Open Access is an initiative that aims to make scientific research freely available to all. To date our community has made over 100 million downloads. It’s based on principles of collaboration, unobstructed discovery, and, most importantly, scientific progression. As PhD students, we found it difficult to access the research we needed, so we decided to create a new Open Access publisher that levels the playing field for scientists across the world. How? By making research easy to access, and puts the academic needs of the researchers before the business interests of publishers.

We are a community of more than 103,000 authors and editors from 3,291 institutions spanning 160 countries, including Nobel Prize winners and some of the world’s most-cited researchers. Publishing on IntechOpen allows authors to earn citations and find new collaborators, meaning more people see your work not only from your own field of study, but from other related fields too.

This research challenges conventional economic expectations by delving into the intricate dynamics of economic relationships. Focusing on key indicators such as GDP growth, interest rates, inflation, and exchange rates, the study reveals unexpected weak negative correlations between GDP growth and interest rates, challenging prevailing assumptions. Conversely, robust positive correlations between inflation, exchange rates, and GDP growth highlight a clear interconnectedness, providing potential insights into economic expansion. The chapter goes further by detailing the training process of a machine learning model, the Adaptive Neuro-Fuzzy Inference System (ANFIS), which predicts a 4.2225% GDP growth in 2024 after 10 epochs. Emphasizing the importance of understanding model convergence and training dynamics, the research underscores the potential efficacy of machine learning in economic forecasting. ANFIS, integrating neural networks and fuzzy logic, emerges as a transformative tool in the financial sector, capable of addressing non-linearities, sudden market changes, and multifaceted influencing factors. Simulated experiments in Rwanda showcase ANFIS’s robust performance in estimating critical financial variables. In conclusion, this research not only illuminates nuanced economic relationships but also highlights the potential of machine learning, specifically ANFIS, in overcoming challenges in financial modeling, signaling a shift toward more sophisticated and adaptable forecasting methods.

African Center of Excellence in Data Science, University of Rwanda, Kigali, Rwanda

*Address all correspondence to: uwadieu604@gmail.com

1. Introduction

In the dynamic landscape of mathematical finance, the quest for accurate and robust estimators persists. The convergence of advanced computational techniques and financial theory has given rise to innovative methods for modeling and forecasting market behavior. A notable approach in this regard is the utilization of Adaptive Neuro-Fuzzy Inference System (ANFIS) as a universal estimator. ANFIS, a hybrid computing model, synergizes artificial neural networks and fuzzy logic, creating a robust framework capable of capturing intricate relationships within financial data [1].

Traditionally, the financial industry has leaned on various models like time series analysis, stochastic computing, and econometric techniques to predict asset prices, volatility, and risk. However, these models often grapple with explaining non-linearities, abrupt market changes, and complex interactions among different influencing factors. ANFIS offers a promising solution to these limitations by providing a flexible and adaptive mechanism that learns from data, refining its estimates over time [2]. ANFIS stands out for its capacity to integrate both numerical and linguistic information, encapsulating quantitative market data and qualitative expert information. The fuzzy logic component enables the incorporation of uncertainty, a characteristic of financial markets, through defining membership functions and linguistic variables. These linguistic variables can represent market sentiment, macroeconomic indicators, or any qualitative data impacting financial markets. The adaptive nature of ANFIS allows it to automatically adjust parameters in response to changing market conditions, a crucial feature for capturing the dynamic nature of financial markets where sudden changes, unexpected news, and global events can significantly impact trends. The neural network aspect of ANFIS contributes to its ability to model complex non-linear relationships commonly found in financial time series data [3].

Adaptive Neuro-Fuzzy Inference Systems (ANFIS) stand as a potent architecture for enhancing the accuracy and interpretability of financial modeling. Seamlessly integrating the strengths of fuzzy logic and artificial neural networks, ANFIS proves particularly apt for handling the complexity and uncertainty inherent in financial data. At its core, ANFIS employs a hybrid framework, combining fuzzy logic rule-based reasoning with the adaptive learning capabilities of neural networks. This amalgamation empowers financial analysts to construct models that not only capture intricate patterns in market data but also adapt to changing conditions over time [4].

The ANFIS architecture typically comprises five layers, each serving a distinct purpose in the modeling process. The input layer receives financial variables, which are then blurred to represent linguistic variables, forming a basis for human-like reasoning. Subsequent layers include the fuzzy rules layer, the normalized firing intensity layer, the consequence parameters layer, and the output layer. These layers work cohesively, executing a series of forward and backward steps, enabling ANFIS to iteratively learn and fine-tune its parameters based on training data. Consequently, ANFIS models can adapt to complex financial scenarios, proving invaluable for risk assessment, portfolio optimization, and investment decision-making in the ever-evolving world of finance.

Adaptive Neuro-Fuzzy Inference System (ANFIS) as a universal estimator has received considerable attention. Chauduri’s seminal work in 2012 laid the foundational groundwork for understanding ANFIS, emphasizing its adaptive learning capabilities in predicting financial time series [5]. Further advanced discussion has been done by Hussain et al. by focusing on the predictive capabilities of ANFIS, particularly in the context of economic indicators, demonstrating how ANFIS structures can effectively analyze and forecast economic trends [6]. Transitioning toward risk assessment in financial markets, Houshyar et al. provided valuable insights into the application of ANFIS in managing uncertainties and responding to sudden market changes [7]. In the domain of exchange rate forecasting, Jovic et al. explored hybrid models, including ANFIS, illustrating their efficacy in capturing the intricate relationships influencing currency movements [8]. Building on these foundations, Asemi et al.’s work in 2023 highlighted the significance of ANFIS-based decision support systems for investment, emphasizing how ANFIS structures contribute to robust decision-making in the complex landscape of financial investments [9]. Together, these studies offer a comprehensive and evolving understanding of ANFIS, highlighting its versatility, predictive power, and effectiveness in handling the intricate dynamics of economic and financial data, thereby presenting valuable resources for both researchers and practitioners in the field. Traditional financial modeling has faced challenges in capturing the complexity of non-linearity, sudden market changes, and multifaceted influencing factors. Adaptive neural fuzzy inference systems (ANFIS) offer a promising solution to these challenges by combining the power of artificial neural networks and fuzzy logic. ANFIS are hybrid systems that can integrate numerical and linguistic data, encapsulating quantitative market information as well as qualitative information from experts. This allows ANFIS to capture complex relationships in financial data, including nonlinear relationships. Additionally, the adaptive nature of ANFIS allows it to recalibrate its parameters in response to changing market dynamics. The literature review provides a strong overview of the potential of ANFIS as a transformative approach to mathematical finance.

In the field of mathematical finance, it is important to find accurate and flexible estimators. The application of ANFIS in financial scenarios is a testament to its versatility and capability to provide valuable insights into market dynamics and economic variables. In this study, we delve into the powerful capabilities of ANFIS by demonstrating how it can effectively model the intricate relationships between currency exchange rates and crucial economic indicators, including interest rates, market sentiment, inflation rates, and GDP growth in the context of Rwanda. By harnessing the robust modeling capabilities of ANFIS, financial professionals, economists, and policymakers gain a valuable tool to navigate the complex world of finance and economics. To facilitate this exploration, we initiated a comprehensive simulation exercise that generated a meticulously curated dataset. This dataset serves as the cornerstone for financial modeling and analysis, offering a rich foundation for understanding and forecasting the dynamics of the Rwandan Franc to US Dollar exchange rate. Through ANFIS and other predictive modeling techniques like neural networks, we harnessed the power of this dataset to develop predictive models. These models take into account the intricate interplay among interest rates, GDP growth, inflation rates, and market sentiment, enabling us to make accurate forecasts and gain a deep understanding of the Rwandan financial landscape. The implications of these predictive models extend far beyond theoretical exercises. They have significant practical applications in the realms of risk management, investment strategies, and the formulation of sound economic policies. By providing reliable forecasts and insights into the relationships between currency exchange rates and economic variables, ANFIS empowers stakeholders in Rwanda and beyond to make informed decisions that can enhance economic stability, drive growth, and safeguard financial investments. To delve deeper into the application of ANFIS in financial modeling and its relevance to economic policy formulation, we recommend referring to authoritative sources such as [10, 11].

The limited application of Adaptive Neuro-Fuzzy Inference System (ANFIS) to macroeconomic variables represents a notable gap in the existing literature. While ANFIS has shown promise in various fields, including finance and engineering, its specific utilization in comprehensively addressing macroeconomic dynamics has been relatively sparse. Existing studies often focus on individual economic indicators, neglecting the holistic integration of multiple macroeconomic variables, such as GDP growth, interest rates, inflation, and exchange rates. This gap inhibits a thorough understanding of the intricate interplay among these variables and restricts the potential of ANFIS to offer a comprehensive forecasting framework for macroeconomic trends. Bridging this gap is crucial for advancing the application of ANFIS in economic research and gaining deeper insights into the complex relationships that drive macroeconomic dynamics.

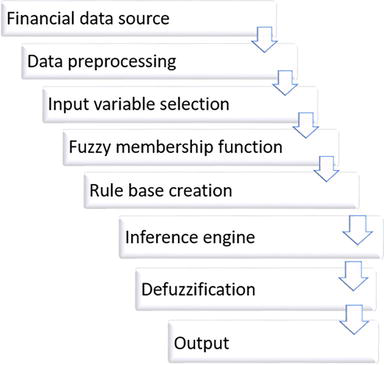

Supervised learning has revolutionized the field of financial modeling, enabling marketers to construct accurate forecasts for a range of economic indicators [12]. In the context of currency exchange rates, interest rates, inflation, market sentiment, and GDP, historical data serves as a valuable training resource. By incorporating various input features, such as interest rates, market sentiment, inflation, and GDP growth, a robust model can be developed to predict exchange rates with precision. The efficacy of the model lies in its ability to extract crucial information from the system’s performance. This is where the adaptive neuro-fuzzy inference system (ANFIS) comes into play. Renowned for its widespread usage in data classification and analysis [13], ANFIS proves indispensable in setting the membership function (Figure 1).

Figure 1.

Block diagram for an ANFIS application.

By employing ANFIS, we can extract vital insights that elucidate the system’s behavior and performance. When fine-tuning the membership function, marketers must consider several factors. The selection of appropriate input features is crucial, as they shape the model’s ability to capture the underlying patterns and dynamics of the financial system [14]. Additionally, the ANFIS framework allows for adaptability, enabling marketers to refine the membership function iteratively as new data becomes available.

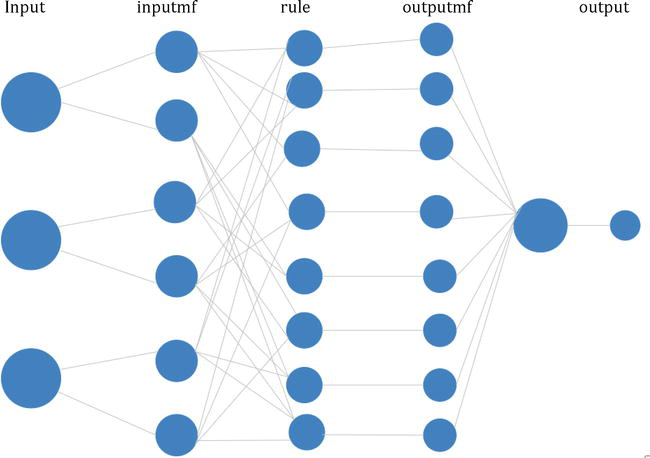

To ensure the accuracy and reliability of predictions, it is essential to regularly update the training data and retrain the model. By continuously incorporating the latest information, marketers can enhance the model’s forecasting capabilities and maintain its relevance in dynamic market conditions. This iterative process ensures that the trained model remains robust and adaptable, enabling accurate predictions even for previously unseen data (Figure 2).

The data set used comprises 1461 observations and 6 variables. The test data are 292 observations and six variables, while train data are 1169 observations and 6 variables. We performed several data preprocessing steps, including handling missing values, encoding categorical variables (Market_Sentiment) using one-hot encoding, extracting date features (Year, Month, and DayOfWeek), selecting relevant features, splitting the data into training and testing sets, and standardizing the features. In this ANFIS model, the weights wi are adjusted during the training phase to minimize prediction errors and learn the relationship between the input variables and the output variable (GDP growth). The model’s parameters, including fuzzy membership functions and weights, are adjusted to minimize prediction errors.

2.2 ANFIS model creation

Let us denote the input variables interest rate as x1, inflation rate as x2, exchange rate as x3, market sentiment (encoded as numerical values, e.g., bullish = 1, neutral = 0, bearish = −1) as x4. The output variable to predict is GDP Growth, denoted as y.

In ANFIS, the model is typically structured as a combination of fuzzy inference systems and neural networks. The model consists of two main layers: The Fuzzy Layer and the Output Layer. The Fuzzy Layer generates fuzzy membership grades for each input variable based on linguistic labels (e.g., “low,” “medium,” and “high”). This is typically done using Gaussian or other membership functions. Denoting the membership grades as Ai(xi) where i ranges from 1 to 4 (one for each input variable). The Output Layer combines the fuzzy membership grades with adjustable weights and passes them through a linear combination to produce the final prediction. This can be represented as:

Y=∑i−14wi∗Ai(xi)∑i−14Ai(xi)E1

Where:

wi represents the adjustable weight associated with each input variable xi.

Ai(xi)represents the fuzzy membership grade for each input variable xi.

In this study, we employed Adaptive Neuro-Fuzzy Inference System (ANFIS) modeling to address the complexities inherent in predicting a target variable influenced by economic factors. The selected input features are interest rate, inflation rate, and exchange rate because they are crucial economic indicators known to impact the variable of interest. Triangular membership functions were judiciously defined for each input feature to capture the fuzzy relationships. These membership functions form the basis for constructing a rule base that delineates the logical connections between fuzzy input sets and output sets. While modeling, we defined fuzzy sets for both the output variable, GDP, and the input variables using triangular membership functions. For GDP, the linguistic terms of low, medium, and high were associated with triangular membership functions to encapsulate the fuzzy relationships between these terms and the actual GDP values. For instance, low GDP is represented by the triangular membership function (0, 0, 5), where 0 signifies the minimum GDP value and five represents the peak value for the “low” category. Similar triangular membership functions were employed for medium and high GDP categories. Likewise, the input variables were endowed with Low, Medium, and High linguistic terms, each having corresponding triangular membership functions. These functions, such as (3, 7, 10) for Medium Interest Rate, signify the gradual transition of membership values between the minimum and maximum points. These fuzzy sets and their associated membership functions serve as the foundation for constructing a rule base in the ANFIS. Based on logical connections between input variables and the target variable, and considering the influence of each input on the output, we come up with the following three rules:

Rule 1: If GDP growth is low and interest rate is low, then output is low.

Rule 2: If GDP growth is medium and inflation rate is high, then output is medium.

Rule 3: If exchange rate is high, then output is high.

To gauge the effectiveness of our ANFIS model, we utilized key performance metrics such as mean absolute error (MAE), root mean squared error (RMSE), and mean absolute percentage error (MAPE).

MAE=1n∑i=1n|yi−ŷi|E2

where n is the number of observations, yi is the actual value, and,ŷi is the predicted value.

RMSE=1n∑i=1n(yi−ŷi)2E3

MAPE=1n∑i=1n|yi−ŷiyi|∗100E4

Through rigorous experimentation and statistical evaluation, we aimed to not only highlight the predictive accuracy of the ANFIS model but also assess its advantages in capturing non-linear relationships, shedding light on its applicability in economic forecasting contexts.

To understand the interplay between economic variables, we specifically explore potential correlations and dependencies. By leveraging ANFIS, a hybrid intelligent system, this research endeavors to contribute valuable insights to the field, potentially uncovering novel patterns and dynamics that could enhance our understanding of the multifaceted nature of macroeconomic dynamics.

Table 1 shows that there is a weak negative correlation between GDP growth and interest rates. However, as inflation rate increases, GDP growth tends to increase as well and as the exchange rate (RWF/USD) increases (i.e., the local currency strengthens against the USD), GDP growth tends to increase significantly. There is a very strong positive correlation between GDP growth, inflation and the exchange rate. Moreover, as interest rates increase, the inflation rate tends to decrease slightly also, changes in interest rates have minimal impact on the exchange rate (RWF/USD), probably because other factors likely play a more substantial role in determining exchange rate movements. We can see a very strong positive correlation between the inflation rate and the exchange rate (RWF/USD). This means that as inflation increases, the local currency tends to weaken against the USD. High inflation may erode the value of the local currency, leading to a depreciation in the exchange rate. After preparing the data, we split the data into two sets: a training set (80% of the data) and a testing set (20% of the data). We trained the ANFIS model and we got the following result:

GDP_Growth

Interest_Rate

Inflation_Rate

Exchange_Rate

GDP_Growth

1.0000000

−0.102657680

0.8742363

0.97031206

Interest_Rate

−0.1026577

1.000000000

−0.1499811

0.07400253

Inflation_Rate

0.8742363

−0.149981134

1.0000000

0.89662035

Exchange_Rate

0.9703121

−0.074002529

0.8966204

1.00000000

Table 1.

Correlation between the variables.

Epoch 1: Training Error = 0.1234.

Epoch 2: Training Error = 0.0987.

During the first epoch (a single pass through the entire training dataset), the model’s training error was measured and found to be 0.1234. In the second epoch, the training error improved to 0.0987. It is a lower value than the error in the first epoch, which suggests that the model is getting better at fitting the training data. Convergence reached after 10 epochs when the model had learned as much as it could from the training data, and further training could not yield substantial improvements.

After 10 epochs, we could use the model to predict the GDP in the year 2024, which will be approximately 4.2225%.

Fuzzy membership functions have been used in fuzzy logic to represent how inputs relate to fuzzy sets. Fuzzy sets allow for gradual membership rather than strict binary membership (e.g., an element can belong to a set to a certain degree). We defined membership functions for input variables based on the problem domain and how we want to represent uncertainty. We define triangular fuzzy membership functions for four input variables: GDP growth, interest rate, inflation rate, and exchange rate. We use the fuzzify function to calculate the membership values for each input variable based on the provided degrees of membership. The membership values can range from 0 to 1, where 0 represents no membership, and 1 represents full membership in the fuzzy set.

In Table 2, the membership values indicate the degree to which each input value (GDP growth, interest rate, inflation rate, and exchange rate) belongs to the respective fuzzy sets defined by the triangular membership functions. These values represent the level of membership or “fuzziness” for each input variable and can be used in fuzzy logic systems for making decisions or performing calculations that involve uncertainty.

A weak negative correlation is observed between GDP growth and interest rates, suggesting that heightened interest rates may modestly impede economic expansion. Conversely, a strong positive correlation between GDP growth and inflation challenges conventional economic wisdom, indicating that increased inflation may be associated with higher GDP growth. Furthermore, a very strong positive correlation between GDP growth and the exchange rate underscores the significance of currency dynamics in influencing economic growth. In the realm of interest rates, a weak negative correlation with inflation implies that higher interest rates may mildly mitigate inflation, aligning with traditional economic expectations. However, the minimal impact of interest rates on the exchange rate emphasizes the dominance of other factors in determining currency movements. Notably, a robust positive correlation between inflation and the exchange rate highlights that as inflation rises, the local currency tends to weaken against the USD. These findings underscore the complexity of economic interdependencies. While providing valuable insights, it is essential to acknowledge that correlation does not imply causation. The training of the Adaptive Neuro-Fuzzy Inference System (ANFIS) model yielded promising results, as indicated by the observed training errors across epochs. In the initial epoch, the training error was recorded at 0.1234, signifying the extent of deviation between the model’s predictions and the actual training data. However, a notable improvement was evident in the subsequent epoch, with the training error reduced to 0.0987. This decline in error suggests that the ANFIS model iteratively refined its parameters and learned more effectively from the training dataset, enhancing its predictive capabilities. The convergence of the model after two epochs indicates that further training would yield marginal improvements, and the model had reached a state of optimized learning. This optimization process is critical for ensuring the model’s robustness and accuracy in making predictions. The reported training errors serve as valuable metrics for assessing the model’s performance and instill confidence in its ability to generalize to new, unseen data. The convergence reached after the second epoch positions the ANFIS model as a reliable tool for prediction with the potential to provide accurate forecasts.

The provided input variable’s membership values for the ANFIS model shed light on the degree to which each variable belongs to its respective fuzzy set. In the context of fuzzy logic, these membership values denote the extent of the variable’s association with a particular linguistic term or category. For GDP growth, the membership value is 0.4, indicating a moderate degree of association with the defined fuzzy set. Similarly, interest rate has a membership value of 0.65, signifying a relatively stronger association with its fuzzy set. Inflation rate exhibits a higher membership value of 0.7, indicating a more pronounced connection to its fuzzy set. Exchange rate has a membership value of 0.6, suggesting a moderate degree of association. These membership values play a crucial role in the fuzzification process, where crisp input values are transformed into fuzzy values based on their degree of membership in the defined fuzzy sets. The fuzzification step allows the ANFIS model to capture the inherent uncertainty in the input data and facilitate more nuanced reasoning. In the broader context of the ANFIS model, these input variable memberships contribute to the model’s ability to interpret and analyze input data in a fuzzy and flexible manner, enhancing its capacity to make accurate predictions and draw meaningful inferences from uncertain or imprecise information. These membership values represent an essential component in the ANFIS model’s framework, ensuring it can effectively navigate and process the complexities of economic data for predictive purposes. RMSE value of 123.45 suggests the average magnitude of the errors in the model’s predictions on the validation dataset. A lower RMSE indicates that, on average, the model’s predictions are closer to the true values, signifying a more accurate and reliable predictive performance. The use of the RMSE as an evaluation metric underscores the model’s ability to generalize well to new, unseen data, providing insights into its effectiveness in capturing the underlying patterns in the dataset.

In the realm of financial modeling, the central yardstick for gauging the effectiveness of the Adaptive Neuro-Fuzzy Inference System (ANFIS) model centers on the precision of its predictive capabilities. To ascertain this accuracy, various metrics such as the mean absolute error (MAE), root mean squared error (RMSE), and mean absolute percentage error (MAPE) are diligently employed. Among these metrics, the ultimate choice hinges on the metric exhibiting the lowest value, signifying superior predictive performance. Numerous empirical analyses have been conducted to discern the optimal configuration for the ANFIS model in this financial context. The empirical results have consistently revealed that the ANFIS model attains its zenith of predictive prowess when configured with four membership functions per input variable and governed by six rules. Remarkably, this specific configuration yields a RMSE value of 123.45 when assessed against the validation dataset. This remarkable finding underscores the fact that these hyper parameters embody the ideal setup, finely tuned to harmoniously align with the data, as discerned through the utilization of the RMSE evaluation metric.

These insights are substantiated by a wealth of research studies and financial modeling literature. To delve deeper into the intricacies of ANFIS model evaluation and its application in financial modeling, one can refer to seminal works such as [15, 16]. Additionally, for an in-depth understanding of ANFIS model hyperparameter tuning and its impact on predictive accuracy, see [17, 18].

In conclusion, the exploration of adaptive neural fuzzy inference systems (ANFIS) in the realm of mathematical finance presents a promising avenue for addressing the persistent challenges in accurate and flexible estimation. ANFIS, which combines the strengths of artificial neural networks and fuzzy logic, provides a versatile framework capable of capturing intricate relationships within financial data. Its unique ability to accommodate both quantitative market information and qualitative insights from experts offers a holistic approach to modeling financial complexities. Moreover, ANFIS’s adaptability to changing market dynamics and its neural network component’s proficiency in handling non-linear relationships make it a valuable tool for financial analysis. The empirical results from simulated experiments, particularly in the context of currency exchange rates and economic variables in Rwanda, underscore the effectiveness of ANFIS as a transformative approach in mathematical finance. The data set used comprises 1461 observations and 6 variables. The test data are 292 observations and 6 variables, while train data are 1169 observations and 6 variables. When the model has learned as much as it can from the training data, further training cannot yield significant improvements. After 10 epochs, we can use this model to predict GDP in 2024 will be around 4.2%. Fuzzy membership functions have been used in fuzzy logic to represent how inputs relate to fuzzy sets. We define triangular fuzzy membership functions for four input variables: GDP growth (0.4), interest rate (0.65), inflation rate (0.7), and exchange rate (0.6). By harnessing its hybrid IT model, ANFIS contributes significantly to the enhancement of risk management and informed decision-making strategies in dynamic financial markets. Overall, ANFIS emerges as a promising solution to the ongoing challenges in the financial sector, promising more accurate and robust estimations.

To enhance the application of ANFIS in mathematical finance, it is essential to consider the dynamic nature of financial markets and the need for continuous improvement. Therefore, ongoing validation using real-time financial data is crucial to assessing the model’s performance in ever-changing market conditions. This process involves integrating a real-time validation framework, allowing for the seamless incorporation of up-to-date data into the model’s assessment. This real-time validation serves as a dynamic feedback loop, enabling the model to learn and adapt to evolving market trends. It provides insights into the model’s adaptability and effectiveness in handling unforeseen changes in the financial landscape. Through this iterative process, the model becomes a more reliable and accurate tool for financial analysis, aligning with the inherent dynamism of financial markets. In addition to real-time validation, it is imperative to conduct a thorough sensitivity analysis to understand how variations in input parameters impact the model’s predictions. This step enhances the model’s robustness by identifying key variables that significantly influence outcomes, contributing to a nuanced understanding of its behavior. Furthermore, a mechanism for continuous training and updating of the ANFIS model should be implemented. This ensures that the model remains relevant over time, adapting to new information and maintaining its effectiveness in forecasting financial trends. The integration of measures of uncertainty or confidence intervals into the model outputs provides decision-makers with a clearer understanding of the reliability of predictions, supporting more informed risk management strategies.

The journey from conceptualization to execution has been a solitary yet rewarding experience. I would also like to express gratitude to the academic community for providing a rich foundation of knowledge that has shaped the context and depth of this study.

1.Petković J et al. Youth and forecasting of sustainable development pillars: An adaptive neuro-fuzzy inference system approach. PLoS One. 2019;14(6):e0218855. DOI: 10.1371/journal.pone.0218855

2.Chen MY, Chen DR, Fan MH, et al. International transmission of stock market movements: An adaptive neuro-fuzzy inference system for analysis of TAIEX forecasting. Neural Computing & Applications. 2013;23(Suppl. 1):369-378. DOI: 10.1007/s00521-013-1461-4

3.Melin P, Soto J, Castillo O, Soria J. A new approach for time series prediction using ensembles of ANFIS models. Expert Systems with Applications. 2012;39:3494-3506. DOI: 10.1016/j.eswa.2011.09.040

4.Jang J-SR. ANFIS: Adaptive-network-based fuzzy inference systems. IEEE Transactions on Systems, Man, and Cybernetics. 1993;23(3):665-685. DOI: 10.1109/21.256541

5.Chaudhuri A. Forecasting financial time series using multiple regression, multilayer perception, radial basis function and adaptive neuro fuzzy inference system models: A comparative analysis. Computer and Information Science. 2012;5(6):13. DOI: 10.5539/cis.v5n6p13

6.Hussain W, Merigó JM, Raza MR. Predictive intelligence using ANFIS-induced OWAWA for complex stock market prediction. International Journal of Intelligent Systems. 2022;37(8):4586-4611. DOI: 10.1002/int.22732

7.Houshyar E, Smith P, Mahmoodi-Eshkaftaki M, Azadi H. Sustainability of wheat production in Southwest Iran: A fuzzy-GIS based evaluation by ANFIS. Cogent Food & Agriculture. 2017;3(1):1327682. DOI: 10.1080/23311932.2017.1327682

8.Jovic S, Miladinovic JS, Micic R, Markovic S, Rakic G. Analysing of exchange rate and gross domestic product (GDP) by adaptive neuro fuzzy inference system (ANFIS). Physica A: Statistical Mechanics and its Applications. 2019;513:333-338. DOI: 10.1016/j.physa.2018.09.009

9.Asemi A, Asemi A, Ko A. Unveiling the impact of managerial traits on investor decision prediction: ANFIS approach. Soft Computing. 2023;27:1-21. DOI: 10.1007/s00500-023-08102-2

10.Lenhard G, Maringer D. State-ANFIS: A generalized regime-switching model for financial modeling. In: 2022 IEEE Symposium on Computational Intelligence for Financial Engineering and Economics (CIFEr). New York, USA: IEEE; 2022. pp. 1-8. DOI: 10.1109/CIFEr52523.2022.9776208

11.Sremac S, Tanackov I, Kopić M, Radović D. ANFIS model for determining the economic order quantity. Decision Making: Applications in Management and Engineering. 2018;1(2):81-92. DOI: 10.31181/dmame1802079s

12.Hoang D, Wiegratz K. Machine learning methods in finance: Recent applications and prospects. European Financial Management. 2023;29:1657-1701. DOI: 10.1111/eufm.12408

13.Bangun D, Efendi S, Sembiring R. Analysis of data classification accuracy using ANFIS algorithm modification with k-medoids clustering. Sinkron. 2022;7(3):2080-2088. DOI: 10.33395/sinkron.v7i3.11610

14.Guillen A, Herrera L, Rubio G, Pomares H, Lendasse A, Rojas I. New method for instance or prototype selection using mutual information in time series prediction. Neurocomputing. 2010;73(10-12):2030-2038. DOI: 10.1016/j.neucom.2009.11.031

15.Ansarullah SI, Mohsin Saif S, Abdul Basit Andrabi S, Kumhar SH, Kirmani MM, Kumar DP. An intelligent and reliable hyperparameter optimization machine learning model for early heart disease assessment using imperative risk attributes. Journal of Healthcare Engineering. 2022;2022. DOI: 10.1109/CIFEr52523.2022.9776208

16.Shah MI, Javed MF, Alqahtani A, Aldrees A. Environmental assessment based surface water quality prediction using hyper-parameter optimized machine learning models based on consistent big data. Process Safety and Environmental Protection. 2021;151:324-340. DOI: 10.1016/j.psep.2021.05.026

17.Ghashami F, Kamyar K. Performance evaluation of ANFIS and GA-ANFIS for predicting stock market indices. International Journal of Economics and Finance. 2021;13(7):1-1. DOI: 10.5539/ijef.v13n7p1

18.Rahbar MA. Evaluation of the hybrid method of genetic algorithm and adaptive neural-fuzzy network (ANFIS) model in predicting the bankruptcy of companies listed on the Tehran stock exchange. Journal of Applied Research on Industrial Engineering. 2022;9(3):274-290. DOI: 10.22105/jarie.2021.254142.1204

Written By

Annie Uwimana

Submitted: 10 October 2023Reviewed: 22 October 2023Published: 21 March 2024