2023] - 9.

Ministry of Agriculture, Forestry and Fisheries. Forest environment tax and forest environment transfer tax (in Japanese) [Internet]. 2023. Available from: https://www.rinya.maff.go.jp/j/keikaku/kankyouzei/kankyouzei_jouyozei.html [Accessed: December 25, 2023]

Notes

- The Aichi Chubu Water Supply Corporation is a special local government that supplies water to four cities and one town in Aichi Prefecture.

- The Kiso Wide Area Union is made up of six towns and villages in Kiso District, Nagano Prefecture.