Open Access is an initiative that aims to make scientific research freely available to all. To date our community has made over 100 million downloads. It’s based on principles of collaboration, unobstructed discovery, and, most importantly, scientific progression. As PhD students, we found it difficult to access the research we needed, so we decided to create a new Open Access publisher that levels the playing field for scientists across the world. How? By making research easy to access, and puts the academic needs of the researchers before the business interests of publishers.

We are a community of more than 103,000 authors and editors from 3,291 institutions spanning 160 countries, including Nobel Prize winners and some of the world’s most-cited researchers. Publishing on IntechOpen allows authors to earn citations and find new collaborators, meaning more people see your work not only from your own field of study, but from other related fields too.

A growing literature is devoted to understanding how public entities can enhance their methods of reporting information to establish a genuine dialog with stakeholders in general and citizens in particular. In the current context, the challenge of achieving sustainable development has impacted various sectors. The public sector is implementing a series of actions aimed at ensuring transparency and environmental, social, and governance sustainability. Public entities disseminate information related to these actions through various reporting tools, attempting to meet the interests of citizens. However, typically, this kind of information is not included in traditional financial reports. The aim of the study can be summarized by illustrating the advantages of a relatively new reporting tool in Italy. Contributing to previous studies, we investigate, using a theoretical-deductive methodology, how governmental entities can improve institutionalization, legitimacy, and stakeholder relations through a new reporting tool known as “Integrated Popular Reporting”. The study highlights how Integrated Public Reporting (IPR) fosters citizen participation in budgeting, improves accessibility to reporting, and promotes accountability. It emphasizes the importance of IPR in enhancing quality of life and transparency, offering valuable insights for policymakers and standard setters.

Department of Economics, University of Campania “L. Vanvitelli”, Capua (Caserta), Italy

Danilo Tuccillo

Department of Economics, University of Campania “L. Vanvitelli”, Capua (Caserta), Italy

Andrea Rey

Department of Economics, Management and Institutions, University of Naples “Federico II”, Naples, Italy

Maria Rita Filocamo

Department of Economics, Management and Institutions, University of Naples “Federico II”, Naples, Italy

*Address all correspondence to: francesco.agliata2@unicampania.it

1. Introduction

The number of studies focusing on non-financial reporting formats adopted by public sector organizations (PSOs) is steadily growing [1]. Indeed, the government plays a central role in managing financial sustainability, and its proactivity in reporting would signify both anticipating regulation and social expectations, as well as taking on a leadership role in promoting sustainability. A range of methods exists to engage citizens in financial sustainability decision-making, encompassing popular reporting (PR), integrated reporting (IR), sustainability reporting (SR), and intellectual capital reporting (ICR). Noteworthy is the rising attention and utilization of PR in the public sector.

Thus, the following research question is derived:

RQ: Can local authorities enhance institutionalization, legitimacy and stakeholder relations through popular integrated reporting?

By combining and integrating the two main evolutionary approaches mentioned earlier – integrated reporting and popular reporting – a communicative model is created that enhances the informational effectiveness of local authorities toward their reference communities. However, it is essential that the structure, content, and communication methods are carefully defined, giving due value to already codified principles and established practices to optimize the overall effectiveness of the tool known as Integrated Popular Reporting (IPR). Governments should be inclined to create an IPR because citizens now demand more than what is provided in traditional financial reports. The development of an IPR should consider the Recommended Practice Guideline (RPG 1) on “Reporting on the Long-Term Sustainability of an Entity’s Finances”, issued by the International Public Sector Accounting Standards Board [14], and the “International Integrated Reporting Framework” (IR Framework) developed by the International Integrated Reporting Council (IIRC) [2]. In line with RPG 1, an IPR should offer information on fiscal sustainability regarding the impact of current policies and decisions on future financial inflows and outflows [14].

This chapter identifies a model of IPR capable of bridging the legitimacy gap generated by Integrated Reporting. Through a theoretical-deductive methodology, it aims to pinpoint the characteristics that an integrated popular report should possess to enhance institutionalization, legitimacy, and stakeholder relations. The following section outlines the theoretical framework concerning transparency and sustainability in the broader public context, along with the system-oriented theories for sustainability reporting analysis. Section 3 highlights the main features of sustainability reporting, the transition to the so-called integrated reporting, and the key differences with popular reporting. Section 4 analyzes the implementation of integrated popular reports in the public sector and explores how IPR could enhance institutionalization, legitimacy, and stakeholder relations. The chapter concludes with a summary of the information presented and provides implications for further research.

2. Transparency and financial sustainability in public sector

The ability to discern the inner workings of governments defines governmental transparency [3]. Governmental transparency has long been a subject of debate among both scholars and professionals, playing a crucial role in ensuring accountability [4]. Moreover, while transparent financial reporting aids organizations in showcasing accountability [5], accountability encompasses information about financial sustainability [6]. Accountability, which entails the process of keeping the public well-informed while also ensuring that authorities are held responsible, consists of three stages: information, discussion, and outcomes [7]. The absence of governmental transparency and freedom of information makes it significantly challenging to ensure accountability for the actions of elected and appointed officials [4]. Governments worldwide are actively engaged in various transparency initiatives, especially with the aim of fostering greater citizen engagement, and they are identified as the most significant group in governmental financial reporting [8, 9, 10]. Indeed, “intelligent” accountability is crucial, enabling citizens to access public data and openly discuss it with authorities, shifting from a monologic accounting approach to a dialogic one [11]. Furthermore, making a public or private organization more transparent would facilitate accountable and sustainability-oriented decisions [3].

Over time, a multitude of studies have been undertaken to pinpoint the factors that erode the financial sustainability of local entities, offering theoretical and empirical evidence rooted in the socio-economic environments within which local governments operate [12].

Moreover, studies related to financial sustainability have focused on various aspects, considering both financial and non-financial factors. Although the utility of government financial statements for reporting the financial sustainability of public sector entities is acknowledged, the literature has not yet sufficiently emphasized financial sustainability reports [13]. Currently, there is no universally agreed-upon definition of “financial sustainability”. However, within the scope of this chapter, it is referenced as the “ability to manage its financial capacity in the short and long term while maintaining the level of services” [13]. Certainly, this necessitates implementing policies capable of delivering public services to current generations without compromising the needs of future ones.

In the first RPG, the International Public Sector Accounting Standards Board (IPSASB), characterized long-term fiscal sustainability as an entity’s capacity to fulfill service delivery and financial obligations both presently and in the future [14]. The RPG delineated three interrelated dimensions of enduring financial sustainability: service, revenue, and debt. The service aspect encompasses the quantity and quality of services offered to recipients and beneficiaries. The revenue dimension involves levels of taxation and other income sources. The debt dimension focuses on the levels of indebtedness within a specific timeframe, including the capability to meet financial commitments [14]. This document underscores the significance of long-term financial sustainability, emphasizing its social and environmental implications, and underscores the crucial role of disseminating information on these matters. It is important to highlight that the limited adoption of accrual accounting poses challenges in evaluating the financial well-being of governmental entities. Despite the initiatives by the IPSASB, numerous government bodies continue to formulate their financial statements using cash or modified-cash/modified-accrual methods. Consequently, the absence of accrual accounting hinders a comprehensive assessment of financial health, leading to a partial measurement and obscuring critical economic factors, including details about infrastructure assets [15].

Interest in this research topic is on the rise in the literature, and an increasing number of scientific studies are acknowledging the potential alignment of the integrated reporting tool with the popular reporting model. In fact, the significance of sustainability-related aspects has become indispensable in the eyes of stakeholders and has indirectly impacted the traditional reporting practices adopted by companies.

2.1 System-oriented theories

The analysis of sustainability reporting relies on fundamental system-oriented theories, namely legitimacy theory, stakeholder theory, and institutional theory [16]. According to these three perspectives, a company is not involved in a “rational” economic activity but must consistently navigate its social, institutional, and political context. This is crucial due to the presence of numerous stakeholders with whom the company must interact and who are impacted by its activities. In relation to the first of the aforementioned theories, the fundamental premise of legitimacy theory is that a business does not automatically survive in the long run but must receive legitimacy from society. According to references [17, 18], a “social contract” arises between the company and the society, within which explicit terms define the set boundaries and implicit terms encompass its expectations [19]. This judgment is solely the prerogative of entities identified as conferring publics, entities deemed by the company to possess the optimal combination of attributes required to influence or revoke legitimacy [20]. If the company’s actions deviate from societal expectations, a phenomenon known as the legitimacy gap will emerge [16, 21]. The stakeholder theory considers the importance of the relationship between the company and every individual who can be influenced by the company’s actions and, in turn, influence its decisions, commonly referred to as a stakeholder [22]. This theory emphasizes the interdependence of the relationships between the company and stakeholders, and it is divided into two branches: (1) normative stakeholder theory and (2) positive stakeholder theory. As outlined in the subsequent paragraph 3, these theories guide the company in a varied manner to address the informational needs of stakeholders [16]. Lastly, institutional theory is based on the idea that a firm is influenced by pressures exerted by institutions (i.e., societies). Several authors [23, 24, 25] view institutions as “taken for granted”, or rather, the social framework of norms and values in which businesses function is presumed regarding economic behaviors considered appropriate or acceptable. The two main dimensions of this theory are isomorphism and decoupling [19]. According to isomorphism, companies conform to other “mythologized” companies within society because they are perceived as “appropriate enterprises” [25]. However, a company is deemed decoupled when it adopts a deceptive stance, as its internal processes do not align with those formally communicated externally [16]. Moreover, this behavior within the context of sustainable information reporting is identified as greenwashing: it involves companies attempting to present an external image of being “environmentally friendly” while they are misleading the consumer.

3. The sustainability reporting through the lens of system-oriented theories

The communication of information through sustainability reporting can be interpreted by considering the so-called system-oriented theories, namely legitimacy theory, stakeholder theory, and institutional theory. These three theories are used to understand the managerial motivations behind the publication of sustainability information [26]. Starting from legitimacy theory, sustainability reporting may enable the achievement, maintenance, or restoration of legitimacy that was previously lost over time. Indeed, reporting practices can constitute a genuine strategy for a business. Through the disclosure of specific information to the conferring public, the company can intentionally shift attention to positive aspects rather than those that might expose a legitimacy gap [16]. In this regard, based on an analysis conducted on a sample of 50 companies listed on the Milan Stock Exchange [27], which issue sustainability reporting, it emerges that this tool is used to disclose social and environmental information to enhance credibility and strengthen trust within the community. Another crucial aspect influencing the strategic use of sustainability reporting is the distinction between the two branches identified in the legitimacy theory literature: organizational and institutional. In organizational legitimacy theory, legitimacy is regarded as equivalent to any other productive factor instrumental in business activity. Therefore, the company’s ability to disseminate specific information through sustainability reports enables it to control its legitimacy status [28]. This stands in contrast to institutional legitimacy theory, where the legitimization process is uncontrollable as it is subject to institutional evaluation. The institutional legitimacy theory aligns with the institutional theory in the same direction: the premise is that the institution drives companies to adapt their characteristics and sustainability reporting practices to the institutional context in which they operate. Therefore, in accordance with institutional theory, a company’s decisions regarding the features of its sustainability reporting and its assurance are shaped by political, social, and economic systems [29]. The stakeholder theory, depending on whether it falls under the “normative/ethical” or “positive/managerial” branch [17, 30, 31, 32], envisions different ways of incorporating information within sustainability reporting. The primary distinction between the two theories is that in the former, the relevance of stakeholders is not dependent on their economic power; consequently, all stakeholders should receive the same treatment, and sustainability reporting must fulfill this obligation by providing information to all stakeholders. In the “positive” or “managerial” theory, stakeholders with greater resources – considered essential to the survival of the firm – are classified as “more relevant”, and their interests will be prioritized. As mentioned earlier, this also leads to differences in terms of sustainable information’s disclosure. Indeed, sustainability reporting within this managerial perspective serves a strategic function because it must meet the expectations of the most relevant stakeholders and prevent their involvement in reporting practices from negatively impacting the company.

3.1 Integrated reporting vs. popular reporting

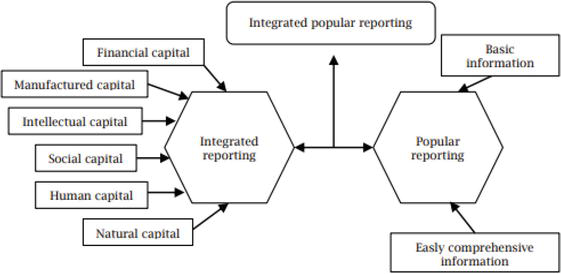

Various companies, organizations, universities, and standard setters have long decided to come together in an international association known as the IIRC. The aim is to implement integrated reporting and define requirements, principles, and criteria in a unified model. The application of this model helps organizations in reporting social, environmental, and governance information, highlighting their various interconnections [33]. Integrated reporting is described as a process rooted in integrated thinking, resulting in a comprehensive periodic report that communicates value creation over time and provides information on various aspects of an organization’s value creation [34]. The integrated report serves as a condensed overview detailing how an organization’s strategy, governance, performance, and prospects, within the context of its external environment, contribute to value creation in the short, medium, and long term [34]. Choosing to adopt integrated reporting requires a shift from an analytical vision to a systemic view, merging traditionally separate information systems [35]. Primarily, the organization is understood as a synthesis of six capital categories, spanning financial, productive, intellectual, human, social, and relational and all these must be expressed in a coordinated manner, emphasizing synergy within a single report [6]. While traditional reports do not disclose information about intangible assets, integrated reporting also communicates information about intellectual capital and value creation [36, 37]. Certainly, an aspect of paramount importance in introducing integrated reporting in the public sector is the resistance to change and technological limitations within public entities [38]. However, the activities carried out by public organizations can have a truly significant impact on achieving the so-called “sustainable development”, along with numerous other benefits, including gaining greater trust from citizens and stakeholders in general. It provides a clearer articulation of objectives, thereby improving the decision-making process and consequently fostering trust within the entity [39]. Despite its potential strengths, this report is not presented concisely and engagingly, often failing to effectively capture the interest of citizens. To address this issue, it would be necessary to create a report that is accessible to everyone and easier to read. In the United States and Canada, and sporadically in Italy, a report named the “popular report” (PR) has been disseminated across various states and cities for several years; this report provides financial information pertaining to governmental entities, as indicated by [40]. The popular report serves the purpose of disseminating financial information from a government entity in a simple and intuitive manner, aiming to reach a broader audience, including those who do not have a background in public finance. As mentioned earlier, it is particularly widespread in the United States and Canada, being promoted by three major government associations, namely the Government Finance Officers Association (GFOA), Governmental Accounting Standards Board (GASB), and the Association of Government Accountants (AGA), each of which provides its own guidelines [41]. In particular, the GFOA has instituted a prize system since 1991 to promote the implementation of the Popular Annual Financial Report (PAFR) [42], while the GASB promotes the so-called SEA report, or “service effort and accomplishment” (SEA) report, issuing guidelines in July 2010 [42, 43, 44]. Finally, the AGA promotes the so-called citizen-centric reporting (CCR), also establishing a prize system based on the best SEA reports following GASB guidelines. It is a brief document that, within four pages, should include strategic objectives, missions and services, cost-revenue related to the identified services and missions, and finally, future challenges. However, when the term PR is referred to in this study, it implies a reference to the document specified by the GFOA, as it is the most widely used in the current context.

3.2 Integrated popular reporting

In the continuum between IR and PR, an instrument for reporting, known as Integrated Popular Reporting (IPR) has been pinpointed. Its purpose is to cater to the informational needs of a substantially wider audience, extending beyond those individuals possessing technical skills. Integrated popular reports are not currently employed by governmental entities; hence, this section offers a theoretical examination of a prototype integrated popular report for a public authority. Specifically, it will scrutinize the content that an IPR should embody to serve as a tool for social legitimation or an institutional reporting tool. This novel report seeks to enhance the communication between the government and its citizens, fostering increased citizen engagement in financial matters and fiscal policy decisions [45]. The formulation of an integrated popular report should carefully consider the Recommended Practice Guidelines (RPG 1) pertaining to the disclosure of “Long-Term Sustainability of an Entity’s Finances”. These guidelines are issued by the IPSASB. Additionally, it should consider the “International Integrated Reporting Framework” (IR Framework) developed by the IIRC [2]. Specifically, the report aims to educate citizens about policy-related challenges and cultivate stronger public support for governmental initiatives [46]. This new reporting tool would have the features illustrated by other authors [47], depicted in Figure 1.

Figure 1.

Reporting tools comparison. Source: Cohen and Karatzimas ([47], p. 456).

As mentioned earlier, the purpose of an integrated popular report is to address a legitimacy gap associated with integrated reporting. Consequently, it should meet the emerging information requirements of citizens emphasized in the literature, aiming not only to provide information about past financial performances but also expectations for the future. Additionally, it should ensure greater transparency regarding the financial situation of their municipality. It should primarily include details regarding the economic viability of the urban area. It should also cover aspects associated with the habitability of a city, enabling a comprehensive assessment of the standard of living and the possibility of making comparisons with cities where residents may enjoy a superior quality of life [48].

Specifically, the IR Framework exclusively identifies a series of questions that need to be addressed when drafting the report [34]. These include:

Overview of the organization and the external environment: “Under what circumstances does it work?”

Governance: “How does the organization’s governance structure support its ability to create value in the short, medium, and long term?”

Business model: “What is the business model?”

Opportunities and risks: “What are the specific opportunities and risks that influence the ability to create value along the time horizon?”

Strategy and allocation of resources: “What is the goal of the organization and how do you intend to achieve it?”

Performance: “To what extent has the organization achieved its strategic objectives, and what are the results obtained in terms of effects on capital?”

Future perspectives: “What challenges and uncertainties will the company likely have to face in pursuing its strategy, and what are the potential implications for the business model and future performance?”

The content of IPR should be designed to overcome a substantial communication obstacle arising from the limited familiarity and proficiency in public finance and government budgets among the primary recipients of the generated information: the citizens. This aligns with the transparency principles underpinning the legal regulations governing public administrations and the budgets they generate. It is crucial to engage citizens so that they are not mere spectators but rather are encouraged to actively participate in the collective decision-making process. Therefore, from a content perspective, the primary focus should be on fiscal sustainability: an IPR should provide information on fiscal sustainability regarding the impact of current policies and decisions on future inflows and outflows [14]. This way, information is obtained regarding government revenue sources and major taxes, as well as expenses and costs of public services, the cost and impact of investment projects, the amount, cost, and sustainability of debt, and the outcomes of government policies [49]. Moreover, citizens should be informed about potential tax increases and the correlation between what they pay and the quality of the service received, allowing them to make a concrete assessment of the quality of life in the cities where they currently reside or would like to move [48]. The dissemination methods of the IPR constitute an additional innovative element, making it much more practical for citizens. Indeed, it can be distributed via email, published on the government’s website, sent to citizens upon request, or distributed during specific events. As mentioned above, aiming for comprehensibility for all, technical terms should be avoided [2, 42], and it should be kept very concise (maximum eight pages) to make its reading similar to that of a newspaper, specifying the meaning of any acronyms.

In addition, a recent study [50] outlined the pillars that characterize the IPR and distinguish it from other social reporting tools, as observable in Table 1.

Understanding: All stakeholders, but especially citizens and governance, can, or rather, be capable of reading and understanding this reporting tool.

Inclusion: The language used is non-technical and takes into account the demographic characteristics of the population. If the educational level is lower, there will be a greater use of graphical information. Moreover, new technologies, including social platforms, are utilized to identify the needs of the population.

Dissemination: In comparison to traditional social reporting, this reporting involves a comprehensive dissemination plan reaching all stakeholders, not relying solely on institutional channels;

Integrated View: Involves a unified perspective derived from both the consolidated and integrated financial statements, providing a clear representation of the group’s responsibilities to key external stakeholders. Additionally, it includes a detailed depiction of the personnel structure, impact on the context, service delivery, and interrelationships among key elements of the consolidated financial statements, along with presenting the value generated and absorbed by the group.

Representative Need: The representation of information depends on the information needs and is done in a concise manner, unrestricted by any standard, highlighting key elements (referred to as “dialogic tools”).

Report

Other social reports

Integrated Popular Reporting

Understanding

X

Inclusion

X

Dissemination

X

Integrated View

X

Representative Need

X

Use of Emerging Technologies for Needs Assessment

X

Dialogical Approach through the Use of Social Platforms

X

Presence of Impact Assessment Orientation

X

Table 1.

The pillars of integrated popular reporting. Source: Biancone et al. ([50], p. 29).

As can be observed, the last three pillars, “Use of Emerging Technologies for Needs Assessment”, “Dialogical Approach through the Use of Social Platforms”, and “Presence of Impact Assessment Orientation”, are closely connected to those mentioned above. The communication of the report [50] proceeds through an initial presentation conference of the document aimed at an exchange of information. During this session, the aspects of the report are explained, and there is an opportunity to get to know the stakeholders and identify their primary interests. This approach helps understand the target audience of the IPR (youth-adults-businesses-media) and the communication method that is consequently most suitable for each category.

Recently, numerous studies have been published regarding reporting tools in general, and, more specifically, in the public sector, given the need to improve levels of transparency and accountability of government entities. Indeed, new tools for reporting have been developed to address the growing information needs of citizens and changes in governmental practices, exemplified by the IPR. In this chapter, a theoretical-deductive analysis has been undertaken to outline if this still relatively new tool can overcome the limitations of Integrated Reporting, and if it can represent a tool for social legitimation, improving relationships with stakeholders. The IPR, functioning as an integrated report, should consolidate both financial and non-financial information into a single document. It should be succinct and communicate to citizens the financial status of the governmental entity in a manner that is clear and encouraging for individuals unfamiliar with accounting and financial terminology [42, 2]. Within the financial domain, specific attention should be directed toward information concerning financial sustainability. Consequently, ratios that are instrumental in assessing the financial well-being of a governmental entity should be incorporated. This allows citizens to comprehend the utilization of their taxes, the extent of investments in infrastructure, and the standard and quality of services offered by governmental entities. Armed with this knowledge, citizens can better contribute to supporting governmental entities through tax revenues. To engage citizens effectively, the dissemination of the IPR should leverage information and communication technologies (ICTs) tools, such as the Internet, email, and social media, and should be written at a newspaper reading level. The opportunity for citizens to contribute ideas and opinions through their social media significantly enhances public value, making them part of the value creation process (or co-producer). On the other hand, the heightened citizen engagement with this emerging tool, facilitated in part by the integration of new technologies – in particular social media – may prompt policymakers to develop a deeper understanding and appreciation for this reporting mechanism. They may more readily perceive the strengths (and potential weaknesses) of IPR, thus potentially fostering a more informed approach to its implementation and utilization within governmental contexts. From the theoretical analysis conducted, it can be inferred that IPR serves as a tool capable of enhancing the decision-making process between stakeholders – in particular citizens – and public administrations. Public administrations must ensure greater transparency toward stakeholders who, thanks to this tool, can overcome the legitimacy gap imposed by Integrated Reporting, which previously served merely as an institutional signaling tool. The IPR surpasses the traditional communication paradigm between the government and citizens that hindered citizens’ access from the outset. The increased involvement of individual citizens, who indirectly become part of the budgeting process and can read this reporting even without any technical skills, has positive effects on both the level of accountability and the quality of life in a specific area. This study contributes new insights into an area that has received limited attention, providing valuable information for government managers and those responsible for setting standards. It emphasizes how an IPR can serve as a suitable tool to address the need for transparency regarding financial sustainability and encourage citizen engagement. However, the research has some limitations associated with being a preliminary theoretical analysis; thus, it does not attempt to delve into the empirical implications of the integrated popular report. This is undoubtedly due to the current limited practical diffusion of the IPR. Future research in this direction might shed light on these aspects, addressing the research gap related to the absence of empirical evidence.

1.Manes-Rossi F, Nicolò G, Argento D. Non-financial reporting formats in public sector organizations: A structured literature review. Journal of Public Budgeting, Accounting & Financial Management. 2020;32(4):639-669. DOI: 10.1108/JPBAFM-03-2020-0037

2.Aversano N, Tartaglia Polcini P, Sannino G, Agliata F. Integrated popular reporting as a tool for citizen involvement in financial sustainability decisions. In: Financial Sustainability of Public Sector Entities. Cham: Palgrave Macmillan; 2019. pp. 185-205. DOI: 10.1007/978-3-030-06037-4_10

3.Gupta A, Boas I, Oosterveer P. Transparency in global sustainability governance: To what effect? Journal of Environmental Policy & Planning. 2020;22(1):84-97. DOI: 10.1080/1523908X.2020.1709281

4.Piotrowski SJ, Van Ryzin GG. Citizen attitudes toward transparency in local government. The American Review of Public Administration. 2007;37(3):306-323. DOI: 10.1177/02750740062967

5.Nakmahachalasint O, Narktabtee K. Implementation of accrual accounting in Thailand’s central government. Public Money & Management. 2019;39(2):139-147. DOI: 10.1080/09540962.2018.1478516

6.Agliata F, Tuccillo D, Rey A, Filocamo MR. The new frontiers of reporting for governmental financial sustainability. Corporate Ownership & Control. 2022;19(3):64-73. DOI: 10.22495/cocv19i3art4

7.Mulgan R. Holding Power to Account. London: Palgrave Macmillan UK; 2003. DOI: 10.1057/9781403943835

8.Manes Rossi F. New development: Alternative reporting formats: A panacea for accountability dilemmas? Public Money and Management. 2019;39(7):528-531. DOI: 10.1080/09540962.2019.1578540

9.Van Helden J, Reichard C. Making sense of the users of public sector accounting information and their needs. Journal of Public Budgeting, Accounting & Financial Management. 2019;31(4):478-495. DOI: 10.1108/JPBAFM-10-2018-0124

10.Daniels JD, Daniels CE. Municipal financial reports: What users want. Journal of Accounting and Public Policy. 1991;10(1):15-38. DOI: 10.1016/0278-4254(91)90018-F

11.Roberts J. No one is perfect: The limits of transparency and an ethic for ‘intelligent’ accountability. Accounting, Organizations and Society. 2009;34(8):957-970. DOI: 10.1016/j.aos.2009.04.005

12.Navarro Galera AN, de los Ríos Berjillos A, Lozano MR, Valencia PT. Transparency of sustainability information in local governments: English-speaking and Nordic cross-country analysis. Journal of Cleaner Production. 2014;64:495-504. DOI: 10.1016/j.jclepro.2013.07.038

13.Caruana J, Brusca I, Caperchione E, Cohen S, Rossi FM. Financial Sustainability of Public Sector Entities: The Relevance of Accounting Frameworks. Palgrave Macmillan. Switzerland AG: Springer Nature; 2018. DOI: 10.1007/978-3-030-06037-4

14.International Public Sector Accounting Standards Board (IPSASB). Recommended practice guideline. Reporting on the long-term sustainability of an entity’s finances. 2013. Available from: https://www.ipsasb.org/publications/recommended-practice-guideline-1

15.Lapsley I, Mussari R, Paulsson G. On the adoption of accrual accounting in the public sector: A self-evident and problematic reform. European Accounting Review. 2009;18(4):719-723. DOI: 10.1080/09638180903334960

16.Zampone G. IL sustainability reporting nelle imprese italiane quotate. Profili teorici e applicativi. 2023

17.Deegan C, Sam kin, G. New Zealand Financial Accounting. Sydney, Australia: McGraw-Hill; 2009

19.Fernando S, Lawrence S. A theoretical framework for CSR practices: Integrating legitimacy theory, stakeholder theory and institutional theory. Journal of Theoretical Accounting Research. 2014;10(1):149-178

20.O’Donovan G. Legitimacy theory as an explanation for corporate environmental disclosures [Doctoral dissertation]. Victoria University of Technology; 2000. DOI: 10.12785/ijbsa/020104

21.Sethi SP. A conceptual framework for environmental analysis of social issues and evaluation of business response patterns. Academy of Management Review. 1979;1:63-74. DOI: 10.2307/257404

22.Freeman RE. Strategic Management: A Stokcholder Approach. Boston: Pitman; 1984

24.Greenwood R, Suddaby R. Institutional entrepreneurship in mature fields: The big five accounting firms. Academy of Management Journal. 2006;49(1):27-48. DOI: 10.5465/AMJ.2006.20785498

25.Boxenbaum E, Jonsson S. Isomorphism, diffusion and decoupling: Concept evolution and theoretical challenges. The Sage Handbook of Organizational Institutionalism. 2017;2:77-101

27.Vitolla F, Rubino M. Legitimacy theory and sustainability reporting. Evidence from Italy. In: Vrontis D, Weber Y, Tsoukatos T, editors. 10th Annual Conference of the EuroMed Academy of Business. Vol. 1, No. 1. Global and National Business Theories and Practice: Bridging the Past with the Future. EuroMed Press; 2017. pp. 1835-1848

28.Suchman MC. Managing legitimacy: Strategic and institutional approaches. Academy of Management Review. 1995;20(3):571-610. DOI: 10.2307/258788

29.Cho CH, Michelon G, Patten D, Roberts RW. CSR report assurance in the USA: An empirical investigation of determinants and effects. Sustainability Accounting, Management and Policy Journal. 2014;5(2):130-148. DOI: 10.1108/SAMPJ-01-2014-0003

30.Gray R, Owen D, Adams C. Accounting & Accountability: Changes and Challenges in Corporate Social and Environmental Reporting. London: Prentice Hall; 1996

31.Guthrie J, Petty R, Ricceri F. The voluntary reporting of intellectual capital: Comparing evidence from Hong Kong and Australia. Journal of Intellectual Capital. 2006;7(2):254-271. DOI: 10.1108/14691930610661890

32.Gray R, Owen D, Adams C. Some theories for social accounting?: A review essay and a tentative pedagogic categorisation of theorisations around social accounting. In: Freedman M, Jaggi B, editors. Sustainability, Environmental Performance and Disclosures. Bingley: Emerald; 2009. pp. 1-54

33.Lombardi R. The corporate sustainability reporting and disclosure. In: The Going-Concern-Principle in Non-Financial Disclosure: Concepts and Future Challenges. Cham: Springer International Publishing; 2021. pp. 31-77. DOI: 10.1007/978-3-030-81127-3

34.International Integrated Reporting Council (IIRC). The international integrated reporting framework. 2013. Available from: https://integratedreporting.org/wp-content/uploads/2013/12/13-12-08-the-international ir-framework-2-1.pdf

35.White A. The five capitals of integrated reporting: Toward a holistic architecture for corporate disclosure. In: The Landscape of Integrated Reporting. Cambridge: Harvard Business School; 2010. pp. 29-32

36.Dumay J, Bernardi C, Guthrie J, Demartini P. Integrated reporting: A structured literature review. Accounting Forum. Vol. 40, No. 3. 2016. pp. 166-185. DOI: 10.1016/j.accfor.2016.06.001

37.de Villiers C, Hsiao PCK. Integrated reporting and the connections between integrated reporting and intellectual capital. In: The Routledge Companion to Intellectual Capital. London: Routledge; 2017. pp. 483-491. DOI: 10.4324/9781315393100-30

38.Manes-Rossi F. Is integrated reporting a new challenge for public sector entities? African Journal of Business Management. 2018;12(7):172-187. DOI: 10.5897/AJBM2018.8498

39.Eccles RG, Krzus MP, Casadei A. Report integrato. Rendicontazione integrata per una strategia sostenibile. Forlì, Italy: Philantrophy; 2012

40.Biancone P, Secinaro S, Brescia V. Popular report and consolidated financial statements in public utilities. Different tools to inform the citizens, a long journey of the transparency. International Journal of Business and Social Science. 2016;7(1):111-124

41.Biondi L, Bracci E. Sustainability, popular and integrated reporting in the public sector: A fad and fashion perspective. Sustainability. 2018;10(9):3112. DOI: 10.3390/su10093112

42.Yusuf J-E, Jordan MM, Neill KA, Hackbart M. For the people: Popular financial reporting practices of local governments. Public Budgeting & Finance. 2013;33(1):95-113. DOI: 10.1111/j.1540-5850.2013.12003.x

43.Biancone PP, Secinaro S. Popular Financial Reporting. Torino, Italy: Giappichelli Editore; 2015

44.Biancone P, Secinaro S, Brescia V. The popular financial reporting: Focus on stakeholders—The first European experience. International Journal of Business and Management. 2016;11(11):115-125. DOI: 10.5539/ijbm.v11n11p115

45.Franklin AL, Ebdon C. Democracy, public participation, and budgeting: Mutually exclusive or just exhausting? In: Box RC, editor. Democracy and Public Administration. New York, NY: ME Sharpe; 2015. pp. 84-106

46.Irvin RA, Stansbury J. Citizen participation in decision making: Is it worth the effort? Public Administration Review. 2004;64(1):55-65. DOI 10.1111/j.1540-6210.2004.00346.x

47.Cohen S, Karatzimas S. Tracing the future of reporting in the public sector: Introducing integrated popular reporting. International Journal of Public Sector Management. 2015;28(6):449-460. DOI: 10.1108/IJPSM-11-2014-0140

48.Prado-Lorenzo J-M, García-Sánchez I-M, Cuadrado-Ballesteros B. Sustainable cities: Do political factors determine the quality of life? Journal of Cleaner Production. 2012;21(1):34-44. DOI: 10.1016/j.jclepro.2011.08.021

49.Sannino G, Tartaglia Polcini P, Agliata F, Aversano N. L‘integrated popular reporting come risposta alle esigenze informative degli utenti nelle aziende pubbliche. Rivista Italiana di Ragioneria e di Economia Aziendale (RIREA). 2019;1:29-45

50.Biancone P, Secinaro S, Brescia V, Calandra D. Linee guida per la realizzazione del Bilancio POP o Integrated Popular Financial Reporting. European Journal of Volunteering and Community-Based Projects. 2023;1(4):23-114. DOI: 10.5281/zenodo.10259584

Written By

Francesco Agliata, Danilo Tuccillo, Andrea Rey and Maria Rita Filocamo

Submitted: 28 December 2023Reviewed: 02 February 2024Published: 08 April 2024