Open Access is an initiative that aims to make scientific research freely available to all. To date our community has made over 100 million downloads. It’s based on principles of collaboration, unobstructed discovery, and, most importantly, scientific progression. As PhD students, we found it difficult to access the research we needed, so we decided to create a new Open Access publisher that levels the playing field for scientists across the world. How? By making research easy to access, and puts the academic needs of the researchers before the business interests of publishers.

We are a community of more than 103,000 authors and editors from 3,291 institutions spanning 160 countries, including Nobel Prize winners and some of the world’s most-cited researchers. Publishing on IntechOpen allows authors to earn citations and find new collaborators, meaning more people see your work not only from your own field of study, but from other related fields too.

This chapter argues that the news media play an important factor in educating the public about financial institutions. It presents some novel survey results, exploring the role of economic news use for the perceived understanding of financial institutions in Germany and the UK. Two web-based surveys were conducted: one in the UK in winter 2018 and one in Germany in summer 2019. Findings show that economic news use is positively related with a better perceived understanding of financial institutions in both countries, even after controlling for demographics and financial socialization. We find that the level of perceived understanding of financial institutions is positively related with education and income and negatively related with being female. The need for information significantly impacted the relationship between economic news use and understanding of financial institutions in the UK but not in Germany. Practical implications for economic and financial news journalists are discussed.

Department of Communication and Media Research, University of Zurich, Zurich, Switzerland

Sophie Knowles

Department of Media, Middlesex University London, UK

Vesile Cinceoglu

Department of Communication and Media Research, University of Zurich, Zurich, Switzerland

*Address all correspondence to: n.strauss@ikmz.uzh.ch

1. Introduction

The way the global economy collapsed during the Global Financial Crisis (GFC) 2008, and the recession that ensued afterwards, highlighted the centrality of financial markets and financial institutions for society and democracy more generally. Now, after a pandemic, the economy is marked by global rising inflation [1], growing inequality [2], a cost-of-living crisis [3], and a new focus on sustainable economic growth [4], which emphasizes the importance of understanding the role financial institutions play in society. At the same time, the 21st century has been characterized by a tremendous increase in complexity of the financial markets [5, 6]. Citizens are confronted with a financial system that is increasingly disconnected from the real-world economy [6, 7], while everyday life has become more and more financialized [8]. In addition, global financial and corporate scandals such as the Pandora Papers, or the insolvency of Wirecard in Germany in 2020 [9]—which have all been widely covered in the international financial press—have questioned the authority, functionality, and honesty of financial institutions worldwide.

Following communication scholars [10, 11, 12], we argue that the news media play a crucial role in informing citizens about economic issues, actors, and institutions. However, research on economic news and its relevance for economic understanding, attitudes, or behavior is lacking (e.g., [13, 14, 15, 16]). Although there is a body of research in finance and economics that has investigated the influencing factors of financial literacy (e.g., [17, 18]) and, among others, media use [19, 20, 21, 22], a theoretical and empirical discussion of the role of financial news use for the understanding of financial institutions has been underrepresented in academic research so far (see for an exception: [20] on monetary knowledge). What is more, numerous studies have consistently and repeatedly shown that financial literacy and financial understanding are unequally spread among the public and in various parts of the world [23], being particularly low among women, younger cohorts, and the less educated public [17, 18]. It has therefore become paramount that we investigate how the news media and economic news use can contribute to a better understanding of financial institutions. In this cross-national survey study, we therefore investigate how economic news use and additional influencing factors are related to the understanding of financial institutions in two Western democracies–Germany and the UK.

2.1 Financial literacy, sociodemographic differences, and personal finance management

Most research about financial knowledge refers to financial literacy, which is generally understood as “a combination of awareness, knowledge, skill, attitude and behaviour necessary to make sound financial decisions and ultimately achieve individual financial well-being” ([24], p. 14). Financial literacy is presented by some authors as the gateway to become an active member of the financial markets (e.g., [25]), to make informed financial decisions [26], to manage retirement planning (e.g., [27]), or to be aware of personal debt levels [28]. However, a worldwide survey by Standard and Poor in 2015 has shown that only 33% of adults worldwide are financially literate [29]. Similarly, academic research has repeatedly provided evidence that financial literacy rates are unequally low in different parts of the world [23] and that people also have difficulties in processing and understanding financial information to various degrees [26, 30].

However, financial understanding is not just about knowing how inflation works, how compound interests play out, or how to invest efficiently and safely (cf. financial literacy: [17, 23]). Instead, financial understanding also expands to the knowledge of the functions and roles of various financial institutions within a democracy. Having a good grasp and understanding of the roles and functions of financial institutions in the countries where citizens live is important to cultivate a knowledgeable and critical citizenry that can make decisions and behave in a way that will benefit their individual economic and social well-being. For example, a recent survey by the European Central Bank (ECB) has shown that there is a positive correlation between people who have a better understanding of the ECB’s task and their trust in the institution [31]. Previous research has indeed shown that increased economic knowledge leads to public policy support and institutional trust in the ECB (e.g., [32, 33]) or the European Monetary Union (e.g., [34]).

Looking at past research that has shown that citizens are not very well informed about real economic conditions [35], it becomes clear that the level of economic and financial understanding has not changed much over time (e.g., US: [36]). To identify the reasons for these low levels of financial understandings, a plethora of research has investigated the influencing factors of financial literacy, albeit most of such studies focus on demographic characteristics, such as age, gender, ethnicity, education, marital status, or income (e.g., [18, 37, 38]). For example, women and less-educated individuals have been found to score lower on financial literacy than men or highly educated individuals [17, 18]. Referring to ethnicity, Sabri et al. [39] showed that the Chinese student minority within a Malaysian student sample had a lower level of financial literacy. Furthermore, Lusardi and Mitchell [23] showed that there was a U-shape when it comes to age and financial literacy, where the youngest and oldest groups scored lower when compared to middle-aged people. Similarly, Bianchi [37] showed that financial literacy was positively correlated with income, wealth, and education but negatively with being married and female. Hence, based on previous findings on financial literacy and demographic factors, we hypothesize:

H1: Perceived understanding of financial institutions is higher for (a) older, (b) male, (c) higher-earning, (d) highly educated citizens and for those (e) belonging to the ethnic majority.

Previous research has repeatedly confirmed that there is a gender gap when it comes to financial literacy or economic knowledge (e.g., [17, 18, 20]). However, rather than presenting this discrepancy as a gender issue, scholars believe that males and females are socialized in distinct ways that make economic topics more or less relevant to them [38]. For example, a study of US introductory economic textbooks has shown that 90% of the examples of economists, policy makers, or business leaders are male [40]. In fact, research on financial literacy has also identified environmental and social factors to be related to financial literacy. For example, Kovarova-Simecek and Aubram [41] showed that among a small sample in Austria, the preferred source of financial information are family, friends, and colleagues. Furthermore, Kim et al. [42] have shown that the parental and social environment in which young adults grow up can influence their financial behavior. In other words, the way parents teach their children or raise awareness on how to deal with money and financial matters can have a positive impact on adults’ financial behavior later in life. Indeed, Loibl and Hira [43] found a medium bivariate positive and significant correlation (r = 0.24) between financial management practices and self-directed financial learning. For this reason, we also want to test whether the ability for personal finance management works as an antecedent to the understanding of financial institutions, in both Germany and the UK. The second hypothesis therefore reads:

H2: A better awareness of personal finance management is related to a better understanding of the role and functions of financial institutions.

2.2 Economic news use and financial understanding

Few scholars in communication science have researched the role of economic news for financial knowledge or understanding. Kalogeropoulos et al. [44] are among the few that have analyzed how the consumption of economic news affects economic sophistication in Denmark. Usually, this stream of research can be situated within the economics, finance, or business discipline (e.g., [20, 22]). Yet, only a small number of scholars in these research fields consider news use as one of the main influencing variables for economic knowledge and rather treat news use as a third variable (e.g., [19]). Moreover, economic news use is sometimes not measured in an adequate way and leaves room for measurement error. For example, Kalogeropoulos et al. [44] measured economic news use as a combination of a general media exposure measure and the results of a content analysis of economic news in Danish news (cf. economic consequence frame).

Based on findings of political news and its influence on political knowledge (e.g., [45, 46, 47, 48, 49]), scholars agree that the news media (e.g., television, newspaper, radio, the Internet) play a crucial role in mediating financial information to the public (e.g., [21, 50]). Interestingly, the argument that individuals might use the news media to get an idea of the current economic situation or economic forecasts was put forward already, around thirty years ago [51]. In fact, survey findings indicate that the news media are a preferred source to learn about money management (e.g., [52]), and more lately, research has shown that seeking financial information on social media or online can lead to greater levels of financial literacy [53] or increased financial satisfaction [43, 54]. For example, a study among South Korean youth found that use of media for financial information was strongly and positively related to financial literacy [22].

There is also some indication that economic news use could potentially close the financial knowledge gap between high- and low-income earners, as low-income consumers prefer to learn about the economy via media sources [55]. However, the picture is varied and can depend on external events and the national context. A recent study using cognitive mapping has shown that while general news consumption is connected to a lower complex understanding of the Global Financial Crisis 2007–2009 (GFC) among Dutch citizens, news uses specifically dealing with the GFC are related to higher cognitive complexity when making sense about the GFC but only among the less-educated citizens [46]. Conversely, another study conducted in the Netherlands implies that more news consumption is not necessarily correlated with a better understanding of economic indicators, such as inflation [56]. However, it should be noted here that reading popular newspapers does not guarantee that one comes across or actively consumes economic information. Economic news consumption itself can be influenced by additional external factors. For example, Knowles and Schifferes [21] showed that business and economic news have been used more intensively by UK citizens in 2011 (after GFC) when compared to 2005.

Some recent research investigating the link between economic news use and financial literacy indicates that there might indeed be a correlation. For example, Kovarova-Simecek and Aubram [41] have presented initial results from a convenience sample in Austria that show that there is a positive relationship between the use of financial magazines, the Internet, and newspapers and financial literacy. In addition, van Rooij et al. [25] showed that individuals who scored higher on financial literacy mostly relied on formal sources such as newspapers, financial advisors, and the Internet. More recently, Hayo and Neuenkirch [20] have shown that the use of various media channels (e.g., newspapers, TV) for information about the ECB is positively related with subjective and objective knowledge about the ECB. Thus, following the argumentation above and the findings from previous research, we presume:

H3: The more citizens consume economic news, the higher their perceived understanding of the role and functions of financial institutions.

2.3 The moderating effect of need for economic news

We know from previous research that cognitive elaboration, or the need to be informed, is a crucial factor for the positive effect of news on political behavioral or attitudinal variables [48]. However, only recently, research on financial literacy and economic knowledge has been considering further influencing variables, such as interest in a topic [19, 57] or personal involvement [50]. Sohn et al. [22] argue that using the news media for economic information requires a conscious and active information-seeking behavior, hence implying an intrinsic interest in economic topics. Based on their results, they contended that “gaining financial literacy through media sources is indicative of a young person’s active effort to seek personal finance information” ([22], 977).

Equally, Hayo and Neuenkirch [20] have shown that the desire to be informed about the ECB is significantly and positively related to information search and knowledge about the ECB. Similar findings have been reported by van der Cruijsen et al. [57] who found that Dutch respondents with a strong desire to be informed about the ECB and who use various media sources more frequently are more knowledgeable about the ECB. Following these findings, the effect of economic news use on the understanding of financial institutions might be moderated by the conscious and cognitive need to obtain financial information from the media. We thus presume:

H4: The relationship between economic news on perceived understanding of the role and functions of financial institutions is moderated by the need to stay informed about the economy such that the relationship is stronger for those with a higher need to stay informed about the economy.

2.4 Germany and the UK: Two cases in Western democracies

Germany is known as one of the strongest economies in the world, based on nominal GDP [58]. Compared to other countries, financial literacy is moderately high (66%), according to the Standard & Poor’s report [29]. However, Hayo and Neuenkirch [20] report that both subjective and objective knowledge about monetary policy and the ECB is rather low among Germans and that they generally have a low interest in these topics. Studying perceived understanding of financial institutions among German citizens is particularly interesting, as Germany has not only faced its biggest post-war fraud scandal with Wirecard in 2020 [59], but it was also one of the European countries that was affected the most by a tax fraud scheme, called “cum-ex” or “cum-cum,” that deprived the German state’s tax offices of €31.8 billion in total [60].

According to the Standard & Poor’s Report mentioned above, financial literacy in the UK is in a similar region to Germany (67%) [29]. Nonetheless, financial literacy remains weak across a wide swathe of the UK public, particularly among women and low-income groups [21]. According to a survey conducted at the height of the pandemic [30], more than half of the UK survey respondents were not sure what GDP meant, and nearly half were not sure they understood government borrowing. People were most confident at understanding unemployment, but one-third were not sure about either interest rates or inflation. The lack of financial literacy makes it harder to ensure that all sections of the community can engage in an economic debate. Although the two countries show similarities in terms of citizens’ financial literacy, the two countries differ regarding their media systems. While Germany can be situated within the corporatist model with a high newspaper circulation, strong state intervention in the media system, and institutionalized self-regulation, the UK has the characteristics of a liberal media system, being market dominated and having no institutionalized self-regulation [61]. Therefore, we are interested in the following:

RQ1: What are the differences between Germany and the UK regarding the influence of economic news use on the understanding of financial institutions in both countries?

To find answers to the research questions and hypotheses, two online surveys were conducted in Germany in June 2019 and the UK in December 2018, with a panel of respondents provided by Qualtrics. The survey has been approved by the Ethics Committee of the MDX Faculty of Arts and Creative Industries at Middlesex University London, and respondents were provided with an appropriate informed consent on the first page of the online survey. In total, 233 people in Germany and 284 people in the UK were recruited through Qualtrics that resembled the national population of German and UK citizens based on a range of socio-demographic variables, including age and gender. The sample in Germany was balanced with 50.6% male and 49.4% female participants, being on average between 35 and 44 years old (M = 3.35/SD = 1.50), earning on average between €20,000 and €29,999 and €30,000 and €49,999 (M = 2.89/SD = 1.65), and having an average education level of Abitur (M = 3.00/SD = 1.80). The UK sample had slightly more female participants (45.4% male; 54.6% female), an average age between 35 and 44 years (M = 3.36/SD = 1.56), an average income between £20,000 and £29,999, and an average education level at the A level (M = 3.06/SD = 1.96). Only regarding the variable ethnicity, both samples are characterized by an over-representation of white participants (Germany: 93.6% white, 6.4% non-white; UK: 91.9% white, 8.1% non-white). The measurements of all key variables per country are described below in detail (see the descriptive of all key variables in Table 1).

Variables

Germany

UK

M

SD

M

SD

Perceived understanding of financial institutions

2.67

0.69

2.61

0.62

Personal finance management

2.34

0.45

3.43

0.53

Economic news use

3.27

0.84

3.10

1.02

Need for economic information

2.24

0.75

2.31

0.73

Table 1.

Descriptive for key variables in the German and UK sample.

3.2 Measurements

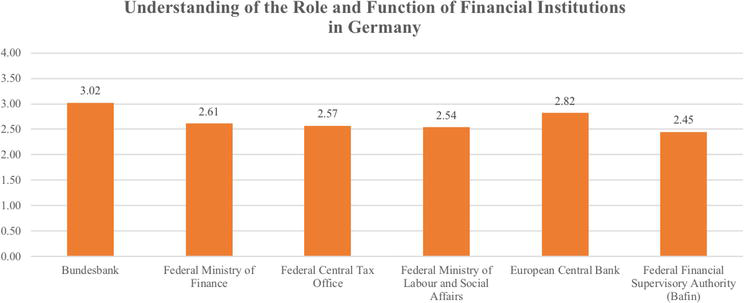

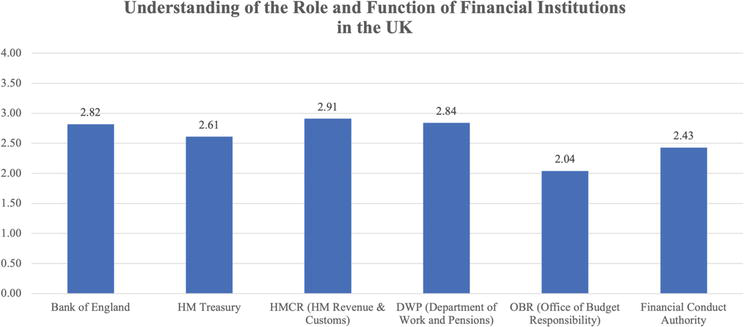

Perceived understanding of financial institutions was measured by asking “How well do you understand the role and function of the following institutions” (1 = never heard of them; 4 = very well) for six various financial institutions in the respective country (Germany: α = 0.92; UK: α = 0.87). For the UK, these were (a) Bank of England, (b) HM Treasury, (c) HMRC (Inland Revenue), (d) DWP (Department of Work and Pensions), (e) OBR (Office of Budget Responsibility), and (e) FCA (Financial Conduct Authority). For Germany, these were (a) Bundesbank, (b) Federal Ministry of Finance, (c) Federal Central Tax Office, (d) The Federal Ministry of Labour and Social Affairs, (e) European Central Bank, and (f) Federal Financial Supervisory Authority (Bafin). Following previous research on the understanding of monetary policy [20] and consumer research that consciously distinguishes between objective and subjective knowledge [62], we chose “perceived” understanding because it’s indicative for individuals’ decision-making processes. See the means of the understanding of the various financial institutions in Germany and the UK in Figures 1 and 2.

Figure 1.

Means for perceived understanding of the role and function of various financial institutions in Germany.

Figure 2.

Means for perceived understanding of the role and function of various financial institutions in the UK.

To measure to what extent citizens were aware and knowledgeable about how to manage their personal finances, we used a common measurement for personal finance management [63], consisting of four questions: “Thinking overall about your, and your partner/spouse’s finances, how important, if at all, do you think it is to…” (1 = not important; 4 = very important) (1) save money for a rainy day, (2) put aside money for your retirement, (3) keep track of income and expenditure, and (4) shop around in order to make your money go further (reversed). However, due to a low reliability score, we dropped the fourth, reversed question (as proposed by the R-function alpha), which yielded a satisfactory reliability score (Germany: α = 0.65; UK: α = 0.67).

Economic news use was inquired by posing three questions: (1) “To what extent do you AGREE or DISAGREE with the following statement? ‘I regularly read the financial pages in the papers or online’” (1 = disagree; 4 = agree); (2) “Thinking more generally, how closely have you been following the news about the state of the economy and its future prospects?” (1 = not at all closely; 4 = very closely); and (3) “How frequently do you follow the news about business and the economy?” (1 = I do not follow this type of news, 2 = less than once a month, 3 = once a month, 4 = once a week, 5 = several times a week, 6 = every day). Although we used different wordings and answer scales for this measurement, the reliability score is sufficient (Germany: α = 0.75; UK: α = 0.77).

The moderator need for economic information was measured by asking a single question: “In your opinion, how important is it for people like you to keep up-to-date with what’s happening in financial matters generally such as the economy and your personal finances?” (0 = do not know/no opinion; 1 = not at all important; 3 = very important). The covariate matrix of all key variables for both countries are shown in Tables 2 and 3.

Zero-order correlations among all key variables in the UK sample.

p < 0.01.

p < 0.001.

3.3 Analysis

To test the hypotheses, we conducted hierarchical regression analysis with listwise deletion in five steps for the German and the UK sample, respectively. In the first block, we only included the sociodemographic variables to predict understanding of financial institutions and test H1. In the second, we added personal finance management to test H2. In the third block, we included economic news use to test H3. In the fourth step, we added need for economic news. To test the moderation effect (H4), we included the interaction effect in the next step. We have checked the regression analysis (excluding the moderation) for robustness and found no indicators that would cause concern for a non-normal, skewed model (e.g., VIF, Cook’s distance, Durbin Watson Test).

The results (Table 4) show that H1 is partly supported for both countries. In all five models for the German sample, we find that men (b) and highly educated (c) and higher earning citizens (d) have a significantly better perceived understanding of financial institutions. Regarding age (a) or ethnicity (e), we do not find any significant relationship. For the UK sample (Table 5), only gender seems to be negatively associated with the outcome variable, as the data show that women have less understanding of financial institutions than men, but this relationship vanishes once the models include economic news use, need for economic information, and the interaction effect. Regarding H2, we find partial support in both the German and the UK sample. For Germany, the relationship only holds in Model 2. For the UK sample, there is a positive, significant relationship between better awareness of personal finance management and the perceived understanding of the role and function of financial institutions, even when including economic news use (Model 3) but not in Model 4–5.

Perceived understanding of the role and functions of financial institutions

Hierarchical regression analyses predicting the perceived understanding of the role and functions of financial institutions—German sample.

p < 0.05.

p < 0.01.

p < 0.001.

Notes: Cell entries are final-entry ordinary least squares (OLS) and standardized Beta (β) coefficients; standard errors in parentheses; n = 217 (after listwise deletion); bolded results are within normal confidence intervals based on 5000 bootstraps.

Perceived understanding of the role and functions of financial institutions

Hierarchical regression analyses predicting the perceived understanding of the role and functions of financial institutions—UK sample.

p < 0.05.

p < 0.01.

p < 0.001.

Note: Cell entries are final-entry ordinary least squares (OLS) and standardized Beta (β) coefficients; standard errors in parentheses; n = 260 (after listwise deletion); bolded results are within normal confidence intervals based on 5000 bootstraps.

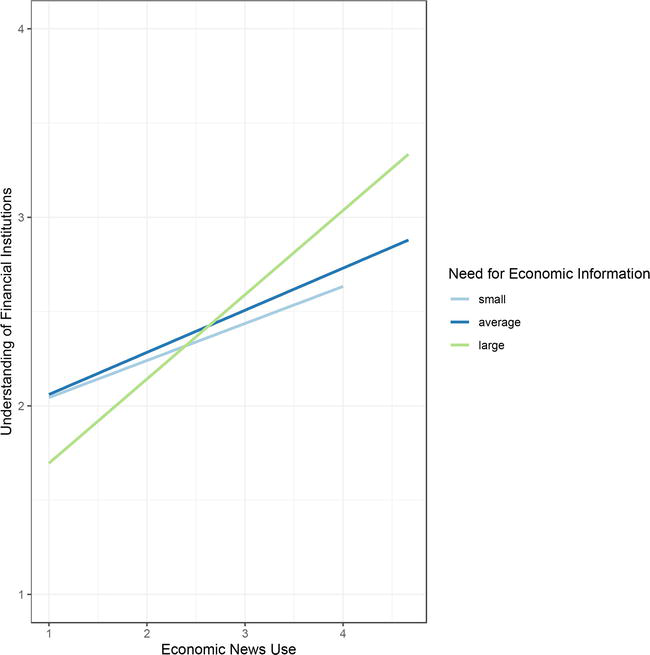

H3 is largely supported in both samples, meaning that the more German and UK citizens consume economic news, the higher their perceived understanding of financial institutions. However, these significant positive relationships disappear once the interaction effects are added to the respective regression models. In the fifth models of the hierarchical regression analyses, we find support for H4 in the UK sample but not in the German sample. Hence, the relationship between economic news use and perceived understanding of financial institutions is significantly and positively moderated by the need for economic information among UK citizens. The plot of the interaction effect (see Figure 3), furthermore, shows that citizens with high levels of economic news use and those with a higher need to stay informed about economic news have a better understanding of financial institutions.

Figure 3.

Conditional plot for interaction effect of economic news use and need for economic information on the perceived understanding of the role and function of financial institutions in the UK sample.

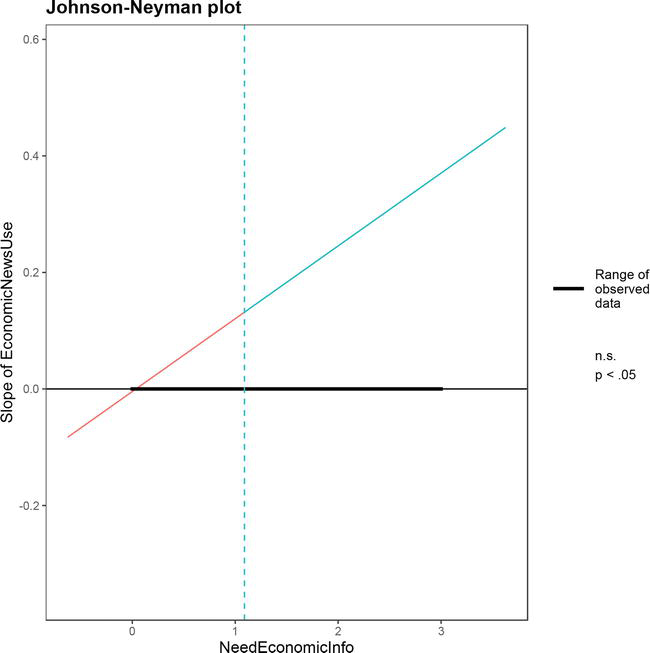

By means of the Johnson-Neyman technique, we show at what levels this moderation effect stays significant for the UK sample. Figure 4 shows that already by scoring higher than one on the question regarding the need for economic information, the slope of economic news use becomes positive and significant. Reversely, economic news has no effect on the understanding of financial institutions if the need for economic information is lower than 1.1. We also tested all the regression results and moderation effects for robustness. Bootstrapping results indicate, however, that not all findings are representative of the entire population of German and UK citizens, probably due to the small sample size. The robust coefficients are bolded in Tables 4 and 5. Hence, generalizations for the German and UK populations need to be considered with caution.

Figure 4.

Johnson-Neyman plot, showing where the conditional slope of economic news use significantly differs from zero.

Understanding the function and role of financial institutions plays a crucial role for a well-functioning democracy. As we argue, only by keeping themselves well-informed about economic topics and institutions, citizens can develop a sound understanding and a critical perspective about the financial system. This enables them to cast deliberative votes and become engaged for a more transparent, just, and sustainable financial system. Scholars in economics, finance, as well as communication science have argued that the news media provide relevant information that contributes to and fosters financial literacy and knowledge [20, 21, 41]. However, only few researchers (e.g., [20]) have also looked at how economic news use can contribute to a better understanding of financial institutions.

In this study, we sought to study how economic news use is related to the perceived understanding of the role and function of financial institutions in Germany and the UK. Our survey results provide clear evidence that there is a significant relationship between economic news use and understanding of financial institutions in both countries. What is more, this study has corroborated previous research on financial literacy [17, 23], showing that the perceived understanding of financial institutions is positively related with education and income and negatively related with being female. However, these findings were more robust and present in the German sample. Similarly, financial socialization or, in other words, the awareness for managing one’s personal finances was not a steady influencing factor for the perceived understanding of financial institutions.

Another interesting result of this study was the moderation effect found in the UK sample. Here, it was revealed that the relationship between economic news use and the understanding of financial institutions is stronger for those people who have a higher need to stay informed about the economy. This result does not only support findings on ECB information seeking and knowledge about the ECB [33, 57], it is also in line with findings from political communication where the need for (political) information has repeatedly been shown to play a crucial role in learning from information consumed via the news media (e.g., [47, 48, 49]). Hence, rather than providing information in school programs on financial education, teachers should prioritize media literacy and encourage students’ curiosity and engagement with financial and economic topics so that they understand the importance of finance in their daily lives. In fact, previous research suggests that merely providing financial information to adolescents is not sufficient to increase financial literacy [18]. Instead, training and workshops should have an attitudinal and practical component to enhance experiential learning that will ultimately lead to better results in financial literacy.

Furthermore, in line with the differences of the media systems in the UK and Germany [61], the findings highlight that the relationship between economic news use and the perceived understanding of financial institutions seems to be higher in the liberal media system in the UK, while in the democratic corporatist model in Germany, sociodemographic data matter more in explaining the understanding of financial institutions in the respective country. It could be possible that the medium newspaper circulation in the liberal model in the UK could be more decisive in explaining the outcome knowledge variable, compared to the democratic corporatist model where newspaper circulation is generally high. What is more, the market-dominated media market in the UK as well as the strong presence of the flagship financial newspaper Financial Times in the country might carry more weight in explaining why the relationship between reading economic news and scoring higher on the perceived understanding of financial institutions is stronger for UK citizens than for German citizens—and this despite the fact that the mean value of economic news use was higher in Germany when compared to the UK.

For financial journalism practice, the findings of this study imply several things. First, news media outlets should become more aware of the significance of financial and economic news for their audience. Although the economic news beat is a niche in general news reporting, receiving only limited attention from its audience [64], the findings in this study have shown that economic news use plays an important role in contributing to the perceived understanding of citizens about financial institutions. Second, based on the results from this study, financial journalists should feel more engaged and motivated to make their coverage more attractive to the general audience, especially for women and those on low incomes. For example, a survey study by Knowles and Schifferes [21] revealed that citizens in the UK thought that the financial media should explain economic events in a clearer and easier language and that they should describe better how economic developments affect them as citizens personally. Following the relationships identified in this study, journalists have evidence that their work matters in educating the public on financial topics and institutions. Thus, by making economic news more attractive (e.g., choice of topics or presentation mode), financial journalists have the potential to activate, educate, and engage a broader and more critical audience for economic issues.

Although the regression models were found to be largely robust and most of the results were representative of the population, the study does not come without limitations. First, it would be worthwhile to repeat the survey among a larger representative sample in both countries, given that the bootstrapping results revealed that some estimates were out of the confidence interval bounds. In fact, the survey samples had an over-representation of white respondents in both countries, compared to the national censuses. In addition, some of the measurements should be further developed, added, and improved. For example, the “need for economic information” should not be measured by a single item, and financial socialization could be measured by additional questions [41, 42]. Furthermore, the answer scales of the survey questions should be kept similar across the measurements (cf. economic news use) in future research. In addition, previous research has shown that asking for perceived or subjective knowledge can sometimes lead to overestimations. Hayo and Neuenkirch [20], for example, report that “particularly disinterested men tend to overestimate their own monetary policy knowledge” (p. 19). Hence, rather than only asking for perceived knowledge, objective knowledge questions for the understanding of financial institutions should be composed in a follow-up study.

Despite these shortcomings, this cross-national survey study has provided useful and first-time insights into the influencing variables of the perceived understanding of financial institutions in Germany and the UK. By working out the pivotal role of economic news use consumption, this study has not only shown that the news media should be attributed more relevance in financial education programs, but the study has also formulated directive implications for financial journalism and practice. To sum up, economic journalists need to take a range of socio-demographic factors into account when they write for a broad audience, so that those from lower incomes, who have less education, women, and those with a lower need to stay informed about the economy are not left out of important discussions.

The authors report there are no competing interests to declare.

The data set associated with the paper can be requested from the corresponding author.

References

1.Romei V, Smith A. Global inflation tracker: See how your country compares on rising prices. Financial Times. 2023. Available from: https://www.ft.com/content/088d3368-bb8b-4ff3-9df7-a7680d4d81b2

2.Chancel L. World Inequality Report 2022. Wid World. 2022. Available from: https://wir2022.wid.world/www-site/uploads/2022/01/Summary_WorldInequalityReport2022_English.pdf

3.Christian A. How the cost-of-living crisis is fuelling job quits. BBC. 2023. Available from: https://www.bbc.com/worklife/article/20230713-how-the-cost-of-living-crisis-is-fuelling-jobquits

4.Stern LN, Lankes HP, Pierfederici R. These are the 4 steps we need to make economic growth sustainable, resilient and inclusive. WEF. 2022. Available from: https://www.weforum.org/agenda/2022/07/sustainable-resilient-inclusive-economic-growth/

5.Kyrtsou C, Sornette D, Adcock C. New Facets of Economic Complexity in Modern Financial Markets. New York: Routledge; 2019

6.Raworth K. Doughnut Economics. Seven Ways to Think like a 21st-Century Economist. London: Penguin Random House; 2017

7.Mazzucato M. The Value of Everything. Making and Taking in the Global Economy. London: Penguin Random House; 2019

8.Epstein GA. Financialization and the World Economy. Cheltenham: Edward Elgar Publishing; 2005

9.Storbeck O. Wirecard: A record of deception, disarray and mismanagement. Financial Times. 2021. Available from: https://www.ft.com/content/15bb36e7-54dc-463a-a6d5-70fc38a11c81

10.Ferree MM, Gamson WA, Gerhards J, Rucht D. Four models of the public sphere in modern democracies. Theory and Society. 2002;31(3):289-324

11.Gans HJ. Democracy and the News. New York: Oxford University Press; 2003

12.Strömbäck J. In search of a standard: Four models of democracy and their normative implications for journalism. Journalism Studies. 2005;6(3):331-345

13.Davis A. Media effects and the active elite audience: A study of communications in the London stock exchange. European Journal of Communication. 2005;20(3):303-326

14.Greenfield C, Williams P. Financialization, finance rationality and the role of media in Australia. Media, Culture & Society. 2007;29(3):415-433

15.Lee M. A review of communication scholarship on the financial markets and the financial media. International Journal of Communication. 2014;8:715-736

16.Thompson PA. Invested interests? Reflexivity, representation and reporting in financial markets. Journalism. 2013;14(2):208-227

17.Lusardi A, Mitchelli OS. Planning and financial literacy: How do women fare? American Economic Review. 2008;98(2):413-417

18.Lusardi A, Mitchell OS, Curto V. Financial literacy among the young. Journal of Consumer Affairs. 2010;44(2):358-380

19.Förster M, Happ R. The relationship among gender, interest in economic topics, media use, and the economic knowledge of students at vocational schools. Citizenship, Social and Economics Education. 2019;18(3):143-157

20.Hayo B, Neuenkirch E. The influence of media use on layperson monetary policy knowledge in Germany. Scottish Journal of Political Economy. 2018;65(1):1-26

21.Knowles S, Schifferes S. Financial capability, the financial crisis and trust in news media. Journal of Applied Journalism & Media Studies. 2020;9(1):61-83

22.Sohn S-H, Joo S-H, Grable JE, Lee S, Kim M. Adolescents’ financial literacy: The role of financial socialization agents, financial experiences, and money attitudes in shaping financial literacy among South Korean youth. Journal of Adolescence. 2012;35(4):969-980

23.Lusardi A, Mitchelli OS. Financial literacy around the world: An overview. Journal of Pension Economics & Finance. 2011;10(4):497-508

24.Atkinson A, Messy F-A. Measuring financial literacy: Results of the OECD/international network on financial education (INFE) pilot study. OECD Working Papers on Finance, Insurance and Private Pensions. 2012;15:1-73

25.Rooij V, Maarten CJ, Lusardi A, Alessie RJM. Financial literacy, retirement planning and household wealth. The Economic Journal. 2012;122(560):449-478

26.Lusardi A, Mitchelli OS. Financial literacy and retirement preparedness: Evidence and implications for financial education. Business Economics. 2007;42(1):35-44

27.Clark RL, Morrill MS, Allen SG. The role of financial literacy in determining retirement plans. Economic Inquiry. 2012;50(4):851-866

28.Lusardi A, Tufano P. Debt literacy, financial experiences, and overindebtedness. Journal of Pension Economics & Finance. 2015;14(4):332-368

29.Klapper L, Lusardi A, Oudheusden V. Financial Literacy around the World: Insights from the Standard & Poor’s Ratings Services Global Financial Literacy Survey. GFLEC (Global Financial Literacy Excellence Center); 2015. Available from: https://gflec.org/initiatives/sp-global-finlit-survey/

30.Schifferes S, Knowles S. Covid-19, inequality and the media. In: Schifferes S, Knowles S, editors. The Media and Inequality. London: Routledge; 2022. pp. 211-225

31.Schnabel I. Societal responsibility and central bank independence. European Central Bank. Eurosystem. 2021. Available from: https://www.ecb.europa.eu/press/key/date/2021/html/ecb.sp210527_1~ae50e2be97.en.html

32.Ehrmann M, Soudan M, Stracca L. Explaining European Union citizens’ trust in the European Central Bank in normal and crisis times. The Scandinavian Journal of Economics. 2013;115(3):781-807

33.Hayo B, Neuenkirch E. The German public and its trust in the ECB: The role of knowledge and information search. Journal of International Money and Finance. 2014;47:286-303

34.Hayo B. Knowledge and attitude towards European monetary union. Journal of Policy Modeling. 1999;21(5):641-651

35.Ranyard R, Missier D, Fabio B, Nicolao D, Summers B. Perceptions and expectations of price changes and inflation: A review and conceptual framework. Journal of Economic Psychology. 2008;29(4):378-400

36.Lusardi A. Financial literacy and the need for financial education: Evidence and implications. Swiss Journal of Economics and Statistics. 2019;155(1):1-8

37.Bianchi M. Financial literacy and portfolio dynamics. The Journal of Finance. 2018;73(2):831-859

38.Driva A, Lührmann M, Winter J. Gender differences and stereotypes in financial literacy: Off to an early start. Economics Letters. 2016;146:143-146

39.Sabri MF, Cook CC, Gudmunson CG. Financial well-being of Malaysian college students. Asian Education and Development Studies. 2012;1(2):153-170

40.Stevenson B, Zlotnik H. Representations of men and women in introductory economics textbooks. AEA Papers and Proceedings. 2018;108:180-185

41.Kovarova-Simecek M, Aubram T. 'Financial literacy, information behavior, and interest in financial news in Austria', social science research. Network. 2018;2018:1-34

42.Kim J, Chatterjee S, Kim J. Outstanding AFCPE® conference paper: Debt burden of young adults in the United States. Journal of Financial Counseling and Planning. 2012;23(2):5-67

43.Loibl C, Hira TK. Self-directed financial learning and financial satisfaction. Journal of Financial Counseling and Planning. 2005;16(1):11-21

44.Kalogeropoulos, Antonios, Albæk, Erik, de Vreese, Claes H., Van Dalen, Arjen (2015), 'The predictors of economic sophistication: Media, interpersonal communication and negative economic experiences', European Journal of Communication 30(4): 385-403.

45.Beckers K, Aelst V, Peter V, d’Haenens L. What do people learn from following the news? A diary study on the influence of media use on knowledge of current news stories. European Journal of Communication. 2021;36(3):254-269

46.Boukes M, van Esch FAWJ, Snellens JA, Steenman SC, Vliegenthart R. Using cognitive mapping to study the relationship between news exposure and cognitive complexity. Public Opinion Quarterly. 2020;84(3):599-628

47.Boulianne S. Stimulating or reinforcing political interest: Using panel data to examine reciprocal effects between news media and political interest. Political Communication. 2011;28(2):147-162

48.Jr E, William P, Hayes AF, Shah DV, Kwak N. Understanding the relationship between communication and political knowledge: A model comparison approach using panel data. Political Communication. 2005;22(4):423-446

49.Xenos M, Moy P. Direct and differential effects of the internet on political and civic engagement. Journal of Communication. 2007;57(4):704-718

50.Wang S-LA. Financial Communications: Information Processing, Media Integration, and Ethical Considerations. First ed. New York: Palgrave Macmillan; 2013

51.MacKuen MB, Erikson RS, Stimson JA. Peasants or bankers? The American electorate and the US economy. American Political Science Review. 1992;86(3):597-611

52.Hilgert MA, Hogarth JM, Beverly SG. Household financial management: The connection between knowledge and behavior. Federal Reserve Bulletin. 2003;89:309-322

53.Sabri MF, Aw EC-X. Financial literacy and related outcomes: The role of financial information sources‘. International Journal of Business and Society. 2019;20(1):286-298

54.Cao Y, Liu J. Financial executive orientation, information source, and financial satisfaction of young adults. Journal of Financial Counseling and Planning. 2017;28(1):5-19

55.Rhine SLW, Toussaint-Comeau M. Adult preferences for the delivery of personal finance information. Journal of Financial Counseling and Planning. 2002;13(2):11-26

56.Jansen D-J, Neuenkirch M. Does the media help the general public in understanding inflation? Oxford Bulletin of Economics and Statistics. 2018;80(6):1185-1212

57.van der Cruijsen C, de Haan J, Jansen D-J, Mosch R. Knowledge and opinions about banking supervision: Evidence from a survey of Dutch households. Journal of Financial Stability. 2013;9(2):219-229

58.Worldbank. Gross Domestic Product 2020. World Development Indicators Database. 2020. Available from: https://databank.worldbank.org/data/download/GDP.pdf

59.Reuters. Timeline: The rise and fall of Wirecard, a German tech champion. Reuters. 2021. Available from: https://www.reuters.com/article/us-germany-wirecard-inquiry-timeline-idUSKBN2B811J

60.Correctiv. The Cumex Files. A Cross-Border Investigation. Correctiv. 2018. Available from: https://correctiv.org/en/top-stories-en/2018/10/18/the-cumex-files/

61.Hallin DC, Mancini P. Comparing Media Systems. Cambridge: Cambridge University Press; 2004

62.Moorman C, Diehl K, Brinberg D, Kidwell B. Subjective knowledge, search locations, and consumer choice. Journal of Consumer Research. 2004;31(3):673-680

63.Atkinson A, McKay S, Kempson E, Collard SS. Levels of financial capability in the UK: Results of a baseline survey. Public Money and Management. 2006;27(1):29-36

64.Strauß N. Financial journalism in today’s high-frequency news and information era. Journalism. 2019;20(2):274-291

Written By

Nadine Strauß, Sophie Knowles and Vesile Cinceoglu

Submitted: 21 July 2023Reviewed: 30 July 2023Published: 29 August 2023