Open Access is an initiative that aims to make scientific research freely available to all. To date our community has made over 100 million downloads. It’s based on principles of collaboration, unobstructed discovery, and, most importantly, scientific progression. As PhD students, we found it difficult to access the research we needed, so we decided to create a new Open Access publisher that levels the playing field for scientists across the world. How? By making research easy to access, and puts the academic needs of the researchers before the business interests of publishers.

We are a community of more than 103,000 authors and editors from 3,291 institutions spanning 160 countries, including Nobel Prize winners and some of the world’s most-cited researchers. Publishing on IntechOpen allows authors to earn citations and find new collaborators, meaning more people see your work not only from your own field of study, but from other related fields too.

This chapter discusses the nexus between financial inclusion and financial literacy, focusing on the microfinance institutions’ contribution to increasing of financial literacy and financial inclusion among their clients. The microfinance sector in Bosnia and Herzegovina is perceived as the most well-organized and regulated worldwide. We use it as a case example of how microfinance institutions make changes in the financial system landscape and contribute to the well-being of individuals. During the COVID-19 pandemic, microfinance institutions in Bosnia and Herzegovina organized a series of workshops on digital financial literacy in order to provide their clients with the knowledge related to digital financial products/services used to help their clients better to integrate into the financial system. The chapter provides evidence on digital financial literacy initiatives contributing to financial literacy increase and more frequent usage of digital financial services contributing to greater financial inclusion of individuals. The presented research will contribute to the existing literature in terms of a better understanding of the importance of financial literacy and education in building inclusive financial systems as well as provide evidence of positive practices among financial institutions, namely microfinance institutions in regard to increasing financial literacy.

Faculty of Economics, University of Tuzla, Tuzla, Bosnia and Herzegovina

Meldina Kokorović Jukan*

Faculty of Economics, University of Tuzla, Tuzla, Bosnia and Herzegovina

*Address all correspondence to: meldina.kokorovic@untz.ba

1. Introduction

As one of the preconditions of sustainable economic growth, financial inclusion has been on the policymakers’ agenda for more than several decades now. As it is indicated by the World Bank (WB) [1], universal financial inclusion needs to be achieved by 2020, yet countries still struggle to create a financial ecosystem that is accessible to all. According to the latest Global Findex Survey (GFS) from 2021, account ownership around the world increased by 25% in the 10 years spanning 2011 to 2021, from 51% of adults to 76% of adults [2]. From 2017 to 2021, account ownership in developing economies increased by 8%, but still, there are more obstacles to achieving universal financial inclusion in developing economies due to a number of barriers and lower efficiency of the financial system.

More in-depth analysis provides evidences that, besides the standard set of barriers to financial inclusion (financial products/services being too expensive, lack of necessary documentation, availability and trust in financial institutions, insufficient funds, and religious reasons), financial illiteracy is one of the reasons of poor financial inclusion. Through comprehensive cross-country analysis [3] a positive and significant relationship between financial literacy and measures of financial inclusion was found. The financial measure includes having a bank account at a formal financial institution, including mobile money accounts; the proportion of adults in a country that has a debit card; the proportion of respondents that use a bank account to save; and the proportion of adults in a country that use of debit cards. Thus, it can be concluded that raising financial literacy among the general population can be a good way forward to increasing financial inclusion.

Developing countries, among which is Bosnia and Herzegovina (B&H), are putting efforts to improve financial inclusion through improving financial system regulatory and institutional framework, improving banking systems and increasing awareness of the financial health importance. These efforts are coordinated among financial system regulators (central banks and regulatory agencies), financial institutions as well as civil society organizations working on improving financial literacy and financial health among individuals and on a household level. The importance of financial literacy and financial health was even more emphasized during the 2020–2023 COVID-19 pandemic, which profoundly changed people’s lives in terms of their spending habits and interaction with financial institutions. Then, more than ever before, financial literacy became crucial for maintaining day-to-day payments during the lockdown. In that respect, financial institutions increased their efforts to provide adequate solutions for their clients to overcome challenges imposed by the pandemic. Most of the financial institutions (banks, insurance companies, and microfinance institutors) created online platforms and new mobile applications to ensure their clients have access to their financial products/services.

This chapter provides insight into the efforts of microfinance institution(s) in B&H to improve (digital) financial literacy of their clients in order to ensure their better financial health which will consequently positively impact the performance of the financial institution itself. As a response to the lockdown, one of the leading microfinance institutions in B&H started the imitative series of workshops to improve digital financial literacy among their clients in order to break down the fear of using digital platforms (online banking) for payments. The intention behind the initiative was to empower clients to use online banking in order to shorten the time needed for the completion of payments (prior to using online banking, clients were forced to stand in lines in banks to complete payments), to ensure more cost-efficient payment (on-line payment are less costly than payment in the bank) and, at that time, to decrease the health risk associated with the COVID-19 infection.

2. Financial inclusion and (digital) financial literacy nexus

The definition of financial inclusion is rather complex. As an antipode to financial inclusion, financial exclusion was the firstly introduced concept and it referred to as the process where the poor and disadvantaged are prevented from accessing the financial system [4] and the inability to access necessary financial services in an appropriate form [5]. Being a rather broad socio-economic concept, the most comprehensive definition of financial inclusion was given by the WB [6] in which financial inclusion means that individuals and businesses have access to useful and affordable financial products and services that meet their needs – transactions, payments, savings, credit, and insurance – delivered in a responsible and sustainable way.

However, as the financial system evolves, financial institutions are embracing digital transformation where financial services and products are mostly digitalized, which directly contributes to greater financial inclusion in general. The findings of the latest WB-GFS from 2021 [2] show that COVID-19 boosted the adoption of digital financial services in developing economies and that mobile money has become an important enabler of financial inclusion (especially in Sub-Saharan Africa). Today, financial inclusion is understood through the ability of financial institutions to provide widely accessible financial services/products using digital technologies. In that sense, in today’s academic and practical discourse, the term digital financial inclusion is being used more often and is perceived as the enabler of achieving universal financial inclusion. In respect to defining the concept of digital inclusion, digital financial inclusion, as defined by the WB [7], refers broadly to the usage of digital financial services to advance financial inclusion, i.e., the deployment of digital means to reach the digitally financially excluded and underserved populations with such financial services.

Digital financial inclusion is seen as the fourth stage of the financial revolution after developing microcredit, microfinance, and financial inclusion [8]. From the first microcredit and microfinance products/services (which will be discussed in more detail in the next section), the new financial landscape evolved to boost the inclusion of the adult population into the financial systems. Digital transformation of financial services has significantly increased financial inclusion, but still, the financial landscape counts on the financial institutions such as microfinance organizations to adopt the new technologies and provide digital financial products/ services to the unbanked part of the population.

One of the key barriers to (digital) financial inclusion is a lack of financial and ICT knowledge as reported by [9]. For the past several decades, financial literacy has been the key driver of financial inclusions since a better understanding of basic financial concepts, the usability of financial products/services and their contribution toward financial health and overall financial well-being of individuals is enabling greater involvement in the financial system. To that end, government, non-government organizations, universities, and financial service providers are creating different initiatives and education programs to improve financial literacy with more or less success. However, what research shows [10] is that promoting financial literacy is a way to ensure people live more financially secure lives.

Now, we turn our attention toward understating the microfinance landscape and its contribution to financial inclusion.

3. Microfinance and its contribution toward financial inclusion

Measured by the level of financial products and services ownership and usage, financial inclusion is directly linked to the ability of financial institutions to reach out to each adult individual. In a dominantly bank centric financial system, where commercial banks play the key role in providing bank accounts, credit and debit cards, savings and borrowing offers, individuals are often faced with the situation that they do not meet strict banking rules to be the bank clients or, what are the most usual case, these products and services are too expensive for lower-income groups, especially in developing part of the world. To fill the gap in the financial system and provide products and services to the poorest, the idea of microfinance was born. The following sections discuss the notion of microfinance, the history of microfinance institutions’ development, and the characteristics of microfinance institutions.

3.1 The notion of microfinance and microcredit (microloan)

The concept of microfinance has its roots in the 18th-century but microfinance started to develop strongly in the last few decades dominantly in underdeveloped and developing countries. The oldest system of microcrediting and microcredit organizations, the predecessor of today’s microfinance institutions, the “Irish Loan Fund” system, was founded in Ireland based on the idea of Jonathan Swift. His idea of lending to poor residents without collateral was accepted very slowly, but in 1840 it became widespread throughout Ireland, with the formation of approximately 300 funds. Those funds were lent to approximately 20% of households in Ireland. The four basic components of Swift’s lending scheme were: small loans, weekly repayments, co-signers, but not physical collateral, and a lawsuit in case of inability to collect the loan [11].

The origin of the modern concept of microfinancing and the functioning of modern microcredit organizations is linked to the Grameen Bank from Bangladesh and its founder Muhamed Yunus. Yunus started the fight against poverty in 1974 during the great famine in Bangladesh. He discovered how very small loans (microcredits) can significantly improve the lives of the poorest. At that time, he started a research project on the economy in rural areas. His first loan was USD 27, which he lent out of his own funds to a woman who made bamboo furniture. At that time, traditional banks in Bangladesh were not interested in providing small loans to the poor because of the high risk of debt collection. However, Yunus believed that the poor would pay back their debts if given the chance and that the concept of microcredit could be turned into a profitable business model. The Norwegian Nobel Committee decided in 2006 to award the Nobel Peace Prize to the Grameen Bank from Bangladesh, as well as to its founder, for their efforts in achieving the economic and social empowerment of the poorest by providing the opportunity for a large number of poor people to start entrepreneurial activity through microcredit, which formally awarded the entire microcredit sector in the world for its success in reducing poverty. In the explanation of the Committee, it was pointed out that achieving long-term peace in the world cannot be achieved unless a large population of the poor finds a way to get out of the “circle” of poverty, and microcredit is one of those ways. The same was concluded by [12], “The key to ending extreme poverty is to enable the poorest of the poor to get their foot on the ladder of development. The ladder of development hovers overhead and the poorest of the poor are stuck beneath it. They lack the minimum amount of capital necessary to get a foothold, and therefore need a boost up to the first rung.” It was clear that new types of financial institutions with more sensibility toward the poor were needed to evolve.

Interestingly, at that time the concept of microfinance had been perceived as unsustainable by the WB and other international donors and financiers for many years. However, after several decades of successful work by the Grameen Bank, the leaders of the WB admitted that “microcredit programs have breathed energy into the market economy in the countryside and the poorest part of the population in the world. By approaching the fight against poverty from a market point of view, millions of people have been enabled to improve their position with dignity.” [13] Joseph Deiss, the Chairman of the General Assembly of the United Nations [14] said in his speech held at the annual assembly of the United Nations on October 13, 2010, that “microfinance is a key instrument for improving the living conditions of poor population.“ Recognizing microcredit as an effective means of fighting poverty, the WB established the Consultative Group to Assist the Poor (CGAP). CGAP today represents a consortium of over 30 public and private agencies working to improve access to financial services for the poor.

Microfinance is a concept developed from the concept of micro-crediting but in academic literature the term “microfinance” is often identified with the term “microcredit” (or “micro-crediting”), which is wrong. Namely, as already pointed out, Grameen Bank, the forerunner of today’s microcredit financial institutions, paved the way for the development of microfinance by approving microloans for the poor. With the development of the bank, i.e., by understanding the needs of the poor for various financial services, the bank’s activities expanded and, in addition to microcredit, the bank began to offer a wide range of financial services, from savings to money transfer services. So, microcredits represent only one of the financial products that are found in the wide range of offers of microcredit financial institutions that deal with microfinancing.

Microfinance is a set of different financial services (such as lending and savings), both conventional and digital, intended for those clients who do not have access to conventional financial/banking products and/or services. According to CGAP, microfinance, in a broad sense, refers to the provision/provision of financial services to poor and low-income clients who have limited or no access to conventional banks, while in a narrower sense, microfinance refers to institutions that use new techniques developed in the last 30 years to provide microcredits to informal entrepreneurs, where the range of services of these institutions includes savings, insurance services and money transfer services [15].

Microfinance services are intended for the poorest strata of society, but also for entrepreneurs and small and medium-sized enterprises that do not have the possibility to secure collateral when borrowing funds, do not have stable income, or do not have a credit history. The microfinance project proved to be a successful instrument in solving the financial problems of the low-income population in many parts of the world (e.g., India, Bangladesh, Latin American countries, Bosnia and Herzegovina, etc.).

Owing to the growth in financial technology aided by the widespread adoption of mobile and internet services across the world, the microfinance industry was able to establish a firm standing globally. The global market size for the microfinance industry is estimated to grow by USD 122.46 billion from 2021 to 2026 at a compound annual growth rate (CAGR) of 11.61%. The rapid adoption of technology has been one of the primary contributing factors to the growth of the microfinance sector. Moreover, global development agencies and several governments have been making concerted efforts to alleviate poverty by enabling financial inclusion products, such as micro-credits, to the underserved segment [16].

3.2 The microfinance sector and microcredit organizations

The drivers of the development of the microfinance sector are microcredit financial institutions/organizations. Microcredit organizations can be defined as non-deposit, non-profit, or for-profit organizations, whose main activity is providing microcredit to socially disadvantaged persons with the aim of developing micro-entrepreneurship. These are credit organizations that do not have the character of banks, nor are they established according to bank procedures.

Starting from the given definition, it is possible to distinguish two types of microcredit organizations:

non-profit microcredit organizations, which operate as non-governmental organizations (in B&H legislation they are called microcredit foundations), and

profit microcredit organizations, which have the status of a financial institution (in B&H legislation they are called microcredit companies).

The microcredit sector, as a rule, develops through the establishment of non-profit microcredit organizations, which grow into for-profit financial institutions through the development of the credit portfolio and expansion of the client base. For-profit microcredit organizations differ from non-profit ones in the way they are regulated, especially in terms of the sources of financing business activities.

For example, according to the Law on Microcredit Organizations of the Federation of B&H (Official Gazette of the Federation of B&H, No. 59/06), a microcredit organization is a non-depository financial organization whose main activity is the granting of microcredits. The microcredit organization performs microcredit activities with the aim of improving the financial position of microcredit users, increasing employment, providing support for the development of entrepreneurship and making a profit. In some countries, as in the case of B&A, microcredit organizations are under the jurisdiction of banking agencies, considering the activity of microcredit.

Microcredits are the most significant financial product that microcredit organizations provide to their clients. The amount of microcredit varies from country to country, as well as from the legal regulations that regulate the activity of microcredit organizations. In B&H, for example, microloans amount to 50,000 KM, which is equivalent to the amount of microloans in the EU of 25,000 EUR.

3.3 An overview of microfinance sector and its contribution toward financial inclusion in Bosnia and Herzegovina

Microcredit organizations in B&H began to develop in the post-war period from 1995 as part of programs implemented in this area with the aim of helping in employment and revitalization of economic activities through the marketing of microcredits. A large number of donors and financiers, primarily the WB, followed by other international organizations, made a significant contribution to the development of this sector by financing the operations of microcredit organizations. Microcredit organizations were created to fill the gap between commercial banks and humanitarian non-governmental institutions to support the development of small businesses and self-employment.

The microcredit sector of B&H has begun to play a significant role in reducing poverty and supporting the development of small and medium-sized entrepreneurship among the socially vulnerable population that does not have the possibility of obtaining financial resources from traditional/conventional banks. According to the Association of Microcredit Financial Institutions in B&H (AMFI) [17], the results achieved in the past 13 years included B&H among the countries with the highest development level in this domain of financial offer, which is often mixed with traditional banking, but the main difference is that the banks serve the wealthiest clients with credit history and collateral, while the microfinance i.e., microcredit organizations serve the clients who do not have collateral and have low income or no income whatsoever.

B&H microcredit organizations are among the leading microfinance institutions in the world, according to the level of transparency in business operations and financial reporting. Forbes’ list of the 50 most successful microcredit organizations for 2007 includes five microcredit organizations from B&H [18]. The microcredit sector is one of the few sectors of the B&H economy that has adopted and reached the world business standards that apply in this sector.

The most important microfinance law was adopted in 2006. According to this new regulation framework, former microcredit organizations (originally 35) had to transfer into either microcredit foundations or microcredit companies. According to the mentioned law, microcredit foundations are legally authorized to dispense individual microcredits up to 10,000 BAM in value (5.000 Euros) while microcredit companies are legally authorized to dispense individual microcredits up to 50,000 BAM in value (25.000 Euros). Both types of microcredit organizations are non-deposit-taking financial institutions.

According to the Financial Stability Report for 2021 issued by the Central Bank B&H [19], the operations of the microcredit sector in 2021 were marked by: asset growth, growth of gross loans, and capital increase, accompanied by the decreased value of delayed loans, and profitability growth. At the end of 2021, there were 26 microcredit organizations operating in B&H: 14 microcredit companies and 12 microcredit foundations. At the end of 2021, the total assets of the microcredit sector were higher by 7.8% compared to 2020, while loans increased by 8.2%. Out of the total microcredits amount, 97.4% was extended to individuals and households. The main sectors being financed are the agriculture sector (27.6%), followed by the financing of housing needs (17.4%) and the service sector (11.1%).

4. BH microfinance institutions initiatives for improving financial literacy: The case of digital financial literacy initiative: “Our classorom”

4.1 Initiative description and methodological framework for measuring the efficiency

Microfinance institutions in B&H developed individual approaches toward addressing client’s needs. The main reason for their success and the low percentage of non-performing loans is their ability to provide custom-made financial products/services as well as to support their clients in terms of financial education. During the COVID-19 pandemic, one of the biggest microcredit organizations in B&H, MI-BOSPO, organized a series of educations on digital financial literacy for their clients to help them to overcome obstacles posed by the lockdown.

MI-BOSPO became aware of the fact that their clients are exposed to waiting in long lines to complete the payments in commercial banks as well as of long commuting time spent on public transportation in order to pay their monthly loan installments. Sometimes, this waiting and commuting time could take several hours and could pose a health risk as well. This microfinance organization at that time had only one cashier in Tuzla where the microcredit installments could be paid, meaning that the majority of the clients paid installments through commercial banks. With the aim to motivate and support their clients (dominantly women) to use new digital technologies, such as online and mobile banking tools, to ease their business activities and support their family financial needs, MI-BOSPO has identified a need for a structured approach in the digital financial education. To that end, the initiative, called “Our Classroom” was launched in 2020 and 2021. The initiative was designed to raise the level of digital financial literacy among women, and increase the level of their knowledge and skills in digital banking tools, the types of digital services available, the reliability of the tools, and the simplicity and security of use. The main idea behind the initiatives was to assure the safety of their clients by eliminating waiting in long queues, and their health protection during the time of the pandemic, but also help their clients to overcome the prejudices such as internet safety, distrust, fear of something new and virtual, and present the advantages and possibilities given by this method of money transfer. The overall objective was to provide responsible financial services and increase the skills and knowledge of women clients on the use of digital banking tools.

“Our classroom” initiative included a series of tailored educational workshops on the following topics:

introduction to digital payment channels (electronic banking, mobile banking, credit cards, payment and withdrawal of money at the ATMs),

advantages and possibilities of internet and mobile tools, applications and services for money transfer and payments,

internet and mobile security and safety, and

raising the level of digital literacy, trust, and awareness.

Education was implemented by the independent consultant. To provide better outreach the clients, workshops were organized in 10 towns throughout the whole territory of B&H (Tuzla, Brčko, Bijeljina, Gradačac, Kalesija, Lukavac, Doboj, Zenica, Živinice, Srebrenik, Vlasenica, Banja Luka, Gračanica, Sarajevo, Zavidovići).

To follow the implementation as well as to capture the effects of educational workshops, the Faculty of Economics, University of Tuzla was commissioned to evaluate the level of digital financial literacy of MI-BOSPO clients and their need for education. The comprehensive methodology was developed in order to capture the effects of the initiative. To that end, protocols for collecting base-line and end-line data were developed. The following activities were performed:

preparation of survey methodology and questionnaires,

sample calculation of targeted survey participants,

data collection, and

data analysis.

For the purpose of understating the level of financial literacy, the incentive to use online banking and the effectiveness of the training in increasing digital financial inclusion, a base-line survey was conducted using the questionnaire prepared for this purpose.

The sample included clients of the microcredit organization MI-BOSPO. The basic sociodemographic features of the respondents are given in Table 1, while the geographical distribution sample is given in Appendix I.

Sociodemographic characteristics

Frequency

Percentage

The middle

Rural

157

65.1

Urban

84

34.9

Total

241

100.0

Residence

FBiH

132

55.0

RS

104

43.2

Brčko district

4

1.7

Total

240

100.0

Marital status

Unmarried

16

6.7

Married

181

75.4

Divorced

21

8.7

Widow

22

9.2

Total

240

100.0

Education

Unfinished elementary school

1

0.4

Finished elementary school

47

19.5

Medium professional qualifications

179

74.3

Tall professional qualifications

3

1.2

Master’s degree

10

4.1

Doctorate

1

0.4

Total

241

100.0

Primary source of income

Pensioner

20

8.3

Self-employed

168

69.7

Employed

39

16.2

Second

14

5.8

Total

241

100.0

Income level per households

less than 500 BAM

14

7.1

501 BAM - 1000 BAM

49

24.7

1001 BAM - 1500 BAM

43

21.7

1501 BAM - 2000 BAM

42

21.2

2001 BAM - 2500 BAM

28

14.1

over 2500 BAM

22

11.1

Total

198

100.0

Income from registered business

less than 500 BAM

57

28.6

501 BAM - 1000 BAM

69

34.7

1001 BAM - 1500 BAM

26

13.1

1501 BAM - 2000 BAM

20

10.1

2001 BAM - 2500 BAM

13

6.5

over 2500 BAM

14

7.0

Total

199

100.0

Access to Internet

Yes

225

94.1

no

14

5.9

Total

241

100.0

Table 1.

Sociodemographic characteristics of respondents.

Source: Authors’ calculations.

The average size of households was 3.72 with a standard deviation of 1.42. At least one household had only one member, and the largest of them had even 9. An average number of people included in the business is 2.44 with a standard deviation of 1.71. At least one household only had one member, and the largest them even 15. When it comes to the type of business, mostly the respondent stated that are working in the agriculture sector (40.2%), trade (21.6%), services (32.8%), and production (5.0%) sectors.

At the end of the project, the end-line survey was conducted among the clients who attended education. In total 66 responses were collected in the endline-survey which was sufficient enough to draw conclusions on the efficiency of the initiative.

The following sections provide the analysis of the data collected through base-line and end-line survey.

4.2 Understanding of the current usage level of digital banking products/services

In this section, the research results related to understanding the current usage level of digital products/services by the MI-BOSPO clients are presented. The focus is given to better understanding of the current practices of using financial products in general, both for personal and business use, as well as of the use of Internet and mobile banking services for personal and business needs with the aim to understand the reasons for poor usage of online banking services.

4.2.1 Use of financial products and services for personal and household needs

The frequency of usage of financial product and service for personal and/or needs households are given in Table 2.

Characteristics

Frequency

Percentage

Having the opened bank account

yes

197

83.1

no

40

16.9

Total

241

100.0

The bank where the account is open

NLB Bank

38

0.20

New bank

27

0.14

Raiffeisen bank

20

0.10

Sberbank

20

0.10

Unicredit bank

20

0.10

Other banks

69

35.6

Total

194

100.0

Knowledge on whether local community stores accept payment cards

yes

166

69.5

no

40

16.7

I do not know

33

13.8

Total

239

100.0

The main way of receiving salary

In cash

146

61.3

Through the bank account

74

31.1

In the last 6 months did not receive any income

18

7.6

Total

238

100.0

Table 2.

Usage of financial products and services for personal and needs households.

Source: Authors’ own research.

With further analysis of the use of financial services, it was detected that from the total number of respondents, 37 of them (25.9%), who receive salary in cash, transfer this salary to a bank account, while 106 respondents (74.1%) do not transfer their salary on to the bank account. On the other hand, the respondents who receive their salaries through the bank account, in 15 cases (20,3%) withdraw the money from the bank account, while 59 respondents (79,7%) do not withdraw the money.

Additionally, the analysis of the payment habits was conducted where respondents were asked to answer which types of payment are using to pay for their bills. The results are provided in the following Table 3.

The payment methods

Frequency

Percentage

Cash payments

yes

233

98.7

no

3

1.3

Total

236

100.0

From their bank accounts

yes

67

28.3

no

170

71.7

Total

237

100.0

Using mobile application

yes

19

8.1

no

217

91.95

Total

236

100.0

Using computer

yes

10

4.3

no

225

95.7

Total

235

100.0

Table 3.

The payment methods.

Source: Authors’ own research.

When it comes to payment methods, it can be observed that the respondents mainly pay cash, which shows that the respondents are not utilizing the opportunities of faster payment methods such as online payments through mobile applications and Internet banking.

With respect to the business needs of respondents, only 26 of them (11.7%) declared that for the purposes of their own business, they have contracted services of Internet and mobile banking in some of the banks. Big majority of respondents, 197 of them, (88.3%) claim that do not these services for personal use.

4.2.2 Use of internet and mobile banking services for personal and business needs

The majority of respondents (89.9%), declared owning some devices, such as tablets, smart telephones, and computers for personal use. However, as many as 196 of the respondents, or 82.7%, claim that they do not use the Internet and/or mobile banking for their own personal needs and/or for the needs of their own households.

The respondents who confirmed their usage of Internet and mobile banking services for personal use, provided more in-depth information on the purposes of using online banking services. The most commonly used services Internet and/or mobile banking for personal needs and/or needs of households are given in Table 4.

Type of Internet and mobile banking services used

Frequency

Percentage

Domestic payments - payment direction and others species accounts

Yes

30

71.4

No

12

28.6

Total

42

100.0

Funds transfer on to personal and business accounts

Yes

17

40.5

No

25

59.5

Total

42

100.0

Funds transfer between own accounts

Yes

11

26.2

No

31

73.8

Total

42

100.0

Currency conversion

Yes

4

9.5

No

38

90.5

Total

42

100.0

Checking the account balance, transaction and credit card debts

Yes

35

83.3

No

7

16.7

Total

42

100.0

Overview of all orders, their status, and others information

Yes

28

66.7

No

14

33.3

Total

42

100.0

Overview of exchange rates/exchange rates lists

Yes

4

9.5

No

38

90.5

Total

42

100.0

Overview of useful contacts in the Bank

Yes

10

23.8

No

32

76.2

Total

42

100.0

Table 4.

The most commonly used services Internet and/or mobile banking for personal needs and/or needs households.

Source: Authors’ own research.

In respect to the use of Internet and mobile banking services for business needs, 110 respondents (48.2%) declared that for the purposes of their own business have some type of electronic device, such as a tablet, smartphone, or computer. However, the majority of them (89.4%) claim that they do not use the Internet and/or mobile banking for business needs. Only 24 respondents, or 10.6% of them declared some of the services of Internet and/or mobile banking for business purposes.

An overview of the most commonly used service for business purposes is given in the Table 5.

Type of Internet and mobile banking services used

Frequency

Percentage

Domestic payment – utility bills and other invoices payment

Yes

20

83.3

No

4

16.7

Total

24

100.0

Foreign payments

Yes

2

8–7

No

21

91.3

Total

23

100.0

Funds transfer between own accounts

Yes

12

54.5

No

10

45.5

Total

22

100.0

Currency conversion

Yes

3

14.3

No

18

85.7

Total

21

100.0

Two-way communication with the bank

Yes

6

27.3

No

16

72.7

Total

22

100.0

Products notice and services banks and special benefits and actions for client’s banks

Yes

12

54.5

No

10

45.5

Total

22

100.0

Account balance and transactions overview

Yes

21

95.5

No

1

4.5

Total

22

100.0

Payment obligation way paid order

Yes

16

72.7

No

6

27.3

Total

22

100.0

Bank statements and payment orders generation and overview

Yes

15

86.4

No

7

13.6

Total

22

100.0

Overview of all orders, their status and other information

Yes

19

86.4

No

3

13.6

Total

22

100.0

Overview of exchange rates/exchange rates lists

Yes

4

18.2

No

18

81.8

Total

22

100.0

Overview of the useful contacts in the Bank

Yes

6

27.3

No

16

72.7

Total

22

100.0

Table 5.

The most commonly used services of Internet and/or mobile banking for business purposes.

Source: Authors’ own research.

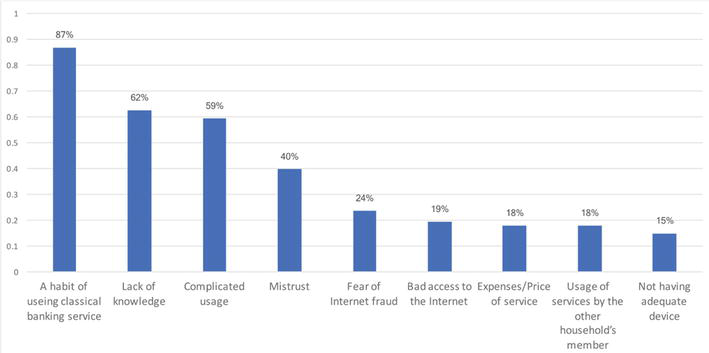

The main reasons for poor usage of Internet and mobile banking are presented in Figure 1.

Figure 1.

Reasons for insufficient usage of Internet and mobile banking services. Source: Authors’ own research.

Based on the data presented in the previous figure, it can be concluded that the most important barriers to the usage of Internet and mobile banking services are the habit of using classical banking services, lack of knowledge, complicated use, mistrust, and fear of Internet fraud.

4.3 Knowledge regarding the use of Internet and mobile banking services and willingness to participate in education

Assuming that the survey participants do not have adequate knowledge of the use of Internet and mobile banking services, one of the research goals was to establish the level of relevant knowledge on basic financial concepts. For that purpose, a questionnaire consisting of 14 statements was created. The results given in Table 6 enables a better insight into the knowledge of respondent in regard to the usage of Internet and mobile services banking.

Statement

Frequency

Percentage

Internet and/or mobile services can be used to check the account balance and payments from and to bank account

True

157

66.8

False

5

2.1

I do not know

73

31.1

Total

235

100.0

Internet and/or mobile services can be used for debt balance overview, overdue and unpaid installments, interests, costs, and limits on credit and debit cards.

True

122

51.9

False

5

2.1

I do not know

108

46.0

Total

235

100.0

Internet and/or mobile services can be used for utility bills and other bill payments

True

195

83.0

False

1

0.4

I do not know

39

16.6

Total

235

100.0

Internet and/or mobile services can be used for payment of utility bills using the option to take of photo of the bill which will automatically translated into the payment request

True

78

33.3

False

10

4.3

I do not know

146

62.4

Total

234

100.0

Internet and/or mobile services can be used for currency conversion

True

44

18.8

False

12

5.1

I do not know

178

76.1

Total

234

100.0

Internet and/or mobile services can be used to review payments

True

151

64.5

False

5

2.1

I do not know

78

33.3

Total

234

100.0

Internet and/or mobile services can be used to create templets of payment instructions for future faster payment

True

88

37.6

False

4

1.7

I do not know

242

60.7

Total

234

100.0

Internet and/or mobile services can have an option to set the future date for the payment

True

34

14.6

False

15

6.4

I do not know

184

79.0

Total

233

100.0

Internet and/or mobile services can be used for utility bill subscriptions by using e-payments

True

49

20.9

False

9

3.8

I do not know

176

75.2

Total

234

100.0

Internet and/or mobile services can be used to get information about the Bank

True

116

49.8

False

3

1.3

I do not know

114

48.9

Total

233

100.0

Internet and/or mobile services can be used to find the closest ATM or branch office

True

121

51.7

False

3

1.3

I do not know

110

47.0

Total

234

100.0

Internet and/or mobile services can be used for payment of public taxes

True

91

38.9

False

8

3.4

I do not know

135

57.7

Total

234

100.0

Internet and/or mobile services can be used for bank statement withdrawal Internet and/or mobile services can be used for bank statement withdrawal

True

89

38.0

False

10

4.3

I do not know

135

57.7

Total

234

100.0

Internet and/or mobile services can be used for bank statement withdrawal

True

57

24.4

False

12

5.1

I do not know

165

70.5

Total

241

100.0

Table 6.

Relationship knowledge – use Internet service and mobile banking.

Source: Authors’ own research.

As it can be observed from the previous table, the most dominant answer to all statements is “I don’t know” if the statement is true or not. This means that respondents lacked knowledge of basic financial concepts.

Combining the results of the reasons for the poor usage of Internet and mobile banking services with the understating of basic financial concepts, it was clear that more education is needed in order to break down the circle of fear of using online banking services. 65 respondents (27.3%), expressed their willingness to participate in education in which they would gain more theoretical and practical knowledge about Internet and mobile banking. Most of the respondents, i.e., 173 of them, or 72.7%, did not express this willingness. The majority of the respondents, 158, or 66.4%, believe that their use of Internet and mobile banking would not change significantly, despite the acquisition of more theoretical and practical knowledge, while 80 respondents, or 33.6%, believed that they would use the Internet and mobile banking more if they gained more theoretical and practical knowledge about it.

4.4 Effects of “our classroom” initiative toward improving knowledge and usage practices of Internet/mobile banking

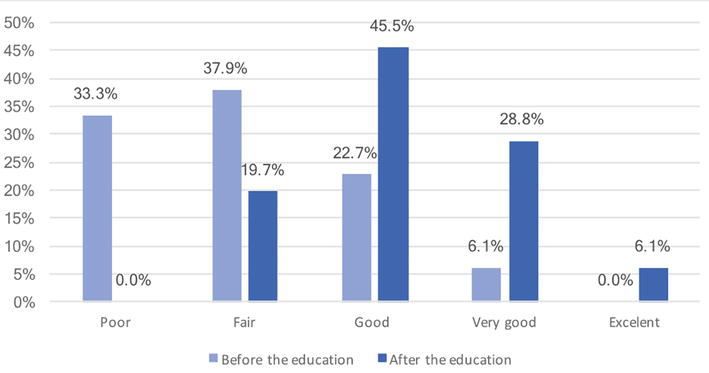

The results of knowledge self-assessment with respect to usage of Internet and/or mobile banking services after the education within “Our classroom” are presented in Figure 2.

Figure 2.

Knowledge self-assessment with respect to usage of Internet and/or mobile banking services. Source: Authors’ own research.

As it can be observed, participation in education improved the level of self-assessed knowledge with respect to the usage of the Internet and/or mobile banking services. Prior to the education, the majority of respondent assessed their knowledge as poor (33,3%) or fair (37,9%), while after the education it can be observed that the level of knowledge significantly increased. More than 45% of respondents assessed their knowledge as good, 28,8% as very good, and 6,1% as excellent. It can be concluded that education improved the self-assessed knowledge among participants since none of the respondents assessed their knowledge as poor after the completion of the education.

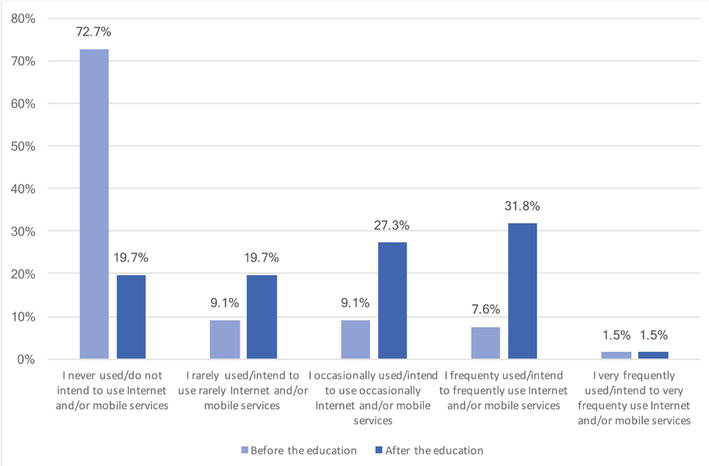

Self-assessment of the level of Internet and/or mobile services usage prior to education in contrast to after the education is presented in Figure 3.

Figure 3.

Self-assessment of Internet and/or mobile services usage frequency. Source: Authors’ own research.

Based on the self-assessment of Internet and/or mobile services usage frequency before and after education, it can be concluded that education had a positive impact on the intention to use online banking services. While more than 72% of the respondents reported that never used Internet and/or mobile services prior to education, only 19,7% of them reported that they do not intend to use it in the future. On the other hand, 27,3% of respondents declared the intention to use the service occasionally, and 31,8% of them that they will use the Internet and/or mobile services frequently.

In order to gain a more in-depth understanding of the knowledge increase after the education, respondents were asked to answer whether some statements regarding the usage of Internet and mobile services are correct. The results of this assessment are given in Table 7.

Statement

True (%)

False (%)

I do not know (%)

I am more confident and have less fear with respect to Internet payment after the education

81

9

9

I completed at least one transaction using the Internet or mobile banking services after the education

32

68

0

As a result of the education I know how to check my account balance using online banking

45

55

0

As a result of the education I know how to file a request for online banking services

44

47

9

Internet and/or mobile services can be used for payment of utility and other bills

100

0

0

Internet and/or mobile services can be used for payment of utility bills using the option to take of photo of the bill which will automatically translated into the payment request

94

0

6

Internet and/or mobile services can be used for currency conversion

77

0

23

Internet and/or mobile services can be used for an overview of completed payments

89

0

11

Internet and/or mobile services have the option to create templets of payment instructions for future faster payment

91

0

9

Internet and/or mobile services can have an option to set the future date for the payment

80

0

20

Internet and/or mobile services can be used for utility bill subscriptions by using e-payments

85

0

15

Internet and/or mobile services can be used to obtain information about the bank

98

0

2

Internet and/or mobile services can be used to find the closest ATM or branch office

97

0

3

Internet and/or mobile services can be used for payment of public taxes

79

0

21

Internet and/or mobile services can be used for bank statement withdrawal

88

0

12

Internet and/or mobile services can be used for foreign payments

88

0

12

Table 7.

Attitudes and knowledge toward using Internet and/or mobile services after education.

Source: Authors’ own research.

Based on the results presented in the previous table, it can be concluded that participation in education contributed toward a better understanding of the basic financial concepts among participants. The majority of responders answered correctly to the proposed statements, while the percentage of the answer “I don’t know” is in a range from 2 to 23%.

It has to be emphasized that participation in education also contributed toward the increase of the confidence and trust among participants to use the Internet and/or mobile services. More than 81% of respondents confirmed that their trust and confidence were increased as a result of education.

Digital transformation as the concept of digital technology use in business practices, is profoundly integrated in today’s everyday life. The need for digital transformation was even more obvious during the COVID-19 pandemic. As a result of the lockdown, most of the day-to-day activities and business operations were transferred into the online world. The financial sector, like any other service sector, had to adapt and offer their clients products and services that are available online and do not require that client has to come to the bank or any other financial institution.

During the lockdown period, many financial institutions in B&H faced the problem of reaching their clients and adequately addressing their needs, despite the fact that most of the financial institutions initiated digital transformation of their businesses and were already offering Internet and mobile services to their clients.

Needs assessment conducted by MI-BOSPO provided an insight into their clients’ level of usage of Internet and mobile banking services, level of knowledge (financial literacy), and confirmed the need and readiness of their clients to participate in education to increase their level of financial literacy and improve their habits of using the Internet and mobile banking service. As a result of the needs assessment among MI-BOSPO clients, “Our classroom” initiative was introduced. The initiative envisaged the organization of tailored education workshops, based on the needs assessment research conducted prior to workshop organization, where clients would gain a better understanding of the key financial concepts and practical aspects of using the Internet and mobile banking.

As a result of “Our classroom” initiative, valuable insights into financial inclusion and literacy were gained. An interesting finding is that there are around 19% of clients do not have bank accounts which is the primary indicator of financial inclusion. The clients are mostly receiving cash payments which further dissimulated them to have bank accounts. Those who own a bank account rarely use Internet and mobile banking services. Only 14,5% of clients use these services for personal affairs, while just 10% for business purposes, proving that digital financial inclusion is even lower than the overall financial inclusion measured by bank account ownership. The research conducted prior to workshops provided an insight into a better understanding of the low digital financial inclusion through a better understating of the factors contributing to poor usage of Internet and mobile banking services. The research showed that the main reasons for avoiding online banking services are (1) the habit of using classical banking services, (2) lack of knowledge, (3) complicated use, (4) mistrust and (5) fear of Internet fraud. Besides the habit of using classical banking services, all other four barriers to using online banking are related to poor financial literacy. More in-depth analysis showed that the majority of clients did not have knowledge of the basic financial concepts.

“Our classroom” initiative resulted in the positive change toward increase of (digital) financial literacy and (digital) financial inclusion. Endline research showed that initiative contributed toward:

improvement of the level of self-assessed knowledge with respect to usage of Internet and/or mobile banking services, since none of the respondents assessed their knowledge as poor after the completion of the education. More than 45% of respondents assessed their knowledge as good, 28.8% as very good, and 6.1% as excellent.

increased intention to use online banking services among clients. While more than 72% of the respondents reported that never used Internet and/or mobile services prior to education, only 19.7% of them reported that do not intend to use it in the future. 27.3% of respondents declared that they have the intention to use the service occasionally, and 31.8% of them that they will use the Internet and/or mobile services frequently.

a better understanding of the basic financial concepts among participants. The majority of responders answered correctly to the proposed statements, while the percentage of the answer “I don’t know” is in a range from 2 to 23%.

increase of the confidence and trust among participants to use the Internet and/or mobile services. More than 81% of respondents confirmed that their trust and confidence were increased as a result of education.

Authors would like to express their gratitude toward the microcredit foundation MI-BOSPO from Tuzla, Bosnia and Herzegovina for initiating the “Our classroom” initiative and recognizing the importance of the scientific approach toward measuring the effects of these efforts. The authors would like to thank personally to Mr. Safet Husić, CEO at MI-BOSPO, Ms. Azra Berilo, HR manager at MI-BOSPO and Ms. Dragana Lukić, marketing manager at MI-BOSPO.

1.World Bank. UFA2020 Overview: Universal Financial Access by 2020. World Bank. 2018. Available from: https://www.worldbank.org/en/topic/financialinclusion/brief/achieving-universal-financial-access-by-2020 [Accessed: August 22, 2023]

2.Demirgüç-Kunt A, Klapper L, Singer D, Ansar ST. Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19. Washington, DC: World Bank; 2022. DOI: 10.1596/978-1-4648-1897-4

3.Grohmann A, Klühs T, Menkhoff L. Does financial literacy improve financial inclusion? Cross country evidence (September 2017). DIW Berlin Discussion Paper No. 1682. 2017. 10.2139/ssrn.3034178

4.Leyshon A, Thrift N. Financial exclusion and the shifting boundaries of the Financial system. Environment and Planning A: Economy and Space. 1996;28(7):1150-1156. DOI: 10.1068/a281150

5.Sinclair PS. Financial Exclusion: An Introductory Survey. Edinburgh: Centre for Research in Socially Inclusive Services (CRISIS), Heriot-Watt University; 2021

6.World Bank. Overview. World Bank [Internet]. 2022. Available from: https://www.worldbank.org/en/topic/financialinclusion/ [Accessed: August 22, 2023]

7.World Bank. Digital financial inclusion. World Bank. 2022. Available from: https://www.worldbank.org/en/topic/financialinclusion/publication/digital-financial-inclusion [Accessed: August 22, 2023]

8.Lauer K, Lyman T. Digital Financial inclusion: Implications for customers, regulators, supervisors, and standard-setting bodies. In: Consultative Group to Assist the Poor (CGAP) Brief; Consultative Group to Assist the Poor (CGAP). Washington, DC, USA; 2015

9.Anakpo G, Xhate Z, Mishi S. The policies, practices, and challenges of digital Financial inclusion for sustainable development: The case of the developing economy. FinTech. 2023;2(2):327-343. DOI: 10.3390/fintech2020019

10.Lusardi A, Mitchell OS. The importance of financial literacy: Opening a new field. NBER Working Papers 31145. National Bureau of Economic Research, Inc. 2023

11.Hollis A, Sweetman AC. Competition and institutional development: The Irish loan funds through three centuries. Economic History. 1997;1997:9704003

12.Sachs J. The End of Poverty: How We Can Make It Happen in Our Lifetime. UK: Penguin; 2005

13.Yunus M, Jolis A. Banker to the Poor: micro-Lending and the Battle against World Poverty. New York, NY: Public Affairs; 2003

14.Dreiss J. Statement of H.E. Mr. Joseph Deiss, President of the 65th Session of the General Assembly, at the 29th Plenary Meeting: Follow-up to the International Year of Microcredit. 2010. Available from: https://www.un.org/en/ga/president/65/pdf/statements/20101013-microcredit.pdf [Accessed: August 10, 2023]

15.Rosenberg R, Gonzalez A, Narain S. The new moneylenders: Are the poor being exploited by high microcredit interest rates?. Occasional Paper, No. 15. 2009. Available from: https://www.cgap.org/sites/default/files/CGAP-Occasional-Paper-The-New-Moneylenders-Are-the-Poor-Being-Exploited-by-High-Microcredit-Interest-Rates-Feb-2009.pdf [Accessed: June 24, 2023]

16.PwC. Next-gen microfinance: The role of digital technology [Internet]. 2023. Available from: https://www.pwc.in/assets/pdfs/consulting/financial-services/fintech/publications/next-gen-microfinance-the-role-of-digital-technology.pdf [Accessed: July 23, 2023]

17.AMFI. About us [Internet]. 2023. Available from: https://amfi.ba/en/about-us/ [Accessed: July 20, 2023]

18.Forbes. The 50 Top Microfinance Institutions [Internet]. 2007. Available from: https://www.forbes.com/2007/12/20/microfinance-philanthropy-credit-biz-cz_ms_1220microfinance_table.html?sh=7ca2e295b292 [Accessed: August 04, 2023]

19.CBBiH. Financial stability report for 2021 [Internet]. 2023. Central bank of Bosnia and Herzegovina. 2023. Available from: https://www.cbbh.ba/Content/Archive/575 [Accessed: July 20, 2023]

Written By

Jasmina Okičić and Meldina Kokorović Jukan

Submitted: 01 September 2023Reviewed: 02 September 2023Published: 04 October 2023