Abstract

The chapter looks at the challenges of microfinance governance, namely how to balance the interests of the poor with neoliberal governmentality, poverty rates, and Bangladesh’s unique challenges. The study closes the information gap regarding the impact of microfinance governance systems on poverty alleviation, financial performance, sustainability, and social effects. The literature evaluation covers the Impact of COVID-19 and climatic shocks on rural welfare, MFI financial sustainability, and microfinance empowerment. A qualitative and quantitative analysis of secondary data from MFI annual reports, publications from the Microcredit Regulatory Authority, and relevant literature is done using Porter’s Competitive Strategy Theory. The research found that MFIs need inclusive governance with stakeholder viewpoints to fight poverty and improve social responsibility. It reveals Bangladeshi MFIs have decreased poverty and increased financial inclusion, but more strategic governance improvements are required for optimum benefit. MFIs should reduce borrowing and budget deficits, combine Qardhasan and Zakat, and prioritize income-generating activities before lending. This study shows how governance affects MFI performance and emphasizes the necessity for strategic adjustments to eliminate poverty and social inequity. The research found that Bangladeshi MFIs must balance poverty alleviation and financial viability. Future laws should protect microfinance’s goals from profit maximization.

Keywords

- governance

- microfinance

- inequality

- banking

- rural development

- social responsibility

- poverty alleviation

1. Introduction

Bangladesh’s varied and quickly expanding microfinance industry provides a rare opportunity to contrast different approaches. This research analyses the governance and operational frameworks of three important models, the Microfinance Bank (MFB), Microcredit Program (MCP), and Rural Development Scheme, to comprehend their implications on social effect, poverty reduction, and financial performance (RDS).

This study examines the governance and operational frameworks of MFB, MCP, and RDS in Bangladesh, emphasizing financial performance, social effect, management systems, and poverty reduction. This research investigates the impact of several models’ governance structures on financial performance variations and contributing factors, operational sustainability, outreach, and the impact of social inequality and poverty reduction in Bangladesh.

What is the impact of microfinance program intensity on the lowering of income inequality, and how does this impact differ among countries? What is the interplay between environmental disasters, microfinance, women’s self-sustainability, and the effectiveness of microfinance in promoting self-reliance? These subjects investigate the impact of microfinance on income disparity, the decrease of inequality, and the self-sufficiency of women in the face of natural disasters.

This research investigates the hazy connection between Bangladesh’s microfinance institution (MFI) performance and governance frameworks. Through 655 MFIs, microfinance provides services to 77% of the population; the Microcredit Regulatory Authority (MRA) is the Bangladesh government’s MFIs regulatory institution. However, little is known about how governance systems impact sustainability and performance. This division is emphasized by the unique characteristics of Islamic microfinance and the balancing of social goals with financial sustainability.

Being a global pioneer in microfinance, this study offers insightful information on the effectiveness of the models. Comprehending the impact of these strategies on financial success and poverty reduction might help shape policy, enhance MFI efficacy, and progress microfinance research.

There are several advantages to this research. To illustrate the distinctions and implications of MFB, MCP, and RDS on the impact of social inequality and poverty alleviation, the article first contrasts them. Secondly, it examines how governance structures impact MFI sustainability and performance, exposing useful management strategies. Third, the research evaluates the capital structure, gender diversity in management, and CEO duality of various models regarding their financial feasibility. Finally, based on our study, policy initiatives and wise donor contributions may enhance the reduction of poverty and poor access to financing.

Secondary data from three MFI annual reports, publications from the Microcredit Regulatory Authority, and relevant literature are analyzed qualitatively and quantitatively for this research. This data is subjected to Porter’s Competitive Strategy Theory, which posits that five criteria determine market competitiveness and attractiveness.

The study methodology describes data collection and analysis; the analytical part discusses how governance arrangements influence MFI performance, including the impact of social inequality and financial sustainability; and the conclusion highlights significant results and policy implications. Bangladeshi MFI governance literature is reviewed.

2. Literature review

Microfinance reduces rural Bangladeshi women’s poverty. Akhter and Kun [1] pioneered an econometric analysis of microfinance empowerment while examining the Bangladesh Rural Advancement Committee’s program (BRAC). Parvin et al. [2] evaluated Bangladeshi MFI capital structure, financial performance, and sustainability. According to research on Bangladeshi microfinance and COVID-19, the business has improved [3].

Nawaz et al. [4] also underlined the importance of microfinance in women’s business success. The researchers explored how social capital mediates microfinance and women’s entrepreneurial performance. Research on the impact of climatic shocks on rural Bangladeshi households has shown that climate affects family well-being, particularly in rural areas [5]. Microfinance enterprises’ financial sustainability-environmental performance trade-off has been studied. 2022 research on this trade-off in South and Southeast Asia and microfinance companies’ financial and environmental dynamics supports this claim [6]. These studies demonstrate how the COVID-19 pandemic and natural catastrophes affect Bangladeshi microfinance, family welfare, financial performance, and sustainability.

2.1 Prominent microfinance models

Bangladesh has reduced poverty and financial isolation using microfinance. The SHG and MFB Grameen Model have given the poor additional financial services. These versions are well-known both in Bangladesh and elsewhere. Selling Islamic commodities, the Islamic Bank Bangladesh Limited (IBBL) Rural Development Scheme (RDS) is another Grameen Model-based, Shariah-compliant microfinance initiative.

Group financing enables Grameen Model borrowers to get modest loans for income-generating businesses without providing collateral [7]. This perspective empowers women financially [8]. Bangladeshi microcredit research shows SHGs empower women. These types are popular worldwide, including in Bangladesh. The Islamic Bank Bangladesh Limited (IBBL) Rural Development Scheme (RDS) sells Islamic items and is another Grameen Model-based microfinance venture [9]. The impact of microfinance on rural families shows its worth [10].

Bangladesh benefited from IBBL RDS microfinance. Indian microfinance companies like IBBL encourage sustainable development [11]. An analysis of the Rural Development Scheme’s Islamic performance shows its compliance and efficacy [12]. Bangladeshi microfinance enterprises reduce poverty and increase financial inclusion. These projects have helped low-income Bangladeshi women achieve rural welfare and sustainable development.

2.2 Microfinance banking (MFB) model

MFB fights poverty and promotes financial inclusion by lending to people experiencing poverty. By collecting 99% of debts with 87% female involvement via severe punishment and mutual support, the MFB enables Bangladeshi women to gain agency [13]. The absence of a legal agreement between MFB and its borrowers burdens poverty reduction, trust-based financial inclusion, and social capital [14].

Muhammad Yunus established MFB and advocated for philanthropic financial services and impact assessments for organizations dedicated to poverty reduction and development. With a 93.15% repayment record, the MFB’s 2568 outlets and 9 million borrowers illustrate its commitment to reducing poverty and promoting financial inclusion [15]. Aiding the poor to escape poverty with Microcredit is consistent with the microcredit summit campaign’s focus on poverty reduction [16].

With the 2006 Nobel Peace Prize awarded to Professor Yunus, microfinance, and MFBs in particular, became acknowledged internationally for combating multidimensional poverty. Inspiring business among the disadvantaged and decreasing poverty via a distinctive methodology has put creditworthiness and financial inclusion regulations to the test [17]. Microfinance reduces Global poverty, according to the UN Millennium Project [18].

An exhaustive examination of the MFB model and its effects on financial inclusion and the elimination of poverty demonstrates the intricacy and significance of microfinance in empowering people experiencing poverty. Through global development goals, MFB transforms financial inclusion and poverty reduction by capitalizing on the under privilege’s social capital, trust, and entrepreneurial potential.

2.3 Micro credit programme model

Economic empowerment and poverty reduction influence Bangladesh’s microfinance ecosystem. The 1974-founded Micro Credit Programme (MCP) is a substantial loan coverage and customer participation MFI. Like other Bangladeshi MFIs, the MCP has decreased illiteracy, bad health, and squalor. Large rural populations and agrarian economies cause underemployment.

MFIs’ “credit plus” initiatives provide borrowers high-quality inputs, assistance, and training to fight poverty. $100–$1000 “Microloans” (Dabi) have enabled rural poultry, fishing, and handicraft companies to grow, supporting grassroots economic growth [10]. The “Progoti loan” reduces poverty by lending small business loans to men and women who cannot access commercial bank loans. Healthcare, skill development, and asset transfers empower the poor and chronically destitute while advancing society [19].

The Rural Development Scheme (RDS) of Islamic Bank Bangladesh Limited (IBBL) provides Shariah-compliant services to people experiencing poverty, developing Islamic microfinance models. RDS mirrors the MFB model while giving Islamic microfinance solutions tailored to the target population’s financial requirements [20, 21]. Research like the Amanah Ikhtiar Malaysia Microcredit Scheme shows that microfinance reduces poverty by improving disadvantaged people’s income [22, 23].

Bangladesh has shifted to digital Microcredit to reduce poverty and boost economic growth. Islamic microfinance has grown due to fintech, meeting low-income people’s social and financial demands [24]. Studies on how interest rate limits affect microfinance organizations’ sustainability have also shown the challenges of controlling interest rates to ensure their financial viability [25, 26]. Bangladesh’s microfinance business includes traditional, online, and Islamic firms. MFIs and NGOs’ poverty reduction, empowerment, and financial aid have affected Bangladesh’s socio-economic structure.

2.4 Rural Development Scheme (RDS)

Bangladesh’s main microfinance program, the Rural Development Scheme (RDS), promotes rural and agricultural investment to reduce poverty and promote economic independence. RDS financial services have helped and employed rural people since 1995, largely in agriculture and non-agriculture [27]. Rural employment, justice, and equality demonstrate the program’s poverty reduction and economic empowerment goals [28, 29].

RDS microfinance has increased rural financial inclusion. Banking services with flexible lending lengths and low rates provide rural populations with greater financial independence [30]. Through microinsurance and savings initiatives, the RDS has protected its members from accidents and natural calamities [31].

Most RDS financing is Islamic (bai-muajjal). Bai-salam, Mutharabah, and Ijarah provide Sharia-compliant financing [32]. The RDS’s group-based financing and repayment structure has helped rural enterprises get microenterprise and agricultural loans, boosting local economies [12, 33].

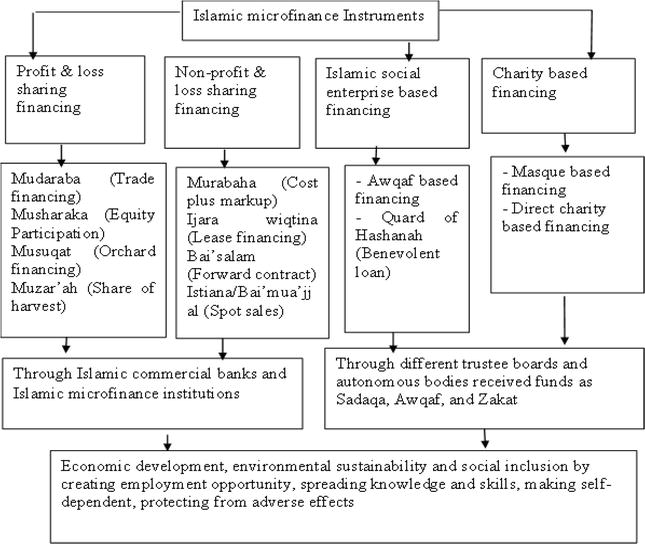

RDS members support holistic and ethical financial development via social and religious education, spirituality, and collective morality [34]. The program’s emphasis on social and religious beliefs, honesty, autonomy, and knowledge has benefitted women financially [35]. According to research, Islamic microfinance via rural development and poverty reduction (RDS) empowers, earns, and builds social capital for women [36]. Rural communities benefit financially from the program’s microfinance and socio-economic benefits [37]. Bangladesh’s unique Islamic microfinance Rural Development Scheme (RDS) promotes rural development, poverty reduction, and financial inclusion—Bangladesh’s microfinance ecosystem benefits from ethical and Islamic banking (Figure 1).

Figure 1.

Islamic micro-finance conceptual model to achieve sustainable development goals (SDGs). Source: Uddin et al. [

Numerous studies have compared microfinance governance with poverty and social injustice reduction. More study is required to understand the complicated linkages between social inequality, microfinance governance, and poverty alleviation.

The MFI’s performance depends on its qualities, financial sources, organizational structure, and external environment. However, little is known about how these attributes affect MFIs’ social and financial success under different governance and regulatory systems. Further research is required to understand governance processes that substantially impact MFI performance, social inequality, and poverty alleviation.

A few thorough quantitative studies on government-run microfinance program governance have combined provider and recipient views using primary data. This demonstrates a research vacuum concerning women’s self-sufficiency, microfinance, and environmental disasters. More empirical research is needed to close gaps in the literature and ascertain if microfinance encourages self-reliance among environmentally sensitive women.

Economic inequality and poverty are decreased via microfinance, although the exact mechanism by which this happens is yet unknown. By examining the relationship between board structure and performance, the report draws attention to the need for further research on the governance mechanisms that underpin MFIs’ social and financial success and their impacts on reducing poverty and inequality.

3. Research methods

Corporate governance and social effect depend on performance and structure. This research uses Porter’s competitive strategy theory [39] to examine this intricate relationship. The approach promotes employee performance-based pay and incentive programs to increase company performance. When comprehensive, cost-free contracts for succeeding periods are unachievable, alternative corporate governance and social effect evaluation methodologies are crucial [40].

This research follows Bhimani [41], emphasizing extensive conceptualization, trustworthy data collection, and rigorous analysis. The causal research study reveals how effective governance may reduce industry and poverty’s social effects. This technique is beneficial for evaluating microfinance firms since governance structures influence the performance and social effects of microfinance institutions (MFIs).

The Grameen Bank, MCP, and RDS microfinance divisions supplied secondary data for this research. Information accessibility and availability impact secondary data utilization, suggest Maione and Barbosa [42]. Although beneficial, this method has data comprehensiveness and institution homogeneity issues.

The research analyses data using descriptive and inferential statistics. This sophisticated approach explains MFI governance processes such as information disclosure, board makeup, auditing requirements, and CEO and director remuneration. Most non-profit institutions include commercial banks, cooperatives, credit unions, nonbank financial institutions, and rural banks. Their social effect is studied beyond financial evaluations. This variation in organizational forms highlights the difficulty of responsible donors and recipients in microfinance governance [40].

Bangladeshi MFI governance affects profitability, customer service, and attractiveness. A preliminary study suggests strict transparency and auditing norms may boost financial performance, whereas remuneration may hurt it. Studies suggest that gender diversity in management, corporate governance, and social responsibility are desirable.

This study contributes to the academic discussion around corporate governance and performance in microfinance and offers useful guidance to practitioners and policymakers. Within the ever-changing realm of microfinance, the intricate but significant relationship between financial performance, the impact of social inequality, and governance frameworks is made clear by both theoretical perspectives and actual data.

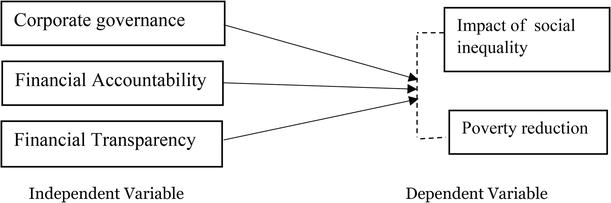

3.1 Conceptual framework

See Figure 2.

Figure 2.

Conceptual framework. Source: Author’s self compilation.

4. Data analysis and interpretation

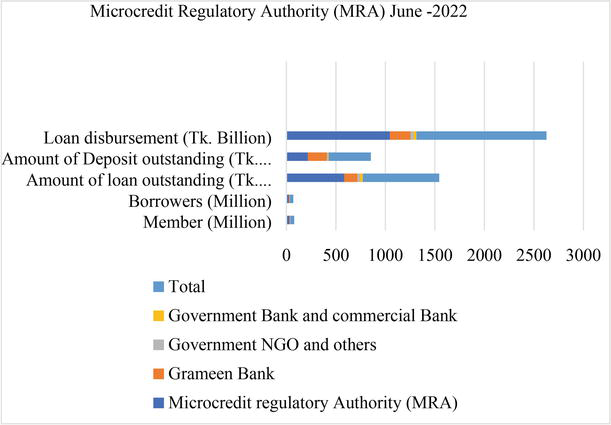

Bangladeshi microcredit sector analysis utilizing June 2022 Microcredit Regulatory Authority (MRA) data. Membership, borrowers, loan disbursement, and outstanding amounts are examined to assess the sector’s status and trends. MRA data provides a complete picture of Bangladesh’s microcredit sector. As of June 2022, the sector has 39.48 million members and 34.76 million active borrowers. This high penetration shows Microcredit’s relevance in Bangladesh’s financial ecosystem. The astonishing Tk. 771.80 billion loans outstanding shows the massive financial activity microcredit institutions facilitate. Also notable is the Tk—426.68 billion in outstanding deposits. Loan disbursement was also strong, total Tk. 1313.67 billion.

Detailed analysis of the data gives intriguing insights into microcredit provider distribution. This industry is dominated by the Grameen Bank, a pioneer with 7.14 million members and borrowers. Grameen Bank has 134.58 billion in loans and 191.02 billion in deposits. Government NGOs and other organizations service a smaller but considerable market share. They have 1.52 million members and 1.12 million debtors with Tk—24.20 billion in loans. With 0.92 million members and 0.52 million debtors, government and commercial banks are smaller (Figure 3).

Figure 3.

Microcredit regulatory authority (MRA) June-2022. Source: Author’s self compilation.

Bangladesh’s microcredit sector is vibrant and diverse, with many firms contributing to its growth. Established microcredit providers like Grameen Bank demonstrate their efficacy. Government NGOs and commercial banks suggest a multifaceted strategy for microfinance in the country. Due to Bangladesh’s socio-economic situation, microcredit services are in high demand, as seen by loan disbursements and outstanding amounts. Microcredit empowers underprivileged communities, especially women, and reduces poverty.

The MRA data shows that microfinance has helped financial inclusion and development in Bangladesh. The sector’s expansion and diversification show its adaptation to Bangladeshi demands. As the sector evolves, it will boost economic growth and social empowerment.

Microfinance in Bangladesh is approached differently through MFB, MFIs, and RDS in IBBL. MFBs and microfinance institutions MFIs differ from RDS in funding sources and training but share loan types and group meeting procedures. IBBL charity foundation funds RDS, unlike MFB and MFIs, which rely on self-funding and NGO contributors. RDS does not offer skill-based training like its competitors.

The research shows that RDS outperforms MFBs and MFIs. Due to better governance, the company’s yearly growth rate has grown from 7% to 12.57%. This shows how effective and appealing RDS is to Islamic borrowers. Success has come from its unique microfinance strategy, which matches its target demographic’s religious views. This alignment may boost payback and operational efficiency via trust and community.

RDS accountability and openness boost borrower trust. The IBBL charitable foundation might offer an innovative fundraising method to stabilize and maintain the financial model. Despite being microfinance pioneers, MFBs and institutions (MFIs) can not reach their full potential due to operational model restrictions.

RDS enhanced growth, repayment rates, and operational efficiency, suggesting that future microfinance programs in Islamic-majority areas should follow suit. The success of microfinance schemes depends on cultural and religious alignment, as shown by RDS’s popularity among Islamic borrowers. Therefore, microfinance organizations should adjust their programs to their target demography’s cultural and religious backgrounds to improve efficacy, growth, and sustainability. The relative success of RDS in Bangladeshi microfinance supports this decision. However, these models must be monitored and adjusted to meet beneficiaries’ changing requirements and the changing economy.

4.1 Microfinance banking model

Figure 4.

Comparative sheet of Grameen Bank. Source: Author’s self compilation.

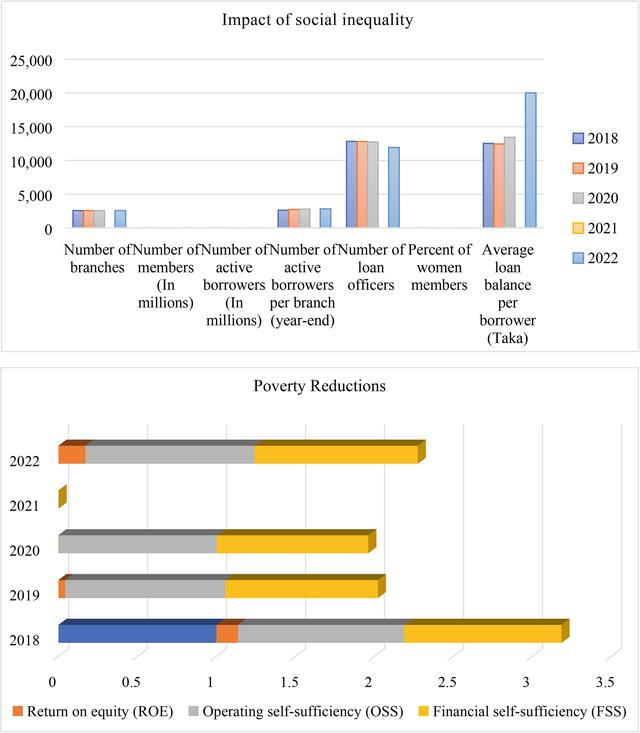

Grameen Bank has grown and stabilized with a stable number of branches and a minor increase in members and borrowers. The average loan balance per borrower rose from BDT 12522 in 2018 to BDT 19977 in 2022, suggesting a growing credit portfolio and financial inclusion. The high ratio of female members and loan officers supports research showing that microfinance institutions empower women by providing financial resources, which can boost home welfare and community development.

ROE, OSS, and FSS show the bank’s financial soundness. 2022 ROE rose to 17.09% from 0.22% in 2020, indicating recovery and profitability. OSS and FSS percentages over 100% indicate that the bank is operationally and financially self-sufficient, supporting sustained microfinance models.

Grameen Bank should continue its existing path based on evidence. Continue to increase its influence, especially among women, and maintain financial health. Diversity has been found to improve microfinance institutions’ stability and reach. Therefore, the bank may consider expanding its financial products. Grameen Bank’s microfinance program balances social benefits and financial viability. Its focus on empowering women and strong financial indicators set it for microfinance success and growth.

However, huge loan defaults, especially in group programs, posed problems. Operational and repayment concerns caused these bank-supervised schemes to fail. Thus, NCBs have restricted or stopped lending to group-based small loan programs. However, they continue lending. State-owned and private commercial banks provide ‘wholesale loans’ to MFIs (MFIs). These loans allow MFIs to lend to microcredit consumers at 10–15% interest rates.

Banking includes state-owned, commercial, and foreign banks with different operations and clientele. Grameen Bank’s success inspired major NCBs and agricultural banks to offer Microcredit, indicating a shift toward inclusive finance. Though promising, group-based microcredit schemes struggled and had high loan default rates. NCBs’ microcredit expansion has suffered a major setback. To address the issues, NCBs have switched from group loans to individual loans, signaling a strategic realignment centered on operational efficiency and risk management. MFIs receive wholesale loans from state-owned and private commercial banks, demonstrating their collaboration in financial inclusion. The risk management strategies of NCBs and other banks in microcredit operations will reveal how financial institutions handle sector difficulties. Longitudinal studies on the long-term durability and efficacy of group-based and individual microcredit services would advance financial inclusion and poverty reduction.

4.2 Rural development scheme (RDS) in Bangladesh

According to the text, Bangladesh’s Rural Development Scheme (RDS) is vital to microfinance, especially Islamic microfinance. Bangladesh accounts for almost half of Islamic Microfinance’s global clients. This approach relies on Islamic banks, tiny Islamic IMFIs, and a conventional MFI with an Islamic microfinance program. These groups promote rural development and financial inclusion.

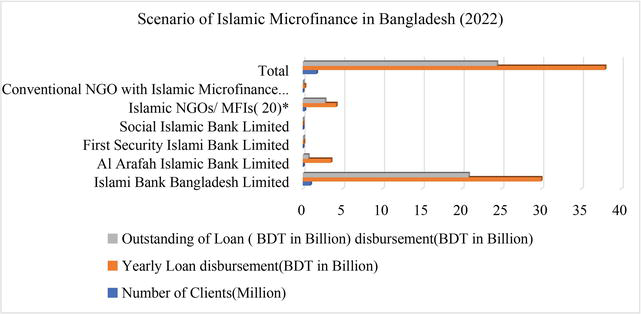

Islami Bank Bangladesh Limited (IBBL) stands out. It dominates Bangladesh’s Islamic microfinance industry with 78.84%. This large number shows IBBL’s sector dominance. Other Islamic banks, including Al Arafah Islamic Bank Limited, First Security Islami Bank Limited, and Islamic NGOs and MFIs, play important roles but less than IBBL. These institutions serve many clients, demonstrating a strong demand for Islamic microfinance.

Figure 5, “Scenario of Islamic Microfinance in Bangladesh (2022),” shows the current situation of Islamic microfinance in Bangladesh. This figure shows the number of clients served, annual loan disbursements, and outstanding loans for IBBL, other Islamic banks, Islamic NGOs/MFIs, and a conventional NGO with an Islamic microfinance program. The numbers show the extent of these services and the financial resources raised for rural development through Islamic microfinance.

Figure 5.

Scenario of Islamic microfinance in Bangladesh (2022). Source: Author’s self compilation.

This data analysis yields several noteworthy insights. First, Islamic microfinance dominates rural development in Bangladesh. These services are crucial to the financial ecosystem since many rural people use them. Second, the data shows IBBL’s sector domination. As the leading supplier, IBBL is crucial to Islamic microfinance. Its strategies may instruct the industry. Third, the range of providers—including smaller Islamic banks and NGOs/MFIs—makes Islamic microfinance competitive. Customers may benefit from the variety of goods and services. These findings affect future research and decision-making in many ways. Understanding Islamic microfinance clients’ needs and preferences is crucial. This data may be used to create financial solutions and enhance services. An extensive analysis of IBBL’s strategy and operations may provide other Islamic microfinance organizations with industry best practices. The long-term effects of Islamic microfinance on rural development and poverty reduction in Bangladesh must also be assessed. This would help evaluate the projects’ financial effect and efficacy. One must investigate the role and impact of smaller firms in the ecosystem to fully appreciate its difficulties, dynamics, and relevance. In conclusion, comparing conventional and Islamic microfinance may help operators and policymakers evaluate their pros and cons.

4.3 The impact of social inequality on rural development scheme

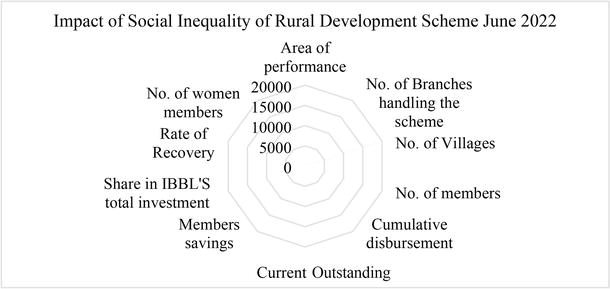

The 1995 Islami Bank Bangladesh Limited Rural Development Scheme (RDS) has grown and produced notable results. About 350 bank branches have executed the campaign, reaching 18,615 communities since June 2022. This huge outreach effort has had an impact on 947,305 people. Additionally, the idea is highly profitable monetarily. A debt of BDT 20,798.82 million remains over the total disbursed funds of BDT 130,445.12 million. Members have exhibited commendable financial participation and maintenance of savings, amounting to BDT 6890 million. The program’s investment share of 3.64% is significant in light of the proportional scale of IBBL’s portfolio. The RDS exhibits an outstanding recovery rate of 99.59%. The fact that 85% of the program’s participants are female further emphasizes the program’s criticality in empowering rural women (Figure 6).

Figure 6.

Impact of social inequality in rural development scheme June 2022. Source: Author’s self compilation.

Data supports several significant findings. Many communities and a large membership base show that the RDS is well-established in rural areas. The scheme’s broad appeal suggests its accessibility and acceptance. Second, the financial data indicate a strong scheme. The system’s large disbursements and deposits show active engagement and trust. The nearly 100% recovery rate is impressive, demonstrating good management and borrower reliability. The scheme’s high female membership shows its inclusion and ability to promote gender equality in rural financial access. Last, the scheme’s investment share shows its importance to IBBL’s strategy.

4.4 Microfinance model

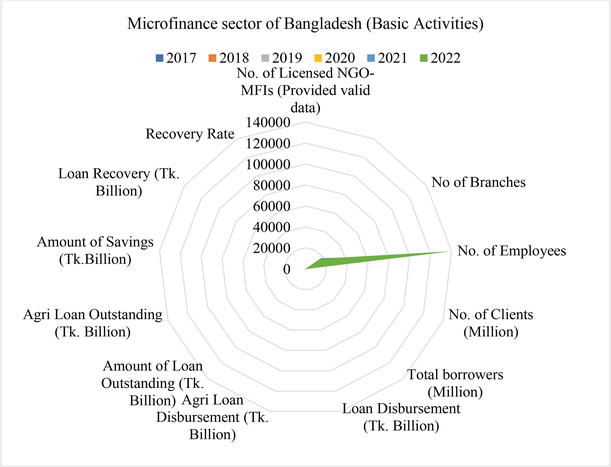

From 2017 to 2022, Bangladesh’s microfinance sector grew and survived. This report examines the sector’s growth based on licensed NGO-MFIs, branches, workers, clients, borrowers, loan disbursement, outstanding loans, savings, and loan recovery rates. The number of licensed NGO-MFIs increased from 590 in 2017 to 758 in 2021, then declined to 655 in 2022. This pattern shows strong sector expansion followed by consolidation or regulatory reforms. The number of branches fluctuated from 17,977 in 2017 to 14,674 in 2018, then rose to 17,120 by 2022. These swings may indicate operational realignments or market movements that required branch operations strategy changes.

The sector’s workforce rose from 108,654 in 2017 to 139,526 in 2022. This increase in employment reflects industry growth and perhaps operational size. This expansion was matched by steady client growth. Over the same period, clients increased from 24.64 million to 29.9 million and borrowers from 19.31 million to 24.85 million. This increase in clients and borrowers shows a wider market and rising microfinance demand. Financial operations, especially loan disbursements, grew. Total loan disbursements rose from 456.02 billion Tk in 2017 to 1045.78 billion Tk in 2022, with agricultural loans rising significantly. Despite the rise in loan disbursements, the recovery rate remained constant at 96–97%. This consistency indicates good sector risk management and collection (Figure 7).

Figure 7.

Microfinance sector of Bangladesh (basic activities). Source: Author’s self compilation.

Based on these findings, Bangladesh’s microfinance sector should make many strategic decisions. First, as clients and loan disbursements grow, MFIs should deliberately expand, especially in underserved areas. Second, with agricultural loans rising, MFIs should continue or expand their focus on this profitable and important segment. Third, the continual increase in personnel highlights the necessity to invest in human resources to sustain growth and service quality. Fourth, digital loan processing, risk management, and customer service technologies are needed to handle scale. Finally, the fall in licensed NGOs in 2022 requires continuous regulatory monitoring and strategy adaptation. Data shows a lively and rising Bangladeshi microfinance sector. Expansion and innovation, especially in digital finance and inclusive banking policies, could boost the sector’s economic development and impact on poverty reduction.

4.5 Empirical studies on MFB, MFI, RDS

Badan Kredit Kecamatan (BKK), Kredit Usaha Rakyat Kecil (KURK), Bank Rakyat Indonesia (BRI), Grameen Bank, BRAC, TRDEP, PTCCS, and Regional Rural Banks in India are crucial to financial inclusion and poverty reduction. These institutions provide loans and other financial services to underserved borrowers to enhance income, especially in rural and economically challenged regions. Nahar and Uddin [43] found that landholding size, education, loan size, and family labour affect the success and reach of MFIs and RDSs.

Empirical research on this topic is varied and substantial. Families with fewer landholdings and less formal education are more likely to engage in microfinance programs, which reduce severe poverty more than moderate poverty. Even non-participating families gain from program spillovers. Bangladeshi studies demonstrate that borrower income substantially connects with land holding size, total yearly employment, loan amount, and family labour. Interestingly, family labour, days worked per year, and landholding size increase NGO recipients’ income, whereas illness decreases it. Another important conclusion is that land assets, employment, and family labour impact family income more than NGO membership terms and loan quantity. This raises doubts regarding MFIs’ poverty alleviation and economic development roles.

The research shows varied results on MFIs and RDSs’ poverty reduction. Grameen Bank lends to agricultural and non-agricultural businesses, increasing income and consumption. Different repayment systems provide BRAC members greater freedom than Grameen Bank members. Ahmed’s [44] report also critiques GB’s operating restrictions, such as not lending to the landless or severely poor, and its large profit margin compared to other sectors. RDS programs provide reduced interest rates and incentives for prompt payback. RDS’s microfinance methodology is more sympathetic and sustainable, particularly its treatment of natural catastrophe borrowers. The studies also note that excessive borrowing might put customers in debt, emphasizing MFIs’ need to manage fund deficits.

These results should inform a substantial portion of the strategic decisions made by RDSs and MFIs. Before consumers spend their money, prioritize actions that generate income to maximize the utilization of loans. Prioritizing credit-use education activities, loan availability, and installment payment duration are essential components of this. Second, Bangladesh could better battle poverty by including Qardhasan and Zakat in their frameworks. Thirdly, excessive borrowing and fund shortfalls must be addressed. Educating borrowers on the risks associated with overborrowing and establishing appropriate lending procedures is critical. In order to enhance their impact, these organizations can benefit from discerning the socio-economic attributes of their borrowers and adapting their services accordingly.

Although empirical evidence suggests that MFI and RDS effects are influenced by factors such as family work and landholding size, they have nonetheless contributed to reducing poverty. The success of these financial institutions is contingent upon their capacity to adapt to fluctuating market conditions, prioritize sustainable lending, and tailor services to individual borrowers. They may be able to continue fostering economic growth and reducing poverty.

4.6 The impact of social inequality and poverty reduction of the microfinance program

The empirical study examines poverty alleviation and the impact of social inequality in microfinance institutions (MFIs). In this field, researchers have uncovered a variety of findings. Methodological Inconsistencies May Account for Variations in Research Design and Implementation. Comprehensive statistical analysis and appropriate research methods are important for the evaluation of MFI efficacy, as stated by Cull and Morduch [13]. This variety in results illustrates the significance of geography, period, research design, and other variables when analyzing the effects of MFIs.

Bangladeshi studies demonstrate how microfinance may boost family earnings and assets. Examples include improved profits, fixed assets, net working capital, food and medical expenses, and children’s education. These studies have frequently missed the program’s overall effectiveness. Some studies have shown that MFIs improve physical and economic wellness by enabling access to healthcare and higher education. MFIs also boost members’ dignity and self-confidence, improving loan payback and income sustainability.

MFIs seem crucial to poverty reduction, particularly in countries with scarce NGO loans. Low-interest loans have reduced poverty. An estimated 5% of MFB and MFI-NGO participants reduce poverty yearly. Grameen Bank members are at least 42% poor. MFB, MFIs-NGO, and RD studies show that these activities aid the severely disadvantaged. Uddin et al. [45, 46] study shows that borrowers’ incomes, healthcare, nutrition, empowerment, and education are improving.

The report advises including interest rates, loan amounts, and use in MFI outreach and sustainability assessments for more complete insights. Rural Development Schemes are more accessible and valuable when group members and field personnel preserve moral and spiritual principles (RDS). According to the research, MFIs may help boost agriculture, which is vital to rural communities. Microfinance has the potential to provide excellent business possibilities since people experiencing poverty can thrive in small enterprises even with higher interest rates.

MFIs’ poverty reduction and impact on social inequality are balanced in the study. Despite improving long-term borrowers’ household wages and spending, MFIs have had little influence on savings and housing. This comprehensive approach highlights MFIs’ multifaceted role and the need for continued research to optimize poverty alleviation. Report: MFI policies and strategies must be customized to communities’ needs and conditions.

Many studies have been conducted on the effects of the intensity of microfinance programs on income inequality and how these effects vary throughout countries. According to studies, more intense microfinance reduces the income gap between the rich and the poor—empirical research links microfinance intensity to income disparity reduction. Varying nations have different impacts from microfinance on income disparity, underlining the need for a more sophisticated understanding of program intensity and income inequality.

Women’s self-sufficiency, microfinance, natural catastrophes, and economic inequalities have been studied. Research suggests that microfinance may help women become more autonomous in the face of environmental calamities. Research shows that microfinance helps women financially, but how environmental vulnerability impacts them is unknown. Female asset ownership and monthly savings have grown thanks to microfinance initiatives. More research is needed to understand how natural catastrophes, microfinance, and women’s self-sufficiency are linked.

Microfinance is linked to income inequality, inequality reduction, and women’s resistance to natural catastrophes. Microfinance program intensity reduces income disparity and empowers women, according to research. More study is needed to understand how microfinance and natural catastrophes affect women’s self-sufficiency internationally.

5. Conclusion

Comparative microfinance governance analysis and its effects on poverty and social injustice demand further empirical and theoretical investigation. Filling these gaps can help us understand MFI performance, environmental catastrophes, women’s self-sustainability, and how microfinance reduces poverty and income inequality.

Many research have studied how microfinance governance reduces poverty and inequality. However, many questions remain concerning this topic. Thus, further study is required to understand the intricate linkages between social inequality, poverty alleviation, and microfinance governance. Performance, MFI features, financing sources, organizational governance, and external contextual variables have been thoroughly investigated. However, little is known about how these attributes affect MFIs’ social and financial success under different governance and regulatory systems. Further research is required to understand governance processes that substantially impact MFI performance, social inequality, and poverty alleviation.

There is little quantitative research utilizing primary data sources to assess government-run microfinance programs from providers’ and customers’ perspectives. The study gap on women’s self-sufficiency, microfinance, and environmental calamities is clear. Microfinance may improve self-reliance among environmentally sensitive women, but more empirical study is required to fill gaps in the literature.

Our understanding of MFI performance, environmental disasters, microfinance, women’s self-sustainability, and how microfinance lowers poverty and income inequality would improve if these research gaps were filled. Further empirical and theoretical study is required to fully comprehend the intricate dynamics of microfinance governance and how it affects social inequality and poverty reduction.

This analysis of Bangladesh’s microcredit industry utilizes June 2022 MRA data to depict this essential financial ecosystem—a strong industry with 34.76 million active borrowers and 39.48 million members. Loan and disbursement statistics of Tk 771.80 billion and Tk 1313.67 billion demonstrate the sector’s financial significance. A successful microlender, Grameen Bank has 7.14 million borrowers and members. Government NGOs and commercial banks give, demonstrating Bangladesh’s microfinance diversity. Bangladesh’s socio-economic realities make microcredit services popular, according to statistics. These programs empower people with low incomes, especially women. The sector’s expansion and diversity demonstrate its ability to meet regional requirements, empowering people and boosting the economy.

Microfinance in Bangladesh takes a complex approach to business goals and poverty alleviation, as seen in this research [47]. The study highlighted the goals and operations of Microfinance Institutions (MFIs), Rural Development Schemes (RDs), and Microfinance Banks (MFBs), which serve different financial ecosystem functions.

The chapter shows how commercial profit pressures affect most MFBs’ and MFIs’ poverty alleviation goals. The commercialization of microfinance has led many organizations to emphasize the disadvantaged. This tendency may be due to a growing emphasis on financial sustainability and the rising costs of serving poorer clients. This tendency contradicts microfinance’s goals of poverty reduction and social welfare.

RDs prioritize social transformation and poverty eradication in this market above private interests. Because regulation is less strict, MFIs may adapt their financial strategies to serve low-income clientele profitably. They may have failed to reduce poverty in their adoption. Different policy frameworks that control these groups also affect their strategies. These organizations make operational and strategic decisions by balancing financial and social goals. According to the report, some MFIs no longer lend to new businesses, while others encourage early returns or use gold as collateral. Replacing standard non-collateralized microfinance techniques might restrict access to these services for low-income people.

Zero-interest emphasizes social empowerment and poverty elimination above profit. This strategy looks less subject to commercial forces, but its financial sector sustainability and scalability are unknown.

According to the research, Bangladesh’s microfinance business is at a crucial point. The business environment and financial sustainability may alter, but poverty must be eliminated. Managing competing duties is difficult. To remain profitable while serving low-income people, institutions must change their strategies. This balance determines how much microfinance reduces poverty and empowers the economy. Future regulations and initiatives in this industry must incorporate these dynamics to avoid profit maximization overshadowing microfinance’s primary goals.

5.1 Limitations

Quantitative MRA data dominate the analysis. Although this gives a general industry perspective, it does not address poverty, operating efficiency, or borrower happiness. This study’s findings on Bangladesh’s microcredit business may not apply to other cultures or economies. Trends and patterns in the microfinance sector change quickly, making June 2022 numbers less important.

5.2 Future study

Future research should include qualitative methods like interviews and case studies further to understand Microcredit’s Impact on borrowers and communities. Compare microcredit sectors in different nations to find best practices for Bangladesh. A longitudinal study will show Microcredit’s long-term impact on poverty and economic empowerment. In the changing financial landscape, digital technology may increase microcredit firms’ productivity, outreach, and customer service. How legislative and regulatory changes influence microcredit should be studied to improve governance and support. The June 2022 Bangladesh microcredit sector study stresses financial inclusion and poverty reduction. The study reveals microfinance’s growth and effectiveness, but future research should address its flaws and adapt to its changing nature.

Acknowledgments

The content of this article falls under the project within the Department of Business Administration Scheme (DEBA) at the International Islamic University Malaysia.

References

- 1.

Akhter J, Kun C. Sustainable empowerment initiatives among rural women through microcredit borrowings in Bangladesh. Sustainability. 2020; 12 (6):2275. DOI: 10.3390/su12062275 - 2.

Parvin S, Hossain B, Mohiuddin M, Cao Q. Capital structure, financial performance, and sustainability of micro-finance institutions (MFIs) in Bangladesh. Sustainability. 2020; 12 (15):6222. DOI: 10.3390/su12156222 - 3.

Murshid N, Murshid N. “innovations” during COVID-19: Microfinance in Bangladesh. Affilia. 2021; 37 (2):232-249. DOI: 10.1177/08861099211054024 - 4.

Nawaz S, Ramzan M, Shahid M. Relationship between microfinance and sustainable women entrepreneurial performance: The mediating role of social capital. NUML International Journal of Business & Management. 2021:70-88. DOI: 10.52015/nijbm.v16i1.56 - 5.

Barua S, Banerjee A. Impact of climatic shocks on household well-being: Evidence from rural Bangladesh. Asia-Pacific Journal of Rural Development. 2020; 30 (1-2):89-112. DOI: 10.1177/1018529120977246 - 6.

Ayayi A, Wijesiri M. Is there a trade-off between environmental performance and financial sustainability in microfinance institutions? Evidence from the south and Southeast Asia. Business Strategy and the Environment. 2022; 31 (4):1552-1565. DOI: 10.1002/bse.2969 - 7.

Schurmann A, Johnston H. The group-lending model and social closure: Microcredit, exclusion, and health in Bangladesh. Journal of Health Population and Nutrition. 2009; 27 (4). DOI: 10.3329/jhpn.v27i4.3398 - 8.

Li X, Gan C, Hu B. The impact of microcredit on women's empowerment: Evidence from China. Journal of Chinese Economic and Business Studies. 2011; 9 (3):239-261. DOI: 10.1080/14765284.2011.592352 - 9.

Debnath D, Acharjee D, Latif W, Wang L. Empowering women through microcredit in Bangladesh: An empirical study. International Journal of Financial Studies. 2019; 7 (3):37 - 10.

Santoso D, Gan C, Revindo M, Massie N. The impact of microfinance on Indonesian rural households' welfare. Agricultural Finance Review. 2020; 80 (4):491-506. DOI: 10.1108/afr-11-2018-0098 - 11.

Uddin MN. Role of Islamic microfinance institutions for sustainable development goals in Bangladesh. Journal of International Business and Management. 2020:1-12. DOI: 10.37227/jibm-2020-64 - 12.

Islam M. Role of Islamic microfinance in women's empowerment: Evidence from rural development scheme of Islami Bank Bangladesh Limited. ISRA International Journal of Islamic Finance. 2020; 13 (1):26-45. DOI: 10.1108/ijif-11-2019-0174 - 13.

Cull R, Morduch J. Microfinance, and economic development [Internet]. 2018. DOI: 10.4337/9781785360510.00030 - 14.

Sukmana R. Critical assessment of Islamic endowment funds (waqf) literature: Lesson for government and future directions. Heliyon. 2020; 6 (10):e05074. DOI: 10.1016/j.heliyon.2020.e05074 - 15.

Newman A, Schwarz S, Ahlström D. Microfinance, and entrepreneurship: An introduction. International Journal of Small Business and Entrepreneurship Research. 2017; 35 (7):787-792. DOI: 10.1177/0266242617719314 - 16.

Adurayemi A, Owualah I, Babajide A. MFBs client-enterprise profitability and loan failure in Ogun state Nigeria. IJASOS-International E-Journal of Advances in Social Sciences. 2019:386-393. DOI: 10.18769/ijasos.550363 - 17.

Chen J, Chang A, Bruton G. Microfinance: Where are we today, and where should the research go in the future? International Journal of Small Business and Entrepreneurship Research. 2017; 35 (7):793-802. DOI: 10.1177/0266242617717380 - 18.

Mader P. Rise and fall of microfinance in India: The Andhra Pradesh crisis in perspective. Strategic Change. 2013; 22 (1-2):47-66. DOI: 10.1002/jsc.1921 - 19.

Cull R, Demirgüç-Kunt A, Morduch J. Microfinance meets the market. The Journal of Economic Perspectives. 2009; 23 (1):167-192. DOI: 10.1257/jep.23.1.167 - 20.

Imai K, Azam S. Does microfinance reduce poverty in Bangladesh? New evidence from household panel data. Journal of Development Studies. 2012; 48 (5):633-653. DOI: 10.1080/00220388.2012.661853 - 21.

Uddin MN, Kassim S, Hamdan H, Saad MBN, Che Embi NA. Green microfinance promoting sustainable development goals (SDGs) in Bangladesh. Journal of Islamic Finance. 2021; 10 (1):11-18. Available from:https://www.researchgate.net/publication/351442117 - 22.

Haneef M, Pramanik A, Mohammed M, Amin M, Muhammad A. Integration of waqf-Islamic microfinance model for poverty reduction. International Journal of Islamic and Middle Eastern Finance and Management. 2015; 8 (2):246-270. DOI: 10.1108/imefm-03-2014-0029 - 23.

Razak DA, Hamdan H, Uddin MN. The effect of the demographic factors of micro-entrepreneur on financial literacy: Case of Amanah Ikthiar Malaysia (AIM). International Journal of Business, Economics and Law. 2020; 21 (3):47-56. Available from:https://www.researchgate.net/publication/343404101 - 24.

Hassan M, Alshater M, Hasan R, Bhuiyan A. Islamic microfinance: A bibliometric review. Global Finance Journal. 2021; 49 :100651. DOI: 10.1016/j.gfj.2021.100651 - 25.

Lensink R, Mersland R, Vu N, Zamore S. Do microfinance institutions benefit from integrating financial and nonfinancial services? Applied Economics. 2017; 50 (21):2386-2401. DOI: 10.1080/00036846.2017.1397852 - 26.

Uddin MdN, Hamdan H, Saad NB, Haque A, Kassim S, Embi NAC, et al. The governance structure of microfinance institutions: A comparison of models of sustainability and their implication on outreach. Asian Journal of Economics, Business and Accounting. 2022; 22 (19):104-123. DOI: 10.9734/ajeba/2022/v22i1930662 - 27.

Wahab N, Bin-Nashwan S, Chik M, Hussin M. Islamic social finance initiatives: An insight into bank Islam Malaysia Berhad’s innovative bangkit microfinance product. Isra International Journal of Islamic Finance. 2023; 15 (1):22-35. DOI: 10.55188/ijif.v15i1.483 - 28.

Calónico S, Cattaneo M, Titiunik R. Robust data-driven inference in the regression-discontinuity design. The Stata Journal. 2014; 14 (4):909-946. DOI: 10.1177/1536867x1401400413 - 29.

Hamdan H, Razak DA, Huridi H, Uddin N. Factors contributing to financial literacy among MSMEs in Klang Valley. Turkish Online Journal of Qualitative Inquiry (TOJQI). 2021; 12 (6):9223-9232. Available from:https://www.researchgate.net/publication/353646187 - 30.

El-Komi M, Croson R. Experiments in Islamic microfinance. Journal of Economic Behavior and Organization. 2013; 95 :252-269. DOI: 10.1016/j.jebo.2012.08.009 - 31.

Widiarto I, Emrouznejad A. Social and financial efficiency of Islamic microfinance institutions: A data envelopment analysis application. Socio-Economic Planning Sciences. 2015; 50 :1-17. DOI: 10.1016/j.seps.2014.12.001 - 32.

Xalane M, Salleh M. The role of Islamic microfinance for poverty alleviation in Mogadishu, Somalia: An exploratory study. International Journal of Management and Applied Research. 2019; 6 (4):355-365. DOI: 10.18646/2056.64.19-027 - 33.

Islam MA, Uddin MS, Thambiah S, Ahmed EM, Rauf MA. Do women’s attitudes matter in acceptance of Islamic microfinance? Evidence from Malaysia. East Asian Economic Review. 2023; 27 (1):61-85. DOI: 10.11644/KIEP.EAER.2023.27.1.418 - 34.

Fianto B, Gan C, Hu B, Roudaki J. Equity financing and debt-based financing: Evidence from Islamic microfinance institutions in Indonesia. Pacific-Basin Finance Journal. 2018; 52 :163-172. DOI: 10.1016/j.pacfin.2017.09.010 - 35.

Nurasyiah A. An empirical study of Islamic microfinance performance for poor family: Maqashid al-sharia perspective. Afebi Islamic Finance and Economic Review. 2020; 3 (01):46. DOI: 10.47312/aifer.v3i01.253 - 36.

Neves M, Monteiro J, Leal C. Determinants of banking profitability in Portugal and Spain: Evidence with panel data [Internet]. 2022. DOI: 10.5772/intechopen.103142 - 37.

Ashraf M. Effects of demographic factors on women's participation in the Islamic microfinance scheme: An analysis using the theory of bounded rationality. Journal of Islamic Accounting and Business Research. 2022; 13 (7):1018-1037. DOI: 10.1108/jiabr-09-2020-0275 - 38.

Uddin N, Pramanik AH, Haque A, Hamdan H. Assessment of Islamic microfinance on poverty reduction in Bangladesh. International Journal of Islamic Marketing and Branding. 2020; 5 (4) - 39.

Porter ME. The structure within industries and companies’ performance. The Review of Economics and Statistics. 1 May 1979:214-227 - 40.

Hair JF, Celsi M, Money A, Samouel P, Page M. The Essentials of Business Research Methods: Third Edition2015. pp. 1-494. DOI: 10.4324/9781315716862 - 41.

Bhimani A. Digital data and management accounting: Why we need to rethink research methods. Journal of Management Control. 2020; 31 (1-2):9-23. DOI: 10.1007/s00187-020-00295-z - 42.

Maione C, Barbosa RM. Recent applications of multivariate data analysis methods in the authentication of rice and the most analyzed parameters: A review. Critical Reviews in Food Science and Nutrition. 2019; 59 (12):1868-1879. DOI: 10.1080/10408398.2018.1431763 - 43.

Nahar L, Uddin MN. Financial performance of microfinance institutions in South Asia. In: Islam AA, Büşra Y, Ersin A, Ahmed Khuhro A, editors. South Asia: State, Society and Politics. 1st ed. Nobel Publishing Group; 2023. p. 523-540. Available from: https://www.researchgate.net/publication/372746027 . - 44.

Ahmed M. Grameen Bank vs. RDS of IBBL: A comparative analysis. Bangladesh Journal of Islamic Thought BIIT. 2008; 4 :5 - 45.

Uddin MN, Nahar L, Saad N. Empowering Rohingya refugees through Islamic microfinance: Exploring prospects and challenges in Bangladesh. Journal of Islamic Social Finance. 2023a; 1 (1):13-23. Available from:https://www.researchgate.net/publication/372788441 - 46.

Uddin MN, Nahar L, Bt Kaseem S, Bt SN. Factors affecting financial literacy among micro, small, and medium-sized enterprises (MSMEs) in Bangladesh and Malaysia. Uluslararası Öğrenci Sempozyumu. 2023b:151-166. Available from: www.internationalstudentsymposium.com - 47.

Uddin N, Benabderrahmane O. The effect of conventional and Islamic microfinance on poverty alleviation in Bangladesh. Milev Journal of Research and Studies. 2019; 5 (2):464-481. DOI: 10.58205/mjrs.v5i2.1255