Abstract

Financial Literacy plus new purchasing power can drive rapid and environmentally sustainable, local-to-global, economic development. Historically, new technologies promote new forms of money and commerce that usher in new economic eras. This chapter is for leaders and innovators in financial services and sustainable economic development. It reveals an emerging era of sustainable prosperity for all. The world can now eradicate centuries-old poverty and inequality at the pace of mobile apps and social media. The funding for this paradigm shift is a next-generation financial instrument and not higher taxes, deeper debt, or redistribution of wealth schemes. The chapter introduces the first token-less ledger currency that is distributed through a public Business-Community Wealth Ledger (BCWL). Dual Currency transactions integrate fiat currencies with wealth-backed ledger currencies, monetizing and mobilizing currently underutilized business resources and increasing profits for participating businesses.

Keywords

- financial literacy

- ledger economics

- ledger dollars

- dual-currency pricing

- underutilized assets

1. Introduction

The global banking and credit union industry is one of the most powerful industries on the planet. While often blamed for global economic inequality or economic disasters, such as the 2008 global economic downturn, global banking—with the right tools and a profit motive—can rapidly fund and deliver economic solutions of enormous magnitude. At present, banks and credit unions demonstrate their good intentions through their foundations and charitable giving; their support to entrepreneurial start-ups; their volunteer, wellness, ESG, and green teams; their investments in community economic development; and more. But the large-scale programs that target the unbanked primarily center today on teaching financial literacy. These financial-literacy programs operate far below their potential to raise-up individuals, and do not transform the poverty facing economically disadvantaged families and communities. Unfortunately, financial Literacy does not give people the purchasing power needed to improve their standard of living and quality of life nor to send their children to better schools and colleges.

2. The modern economic context

Such material scarcity should be a relic of the past. Today, food is an abundant renewable resource. Education and healthcare are also abundant renewable resources. Everything digital from music and videos to online games and educational content is virtually infinite. The technologies, labor skills, global economic infrastructure, and renewable resources needed to rapidly provide affordable housing on a global scale are all abundantly available. All these resources can be deployed across the globe even more rapidly than when the world mobilized for World War II in only a few years—over 75 years ago—with none of today’s global economic infrastructure. The United States went from the end of the Depression to full war preparedness in a mere 14 months, without sending the population to trade schools or colleges. Everything needed was achieved through on-the-job training [1]. A modern day commercial example is how the Sharing Economy, using modern technologies, created millions of jobs and billions of dollars of new wealth in only a couple of years by mobilizing the modest underutilized resources of an empty room in someone’s home or an idle car and driver (Figure 1).

Figure 1.

Continuous economic improvement.

We have become accustomed to living with massive, underutilized wealth side-by-side with massive unmet needs in the US and across the world. Grocery store aisles, full of groceries, are empty of customers more than they are full. College desks are empty more than they are full. Restaurants, movie theaters, fitness clubs, shopping malls, car dealerships, stadiums, and more are all empty more than they are full—all side-by-side with unmet needs for these very products and services by families and communities. This makes no sense. Because of this abundance, individuals, families, and communities across-the-globe no longer need to endure poverty, hunger, poor health, lack of quality housing and education, nor other reflections of poverty that are an outdated inheritance from the past. The same is true of the glaring disparities in wealth and opportunities that plague communities and nations everywhere. Equity is no longer a matter of taking from some and giving to others. That is a fearful myth that holds back progress for the entire human race.

The challenge and the opportunity lie in creating new economic efficiency to produce and distribute needed goods and services from within the massive underutilized productive capacity found across the private, public, and nonprofit sectors alike. Achieving the United Nations Sustainable Development Goals (SDGs) by 2030 will no longer be a challenge if we mobilize around a common vision and deploy a new cooperative financial instrument. Our powerful, global free-enterprise system, combined with social entrepreneurial business models, can rapidly carry the entire human family into a twenty-first century of human cooperation and sustainable prosperity.

What has been the hold up? Poverty–and its unwelcome offspring including crime, inequality, poor health, discouragement, and class warfare–only persists because economics and commerce confuse the separate, but distinct, roles of money and wealth. Money is only one essential tool of wealth creation. Other essential tools include technology, infrastructure, human skill and creativity, planning and design, as well as materials and energy. Producing and distributing wealth is the objective of commerce. Wealth is reflected in both a nation’s standard of living and its quality of life. While money should merely be a tool of wealth creation, money has sadly become the master of wealth creation [2]. While money was once based upon scarce commodities such as gold and silver coins or precious stones, money is today largely electronic debits and credits in computers, seen as bank accounts and stock portfolios. Yet we fail to grasp how money is running the show in the modern world and driving the economic booms and busts that still plague our economies.

3. Exchange-token money versus wealth

Money has historically played several roles in modern economies as “a unit of account, a medium of exchange, a store of value, and a standard of deferred payment” [3]. Yet, as a unit of account, money constantly changes value. Today a loaf of bread might cost $3.00, but because of inflation, it may cost $5.00 down the road or because of recession/depression it may one-day cost $1.00. Money’s changing value is like declaring that a foot is 12 inches long today, yet may be 15 inches long tomorrow or 9 inches long next month. So money, as tokens of exchange, fail as reliable units of measure.

Similarly, exchange-token money fails as a store of value. Consider the 2008 economic crash, when nothing of real value “disappeared,” Yet when valuations fell, the US Federal Reserve declared that trillions of dollars in wealth had disappeared [4]. Valuations represent the price (measured in money) that someone’s stock, company or home would likely fetch in the market. On the other hand, not the tiniest bit of real wealth disappeared in 2008: technology; infrastructure; human skill, knowledge, and creativity; products and services; materials and energy… all still existed throughout the economic crash.

The distinction between money and wealth helps us to understand the failure of cryptocurrencies to advance meaningful economic development or to solve any of today’s social, economic, and environmental problems. Cryptocurrencies are fundamentally new tokens riding on a new ledger (the blockchain), and they represent a next generation of money speculation. Why bother to produce needed goods and services if you can quickly and easily make money through speculation? In fact, cryptocurrencies are much like poker chips. A person buys them with dollars hoping to cash them out for far more dollars: not a great value to society compared to building companies that produce products and services that people need.

This confusion between money and wealth also explains how the economy can grow to many times the wealth that it once contained, and yet six gigantic economic sectors–private; public; nonprofit; cooperative; sharing economy and social impact investing–have not solved the many social, economic, and environmental problems that have all arisen since the post-World War II economic boom. In fact, in the 1950’s, it was common for a single head of household working a 40-hour week to buy a house, a car, put food on the table, and pay for a college education for the children [5].

In contrast, today, two working parents, even working overtime, might struggle to be middle-class, with their children leaving college saddled with enormous financial debt. Instead of advances in the factors of production creating an ever-higher quality of life across-the-board, societies are operating at a mere fraction of their true potential, while underutilized productive capacity is a major segment of the economy [6]. Unfortunately, businesses often downsize and fail (the so-called “creative destruction” feature of free enterprise), while there are still extensive unmet needs for these very products and services in the United States and across the globe. This is the price we pay because economics confuses money (the tool) with wealth (the very products, services, infrastructures, community amenities, etc.) that determines the quality of life for families and communities.

Modern exchange-token economies fail to distribute abundant wealth, which languishes everywhere today as underutilized productive capacity, because win-lose competition over money makes wealth appear to be scarce. Instead of encouraging and supporting people to contribute to society efficiently (at every level of skill), purchasing power is distributed through the eyedropper of paychecks. This inefficiency can be addressed by a social entrepreneurial innovation that combines financial literacy with new purchasing power, creating a next generation of currency that monetizes our abundant excess capacity.

Every new economic era produces new organizational forms for individuals, families, and communities to achieve more of their potential. In the modern era, we have created a global economy that, while it has generated massive material and monetary wealth, remains in many ways both inefficient and inequitable. While a mere 12% of the global population is Caucasian, that cohort controls over 85% of the monetary wealth in the world [7]. Considerable efforts by banks, credit unions, and other financial institutions seeking to promote financial literacy fail to address wealth and power inequities. Most financial-literacy programs do not provide economically disadvantaged populations, especially communities of color, with the economic resources they need to rise out of poverty. By operating within today’s traditional token-money-centered economic paradigm, these programs fail to tackle poverty at its economic roots. The time has come to develop a new economic language—a new financial literacy—around equity that raises the standard of living and quality of life across-the-board for families and communities without relying on higher taxes, deeper debt, or redistribution of wealth schemes.

4. Introducing economic ledgers to supplement exchange-tokens

This chapter introduces a new model of financial literacy, the engine of which combines traditional bank-based financial literacy programs for the unbanked with a new form of enhanced purchasing power called “Ledger Dollars (L$)” [8]. The source of this new purchasing power is a business innovation and wealth distribution system termed “Ledger Economics.” With the decline in use of physical cash and the increasing use of digital debit and credit cards has come a growing recognition of the difference between money, a unit of exchange, and wealth, the goods and services, knowledge and skills, family and community values that surround us. We often call people with a lot of money “wealthy” and those with little money “poor.” Yet we also recognize that there are many other forms of wealth—wealth of human knowledge, lived experiences, social connections, self-knowledge, community cohesiveness, environmental resources—all of which exist abundantly around us. These kinds of wealth are all multiplied when they are shared and diminished when they are not.

The distinction between money and wealth is like the difference between a photograph of a place and the place itself (or understanding that a map is not the terrain). Akin to a photograph, money is a useful abstraction of reality and a valuable tool that we can exchange when we need to, but also like a photograph, money cannot capture nor substitute for all the unseen wealth of a place. A place and its people may lack money, but they may not be poor if they have a lot of family and friend relationships, social and cultural traditions, natural resources, and practical knowledge and skills. Nor does any “non-cash” wealth disappear during economic downtowns or pandemics. People may lose jobs or money, but they lose none of their knowledge and capability, which can continue to grow if they choose.

The distinction between money and wealth is particularly relevant given the inequities that the COVID-19 pandemic revealed. While many people struggled to make ends meet during the pandemic, and while communities of color suffered higher rates of infection and death than most white communities, we also saw the emergence of global protests against police brutality on the part of many people, of all races, in many communities: urban, suburban, and rural [9]. While economic inequality increased in many countries during the pandemic, so too did collective action and the community wealth that aggregated community assets represent. Many people lost paychecks during the pandemic, but they discovered dormant purpose and pursued their passions.

The pandemic also showed how much a focus on money rather than wealth has created an enormous amount of excess capacity, wasted resources, and under-used assets of all kinds. It took the closure of most stores and offices during the pandemic and the shift on the part of many people to e-commerce and telecommuting to show how much competitive duplication of goods and services existed in the traditional economy, how much time we wasted going from one place to another, and how much under-utilized space existed all around us. That duplicate effort, wasted time, and excess space did not just represent the normal cost of doing business. They are the result of confusing money and wealth, as we chased money while over-producing. Chasing money in this way also puts downward pressure on profits, wages and people’s purchasing power, and misses the fact that there is a tremendous amount of untapped wealth in the world, side-by-side with unmet need.

We continue to compete for money without monetizing or measuring our wealth, a paradox that the pandemic revealed. The pandemic forced us all to depend upon those with whom we quarantined and to seek help from and to help others, drawing upon familial and social connections as well as the aid of communities. The pandemic, in other words, accelerated a shift not only from a cash-based to a debit- and credit-card-based economy, but also from competition over money to an appreciation of the multiple forms of wealth in our communities and among ourselves.

This, in turn, suggests a new way to think about financial literacy. Rather than thinking about it in terms of money, we should think about it more broadly in terms of available wealth. When one of America’s most under-appreciated economic thinkers, Henry David Thoreau, went to Walden Pond, he did so to imagine a new kind of economy in which “the cost of a thing is the amount of … life which is required to be exchanged for it, immediately or in the long run” [10]. He argued in the first chapter of

During the pandemic, with many people having less money because of layoffs, furloughs, or pay cuts, the cash economy sometimes seemed like our enemy, a threat to our homes and families. At the same time, we had to learn to be economical in how we lived: reducing our expenditures, eliminating inessentials, and stewarding what we had. While the political economy that drives our legislatures and stock markets seemed increasingly disconnected from our lives, the economy of living, as Thoreau called it, defined the deposits and withdrawals of our day-to-day struggles.

What possibilities does Thoreau’s economy of living offer in terms of financial literacy? It might mean that we learn to put a price on what every moment in our life meant to us and to evaluate the cost of everything in terms of the time it would require us to give it up. Would we really assess our time in terms of some wage that someone else has decided to offer us or would we, instead, demand a wage commensurate with the real value that our life has for each of us? Much more is possible through continuous economic improvement where every advance in technology and human capabilities raises the quality of life, shortens working hours, and reduces damage to the natural world.

The contemplation of one’s own death that occurs during a pandemic can make such questions more urgent. Money comes and goes, but time is all we have, and Thoreau’s economy of living provides a measure of what is the most important of our scarce assets: our own individual lives. Some people may be fine with wasting that asset, frittering their lives away in details, as Thoreau said, or making a living working long hours that keep us away from our families and, in many cases, contribute questionable value to society. But with a novel virus reminding us that we are mere mortals, weighing the cost of things according to the time we must give up in return for them may be the basis for a post-pandemic economy worthy of what we all just went through. Modern ledger theory views wealth as an abundant renewable resource as opposed to the scarcity mentality that surrounds money: there is rarely enough money to do all the things that make life rewarding, but we are surrounded by almost inexhaustible amounts of wealth.

5. Challenges in the modern economy

A dual currency ledger-based economic system may address some of the more perverse aspects of the modern economy. The US healthcare system profits off illness and receives relatively little financial gain by promoting wellness [11]. A heart attack is a major economic event, while people quitting smoking lowers the gross domestic product. The pandemic showed how health disparities continue among those who lack sufficient purchasing power to lead healthier lives. Many employers track and reward their employees for wellness activities, programs proven to reduce healthcare costs, absenteeism, Worker’s Compensation Insurance, and disability claims. But those savings mostly occur at the edges of the system, benefiting those already employed, while most health disparities occur along ethnic and racial lines, regardless of employment status. Nor do these wellness programs address the systemic cause of so much ill health in a country like the US, with a food system awash in sugar, salt, and fat, in a physical environment that leads many people to engage in a lot of sedentary behavior. The stress of modern life also drives many family members to alcohol and drug abuse, which are major obstacles to good health.

Transforming health and wellness in our society requires changes in the underlying economics that drive them. That might have seemed impossible prior to the pandemic, but we saw how quickly and profoundly so many things changed in 2020. Why cannot we also change the economy, which is just another designed system and one with numerous perverse outcomes, as our healthcare system shows? What if the ledgers with which we track wellness activities went further and paid people to lead healthier lives in a currency that extends people’s purchasing power with merchants who have excess capacity in their establishments? Imagine using excess capacity in the pharmaceutical industry to provide affordable medications for seniors, producing and distributing needed medications profitably but at reasonable costs. Medications are a perfect example where the marginal cost of production for an additional quantity of products is a tiny fraction of the initial production costs [12].

These ideas extend beyond the healthcare system and wellness programs. The monetization of business’s underutilized productive capacity impacts every area of work and community life. Imagine workplaces where everyone cooperates to maximize productive efficiency. Instead of win-lose competition over money, visualize an economy where everyone collaborates to rise together. Imagine an economy where advances in technology and other factors of wealth production create “Continuous Economic Improvement (CEI),” defined as an ever-higher quality of life, with ever shorter working hours, and ever less damage to the natural environment.

Most nonprofits utilize volunteers to do the work these organizations do in the world, while often lacking funding to pay for that labor. At the same time, most businesses could use more customers, who have many choices for where they spend their limited funds, and most people could use more goods and services that they do not have enough money to purchase. These three entities occupy the same communities, with money/purchasing power or cash being the only missing ingredient for both merchants and families to each get more of what they want. Meanwhile, an enormous amount of wealth that exists in every community goes unleveraged and unmonetized.

That misalignment of purchasing power and available goods and services undermines the potential for CEI. As a society, we continuously improve our personal and community wealth: our technology and infrastructure, our knowledge and skills, and our personal and social networks. And we continuously upgrade our access to the abundant ecosystem services that nature provides us: solar, wind and geothermal energy, forests and row crops, carbon sinks and our oxygen supply. We have never solved the boom-and-bust cycles in our economy because we do not see the relationship to competitive, money-centered economics versus cooperative people- and planet-centered economics. In contrast, we should expect and make sure that our economy provides an ever-improving standard of living and quality of life, with ever-shorter working hours for everyone and ever less damage to the environment.

Instead of holding down production to the level of available purchasing power–while periodically downsizing much of the economy’s productive capacity–CEI would raise the purchasing power for individuals, families, and communities to match society’s ever-increasing productive capacity. This model of cooperative efficiency would not raise employer labor costs, increase taxes, or deepen debt. Instead, it would leverage society’s current untapped wealth without requiring government subsidies or redistribution of wealth schemes. It would quickly demonstrate that business innovation and the profit motive are far more effective than left-versus-right politics or labor-versus-management battles at solving today’s daunting social, economic, and environmental challenges.

6. A community ledger precedent

An early exposition of this idea was put forth when the psychologist B.F. Skinner wrote a book published in 1948 as

In contrast, our current pricing model, based on the supply of desired goods and services in the face of consumer demand, is extremely inefficient. Masses of desirable goods and services are not distributed where they are needed for lack of purchasing power (money!) in the hands of customers/families. While

7. How a ledger economy would work

How would such an economy work in the real world, as opposed to a novel? Employers would continue to pay their employees in cash, but workers might also receive L$ as a supplement to their paychecks—for their wellness achievements or their volunteer activities. Alternatively, an employer with an excess amount of goods or services might offer, as an employee benefit, L$ with which to buy down the business’s excess capacity. Employees would redeem their L$, which would then be taken off the books.

There are three everyday business practices that already monetize and distribute enormous amounts of underutilized business capacity.

The Sharing Economy, utilizes cash transactions combined with new technologies to leverage underutilized assets, be they an empty apartment, an unfilled car seat, or idle workers.

Employee-benefit programs represent a noncash example, making a business’s excess goods and services available to employees at little or no cost.

A ledger-currency example is loyalty rewards programs, in which benefits to loyal customers are tracked in a ledger, with points being issued, redeemed, and then taken off the books.

In today’s economy, all three examples of monetizing excess capacity are competitive business models benefiting one company against their competitors. We introduce a cooperative network where pooled excess capacity benefits all companies, all employees, all families, and all communities.

Businesses could redeem the Ledger Dollars (L$) of one another’s employees in the same way. Let us say a person earned L$ for doing valuable work in a community—mentoring children in the local school, helping a community group clean up a vacant lot, or taking care of elderly parents. Merchants with excess capacity—mostly empty grocery aisles, unfilled restaurant seats, unused equipment, unsold merchandise—could offer those at reduced cash prices by accepting purchases partly in cash and partly in Ledger Dollars, which would move their merchandise or utilize their services while also reducing the costs to their customers and benefiting the communities within which they exist. Businesses would, in other words, accept a combination of cash and Ledger Dollars, monetizing their excess capacity and increasing the purchasing power of employees, volunteers, students, retired people, the unemployed and stay at home parents everywhere.

Monetizing wealth through an additional ledger currency would expand the capacity of the public and non-profit sectors as well. A city, for example, could credit its residents for contributions of time or insights they provide to planning processes or committee assignments. Or a nonprofit could credit volunteers for their contributions to the mission of the organization or the aid they provide. These sectors would not only expand their impact, but also engage more people in their work by recognizing and compensating for that effort. It would literally return us to the origin of the word “economy” with roots in the Greek words for “household management,” and to the original connotation of the word, involving ideas of thrift and frugality. Instead of wasting the talent and good intentions of the people in a place, a ledger economy would fully utilize the physical, social, and natural assets of a community.

Everything we need to make such a system work already exists. There are digital ledgers aplenty on the Internet, most of them downloadable for free. It only needs agreement among the public, private, and non-profit sectors, each looking to either attract more customers, aid more citizens, or expand people’s purchasing power. And once available, a second currency would require little coaxing of people to participate: who would not want recognition and compensation for the voluntary, unpaid work they already do to further a mission they believe in or to take care of those for whom they feel responsible? While many people might say that they do not do this work for the money, most would welcome being rewarded in a way that would also extend their ability to purchase what they need or know that they are helping others who currently lack the financial resources to afford what they need.

All it takes is openness to the idea that the economy is a designed system and money a human creation, both of which are not working well for large numbers of people in the US and across the globe. We cannot just do more of what is not working well: looking for more money to do what win-lose competition over money is failing to accomplish in economic development. In the modern economy, the more money that goes into circulation (from whatever source), the more competitive duplication is created. Instead, we can re-imagine how to make our economy work for more people, in more equitable and environmentally sustainable ways. Indeed, solving the issues of equity and sustainability lies at the heart of why we need to uplevel the current economy using twenty-first century technologies and renewable resources.

Governments and foundations have historically sought to address inequities through fiscal means—taxation and subsidies—or philanthropic ones—gifts and grants. But those monetary methods miss the mark by assuming that we can eliminate inequities with more cash, perpetuating the idea that people without money need charity. Instead, the less cash a community has, the more it relies on non-monetary workarounds, be they familial, social, cultural, or spiritual. Examples include bartering between community members (watch my kids and I’ll give you vegetables from my garden); 12-Step groups to address addiction, rather than the expensive healthcare system; volunteer programs to feed the hungry such as Second Harvest and the Humanity Alliance; the sharing economy, which offers less expensive rides and places to stay than the traditional economy; In-kind donations from established businesses and more. All of these are creative workarounds for how the cash economy is underserving many individuals, families, and communities. Non-cash commerce is often far more relational, in contrast with the primarily transactional nature of money-based commerce, and L$ enhance that relation-based wealth and enable many more people to stretch currently limited cash resources.

That suggests an economy operating at a different scale than the traditional one that is based on national currencies. Ledger Dollars operate less like national currencies and more like popular loyalty rewards programs, which are a business-issued currencies backed by each business’s available products and services. But unlike loyalty rewards, which reward consumer spending, so that whoever already has the most money now also gets the most rewards, L$ reward far more than spending. Economic ledgers can better match the production of goods and services with business, employee, customer, family, and community wants and needs. National currencies are blunt instruments to address economic inequity, as traditional money chases the highest rate of return. At the same time interest and dividends bring ever more money to those who have the most money. Ledger Dollars encourage a more level economic playing field through more careful and equitable production and distribution of real wealth without any old-fashioned redistribution of wealth schemes. Lastly, national currencies encourage consumerism to promote economic growth, which has negative social and environmental consequences. In contrast, Ledger Dollars promote a higher quality of life by engaging everyone in greater economic efficiency and voluntary sharing of currently idle resources. This approach promotes an ever-higher quality of life without promoting consumer culture. In a post-pandemic world, weary of the physical idleness and social isolation that COVID-19 caused, a new, more equitable and less wasteful economy is just the cure many people are looking for.

None of this means that money is unimportant. During and after the pandemic, many people lost jobs and livelihoods, faced bankruptcy or eviction, and exhausted checking and savings accounts. In response, many governments came to people’s aid, distributing financial resources. Instead, a ledger-based, digital economy helps people and communities leverage untapped wealth and lets businesses market their excess capacity in ways that use the talents, skills, and knowledge of people leveraging assets currently going to waste. Ledgers may seem boring; who wants to talk about accounting protocols and financial transactions? And ledgers may appear an unlikely basis upon which to build a new economic model. But they address the challenges of money-centered economics and commerce. Unlike our money economy, ledgers do not crash or suffer inflation, recession or depression; they do not support artificial scarcity or money hoarding, and they do not lend themselves to speculation or theft. Moreover, ledgers help us to measure not just the exchange of cash, but to account for other forms of capital that we have not tallied before.

Ledger economics also gives youth incentives to be entrepreneurial. Universities could accept L$ towards tuition, books, meals, and student housing as part of a Ledger-Dollars program that helps students subsidize their college educations. For example, Fernando and Melissa earn L$ during their freshman and sophomore school years by working part-time in a local community nonprofit organization that is part of the program. The two of them purchase clothes, school supplies and other necessities at the university’s store in a combination of US Dollars and Ledger Dollars. Seeing the potential of this cash-like financial incentive, Fernando and Melissa, upon graduation, set up their own non-profit organization to build alliances of institutions, merchants, and community organizations to participate expand the reach and impact of the Ledger Dollar system.

Ledger economics could lead to an explosion of creativity and resources and spawn a cooperative, win-win attitude in the community. Consider how after World War II, the United States led 28 nations in the Marshal Plan to rebuild Europe and Japan. Imagine a twenty-first century Peace Corps funded by Ledger Dollars many times more impactful than today’s efforts, or a twenty-first century GI Bill for Youth, where 2 years of domestic or international service work could fund a full-ride college education in Ledger Dollars, because college campuses are awash in empty college desks, empty dorm rooms, and empty cafeterias. Also, imagine what such a mobilization of youth during Covid-19 might have done to take the incredible burden off of our First Responders.

Many businesses, especially restaurants, which were among those most negatively impacted by the COVID-19 pandemic, may be ready for innovation. On the one hand, the pandemic revealed the excess capacity of restaurants, as their dining rooms remained closed, and those that stayed in business had to develop new delivery models, like take-out, drive-through, and home-delivery options. On the other hand, the pandemic also showed how to leverage excess capacity to reduce food costs for families. Some restaurants developed hybrid models in which they delivered components of meals that people could prepare at home, using the distributed network of kitchens in customers’ homes. In this way, consumers became producers of the food they ate, using the underutilized capacity of their own kitchens to their advantage [14].

Such innovations tapped a rarely recognized and under-utilized asset in virtually every community: the unleveraged talent and skill of ordinary people. Traditional economists tend to separate producers and consumers, employees and customers, even though, obviously, most consumers need to produce –i.e. work—to buy what they need. That division between producer and consumer leads to the paradox of companies reducing production costs by laying off employees, while also trying to increase consumer spending, including by those just laid off employees. This is one of the greatest lessons of the pandemic: in a global economy that measures wealth in terms of the amount of money one has or controls, it overlooks other forms of wealth that rarely get measured and monetized, and that have far greater value than anything money can buy. The father of capitalism, Adam Smith, recognized this as the paradox of value [15]. He asked why we value diamonds, which we do not need, and do not value water, which we cannot live without. From a monetary point of view, the answer is obvious. Diamonds are rare, so people who want them will pay more money for them than they will for water, which—in Adam Smith’s time and place—was widely available. But from a value point of view, his paradox is not obvious. Water is more valuable than diamonds and will always be so because of the essential role it plays in keeping us—and every plant and animal on the planet—alive.

The same paradox exists in our conflation of money and wealth. By tapping excess capacity that surrounds us and increasing purchasing power by rewarding people for socially beneficial activities, we increase everyone’s quality of life through an equitable economic system that recognizes the under-valued wealth that exists in every one of us and everywhere around us. That represents a new—and truer—form of financial literacy. Continuous economic improvement based on tapping the excess capacity that is all around us and increasing purchasing power by rewarding people for socially beneficial activities raises the standard of living and improves our quality of life without taking any money or resources away from anyone. This approach can provide rapid, profitable, equitable, and ecologically sustainable economic development wherever people seek to embrace it. Meanwhile, the end of the grow-or-die business imperative opens the door for efficiency and cooperation to replace growth and money-competition as the engines of economic progress.

8. Beyond left versus right

Traditional, competitive, money-centered economics and commerce rests upon the now outdated notion of scarcity, pitting people, communities and nations against one another in a battle for money and domination. A significant challenge to solving our economic problems is the current left-versus-right polarization and stalemate. This status quo prevents us from working together on needed solutions and keeps us from seeing the inherited but now outdated roots of our social, economic and environmental challenges. Ledger economics can counter that polarization by uniting companies, communities, universities, political organizations, and government agencies in a common strategy for progress.

Imagine a Business-Community Wealth Ledger (BCWL) that leverages excess business capacity and promotes continuous economic and community improvements. For Conservatives and Libertarians, the BCWL is 100% voluntary and self-funding. It is business-led, market-based and profit-driven. It respects private property. For Liberals, radicals, greens and socialists the BCWL provides economic development resources that are immediate and not trickle down (Figure 2).

Figure 2.

Beyond left versus right.

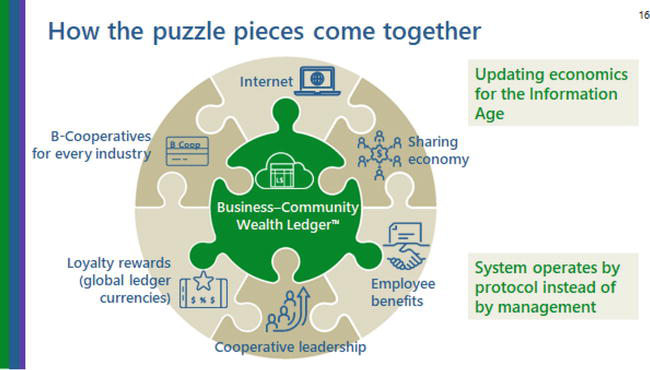

The BCWL is an example of Ledger Economics, which builds upon the success of our free enterprise system and improves upon it, much the way that electronic banking and ecommerce have been improvements to old-fashioned paper currency and banking. Ledger Economics brings new opportunities to address social, economic, and environmental challenges. It also will likely bring new challenges that traditionally accompany paradigm-shifting innovations. Ledger Economics does not rely on exchange tokens, such as coins, paper currency or electronic debits and credits in computers, all of which circulate. Ledger Dollars are issued, redeemed, and taken off the books, like loyalty rewards. When Merchants redeem loyalty rewards, they do not use them to pay employees, vendors, or taxes. Ledgers can also account for dual currency sales, in which businesses accept both US$ and L$, as an alternative to the traditional discounting of goods and services, which puts downward pressure on profits and wages. Merchants profit in US$ from dual currency sales, while at the same time, pooling their underutilized capacity into a public asset, mobilizing rather than wasting underutilized business/community wealth (Figure 3).

Figure 3.

Ledger dollars versus traditional purchases.

Merchants contract with the BCWL, using ratios and restrictions based upon their marginal cost of production. When discounting, merchants accept fewer dollars to increase sales, resulting in downward pressure on profits and wages. In contrast, a new financial instrument such as the Business Community Wealth Ledger, backed by today’s underutilized business capacity, increases purchasing power for employees, families, and communities. Like the Internet, the BCWL would live in the Commons, owned by no-one and managed by protocol rather than politics. Also like the Internet, the BCWL supports mass customization rather than government control. Once a person or a company follows the Internet protocol, they can engage in myriad options. They can do e-commerce, they can engage in charity, and they can have complete freedom of speech and association. As well, they can be for or against guns, drugs, abortions, hunting or veganism. This could be a significant step towards a truly inclusive and equitable, free-enterprise economics, where people all have growing resources to live by their own values.

Merchants sign dual-currency contracts with the BCWL to accept L$ along with US dollars for their goods and services, enjoying cash profits, plus free employee benefits. Members would sign up with the BCWL and receive L$ for their rewardable activities, looking online for the merchants who are part of the system and where they can spend their L$. Community organizations, such as non-profits and school districts, would serve as Sponsors and report to the BCWL the rewardable Member activities. Schools sponsor students; employers sponsor employees; community organizations sponsor volunteers, religious organizations sponsor members; the government sponsors Social Security recipients, public assistance recipients, the unemployed and so forth. Upon receiving the reports of Sponsors, the BCWL would make L$ deposits into member accounts. When L$ are redeemed by Merchants, they would be taken off the books like loyalty rewards, and not circulate like traditional (token) money.

With such a system, everyone wins.

Merchants profit from increased sales and free employee benefits.

Members prosper from expanded purchasing power.

Sponsors benefit from the incentive people have to volunteer or contribute to their communities.

At the same time, disparities would close through new economic efficiencies:

Leaders gain effective tools to address historic challenges.

Workplaces become centers of innovation, learning and contribution.

Families and communities receive newfound wealth that reflects the true value of what they have to offer (Figure 4).

Figure 4.

Business-community wealth ledger.

9. Introducing B-cooperatives

The sharing economy, employee benefits, and loyalty rewards are all established ways to capture and distribute underutilized business capacity. We propose another economic innovation that we term “B-Cooperatives.” Today’s B-Corporations balance profit with purpose, benefiting communities and the environment as well as their shareholders. Our proposed B-Cooperatives extend that idea beyond individual companies to entire industries, bringing companies together, voluntarily, so that the progress historically lost through competition over money is addressed through free-enterprise cooperation.

The Visa system is an example of the power of industry-wide cooperation. Faced with multiple, competing credit-cards from virtually every bank, Visa created a cooperative association in 1958 using a single industry standard for credit cards, entirely operated by protocol. This brought workability and profitability to the then beleaguered credit-card industry through: (a) a new financial instrument, (b) a new payments platform, and (c) a new cooperative network of banks. The same cooperative framework can be applied to the emerging ledger economy. Rather than multiple competing ledgers, a cooperative association—akin to Visa and the Internet—can define a single industry standard, a universal economic ledger, operated by protocol. This would increase the level of cooperation and participation among Merchants, expand the options and buying power of Members, and grow the amount of community participation and volunteerism among Sponsors and Members.

10. Conclusion

Ledger economics would ultimately move the global economy away from win-lose competition over money and towards more efficient win-win economic cooperation. This would benefit individuals, families, and communities everywhere. It would also answer the historic challenge posed by visionary futurist and inventor R. Buckminster Fuller to the world decades ago: “How do we make the world work for 100% of humanity, in the shortest possible time, through spontaneous cooperation, without ecological offense or the disadvantage of anyone?” [16].

Acknowledgments

The authors would like to express their appreciation to Chris Brooks and Larry Walker for their valuable contributions as reviewers of this work.

References

- 1.

Koistinen PAC. Mobilizing the world war II economy: Labor and the industrial-military Alliance. Pacific Historical Review. 1973; 42 (4):443-478. DOI: 10.2307/3638133 - 2.

Watts A. Wealth versus money. In: Does it Matter? Essays on Man’s Relationship to Materiality. Novato, California: New World Library; 1971 - 3.

Shapiro D, McDonald D, Greenlaw S. Principles of Economics, 3rd ed. Houston: Rice University, Open Stax; 2022 - 4.

Weinberg J. The great recession and its aftermath. Federal Reserve History, Federal Reserve Bank, Washington D.C; 2013 - 5.

Johnson DS, Rogers JM, Tan L. A century of family budgets in the United States. Monthly Labor Review. 2001; 124 (5):28-45 - 6.

Board of Governors of the Federal Reserve System Industrial Production and Capacity Utilization—G.17, Federal Reserve Bank, Washington D.C; 2023 - 7.

Global Wealth Report 2023, Leading Perspectives to Navigate the Future, Credit Suisse AG, UBS; 15 June 2023 - 8.

Fisher T, Hodroff J. From money-Centered to People- and Planet-Centered Ledger Economics: Leveraging the Hidden Wealth of Underutilized Productive Capacity. London: Intech Open; 2021 Available from: https://www.intechopen.com/chapters/75019 - 9.

Fisher T. Space, Structures and Design in a Post-Pandemic World. London: Routledge; 2022. pp. 17-22 - 10.

Thoreau HD. Walden. New York: Random House; 2000. Chapter 1 - 11.

Shmerling R. “Is our Healthcare System Broken?” Harvard Health Publishing. Harvard University: Cambridge; 2021. Available from: https://www.health.harvard.edu/blog/is-our-healthcare-system-broken-202107132542 - 12.

Tuovila A. Marginal Cost Meaning, Formula, and Examples. New York: Investopedia; 2023 - 13.

Skinner BF. Walden Two. Hackett: Indianapolis; 1948 - 14.

Duncan N. Life after COVID: Welcome to the World of Hybrid Restaurants. Charlotte, North Carolina: FSR Magazine; Apr 2022 - 15.

Smith A. The Wealth of Nations. Amsterdam: MetaLibri; 2007. p. 26 - 16.

Cape J. Buckminster Fuller Reader Penguin Books. New York; 1972