Open Access is an initiative that aims to make scientific research freely available to all. To date our community has made over 100 million downloads. It’s based on principles of collaboration, unobstructed discovery, and, most importantly, scientific progression. As PhD students, we found it difficult to access the research we needed, so we decided to create a new Open Access publisher that levels the playing field for scientists across the world. How? By making research easy to access, and puts the academic needs of the researchers before the business interests of publishers.

We are a community of more than 103,000 authors and editors from 3,291 institutions spanning 160 countries, including Nobel Prize winners and some of the world’s most-cited researchers. Publishing on IntechOpen allows authors to earn citations and find new collaborators, meaning more people see your work not only from your own field of study, but from other related fields too.

Steel manufacture is a carbon and energy intensive process that, globally, on average, emits 1.9 tonnes of carbon-dioxide (CO2) and uses 5.17 MWh of primary energy per ton produced, accounting for 9% of 11 human CO2 emissions. The structure of the world’s steel production must fundamentally change if the Paris Agreement’s objectives of keeping global temperature increase below 1.5°C from preindustrial levels are to be met. There are a number of technological avenues leading to a lower carbon intensity for steelmaking, which bring with them a paradigm shifts decoupling CO2 emissions from crude steel production by moving away from traditional methods of steel production using fossil coal and fossil methane and toward those based on reasonably priced renewable electricity and green hydrogen. The effects of fully defossilized steelmaking have not yet been thoroughly studied with regard to the energy system. A Gross Domestic Product (GDP)—based demand model for global steel demands, which forecasts an increase in steel demand from 1.6 Gt in 2020 to 2.4 Gt in 2100, is used in this study to investigate the energy system requirements of a global defossilized power-to-steel sector.

Department of Industrial Engineering and Management, JSS Academy of Technical Education, Bengaluru, Karnataka, India

M. Vijay Kumar*

Department of Industrial Engineering and Management, JSS Academy of Technical Education, Bengaluru, Karnataka, India

*Address all correspondence to: mvkjss@gmail.com

1. Introduction

Iron is created by removing oxygen and other impurities from iron ore. Iron is combined with carbon, recycled steel, and small amounts of other elements to form steel. Steel is the most significant material utilized in engineering and construction globally. It is utilized in every aspect of our lives, including automobiles, construction materials, washing machines, cargo ships, and surgical scalpels [1].

In the yearly World Steel in Figures book, which is released in early June, world steel updates the list of nations that produce steel. The Steel Statistical Yearbook, which is published in November/December, may make additional changes to the ranking. Via the Steel Data Viewer, world steel publishes monthly statistics on country steel output for both the current and prior year [1].

The yearly World Steel in Figures book from world steel includes an updated list of significant steel-producing firms. Below 913°C (1,675°F) and between 1395°C (2,543°F) and its melting point of 1539°C (2,802°F), iron has a bcc allotropy. Iron in its bcc structure is referred to as ferrite, but it is also known as alpha iron at low temperatures and delta iron at high temperatures. Iron is in its fcc order between 913 and 1395°C, also known as austenite or gamma iron. With very few exceptions, steel retains iron’s allotropic characteristic even when the alloy contains sizable amounts of other elements (Britannica Technology).

For many years, steel’s usage in recent years has significantly expanded. For instance, between 1950 and 2018, the yearly global production of crude steel (CS) climbed from 201 megatons (Mt) to 1805 MtCS [1]. Despite a 60% drop in energy intensity over the past 50 years, one tonne of steel still requires an average of 5.18 MWhth of primary energy to create.

One of austenitic stainless steel’s most significant qualities is its good weldability. These steels have more broad applications now than other stainless steels do as a result. The main industries for these applications are petrochemical, high pressure storage, and chemical storage tanks. The chemical composition, mechanical properties, and especially toughness of the welds in austenitic stainless steels are often comparable to those of the base metals. These steels do not break easily in the cold. These steels typically do not require pre-heating or post-weld heating because of the stable structure of austenite.

Cast iron (1.8–4.4% carbon) is created when iron starts to absorb carbon at extremely high temperatures, lowering the MP of the metal. Iron production grew with the development of blast furnaces, which were originally employed by the Chinese in the 6th century – B.C. but were utilized in Europe during the Middle Ages. Liquid iron that has been cooled in the main chamber is known as pig iron. The enormous central ingot and the tinier, encircling ingots looked like a sow and her calves. Due to its high carbon content, cast iron is strong but brittle, making it difficult to work with and shape. Once metallurgists learned that the brittleness of iron was mostly caused by its high carbon content, they experimented with novel ways to lower the carbon level and make iron more feasible. By the late 18th century, ironworkers had mastered the use of puddling furnaces to convert pig iron into wrought iron (developed by Henry Cort in 1784). Puddlers had to stir the molten iron with long, oar-shaped implements as the furnaces heated them, allowing oxygen to react with and gradually remove carbon. Iron’s melting point rises as carbon content falls, causing masses of iron to clump together in the boiler. The puddler would take these masses out and shape them into sheets or rails using a forge hammer. Although Britain had over 3000 puddling furnaces by 1860, the process was still hindered by the need for a lot of manpower and fuel. Blister steel is one of the oldest types of steel. In this procedure, heated stone boxes contained wrought iron bars coated with charcoal powder. The iron would eventually absorb the carbon from the charcoal after about a week. Blister steel was produced after repeated heating because the carbon was distributed more uniformly. Because blister steel had a larger carbon content than pig iron, it was considerably easier to press or roll. English clockmaker Benjamin Huntsman learned that high-quality steel could be produced for his clock springs by melting the metal in clay crucibles and then polishing it with a specific flux to eliminate cementation slag. The 1740s saw a development in blister steel production as a result of this discovery. The result was a steel crucible, or cast. However, blister or cast steel has only ever been employed in specific applications due to the high cost of production. As a result, cast iron produced in puddling furnaces continued to be used as the primary structural metal in industrializing Britain for the bulk of the 19th century [2].

2.1 The Bessemer process and modern steelmaking

The iron industry, which still suffered from ineffective manufacturing methods, was under tremendous pressure from the expansion of railroads during the 19th century in both Europe and America. Steel manufacture was slow and expensive, and it had not yet been demonstrated to be a reliable structural metal. That is, until Henry Bessemer discovered a more efficient way to add oxygen to molten iron in 1856, lowering the carbon level. Bessemer created a pear-shaped container, or “converter,” in which iron could be heated and oxygen could be blown through the molten metal, leading to the development of what is now known as the Bessemer Process. The molten metal would react with the carbon when oxygen traveled through it, releasing carbon dioxide and creating a more pure iron. The method, which removed silicon and carbon from iron for a low cost and in a short amount of time, suffered from being too effective. In the finished product, too much oxygen predominated and too much carbon was eliminated. In the end, Bessemer had to pay back his investors while he looked for a way to raise the carbon content and remove the excess oxygen. A similar period saw the acquisition and testing of spiegeleisen, a mixture of iron, carbon, and manganese, by British metallurgist Robert Mushet. The carbon content in the spiegeleisen, if added in the correct amounts, would give the solution to Bessemer’s issues because manganese was known to remove oxygen from molten iron. With tremendous success, Bessemer started using it into his conversion procedure. One issue persisted. Bessemer had been unable to eliminate phosphorus from his final product phosphorus, a harmful contaminant that renders steel brittle. Only phosphorus-free ore from Sweden and Wales could be applied as a result. Sidney Gilchrist Thomas, a Welshman, discovered the remedy in 1876 by incorporating limestone, a chemically basic flux, into the Bessemer process. The undesirable element was removed because the limestone pulled phosphorus from the pig iron into the slag. With this invention, steel could then be produced from iron ore from anywhere in the world. It should come as no surprise that steel production costs started to drop considerably. Because of the new methods for producing steel, the cost of steel rail decreased by more than 80% between 1867 and 1884, sparking the expansion of the global steel industry [2].

2.2 Birth of the steel industry

A number of businessmen at the time identified an investment opportunity in the revolution in steel production, which resulted in the manufacture of cheaper, higher-quality material. Investors in the steel industry in the late 19th century made millions of dollars—in Carnegie’s case, billions—during that time, including Charles Schwab and Andrew Carnegie. US Steel Corporation, founded by Carnegie, was the 1st business to be valued at over $1 billion.

2.3 Electric arc furnace(EAF) steelmaking

Another event that would have a significant impact on the growth of steel production happened shortly after the turn of the century. Paul Heroult created the electric arc boiler to exothermically oxidize charged material at temperatures as high as 3272°F (1800°C), which is more than enough to heat steel manufacture. EAFs were firstly utilized for the production of specialty steels. Particularly in the case of carbon steels or long products, they were able to compete with the large American companies like US Steel Corp. and Bethlehem Steel because to the low investment costs associated with building up EAF mills. Less energy is required per unit of production for EAFs since steel can be made entirely from scrap or cold ferrous feed. Operations can be interrupted and started with low related expenses, in contrast to simple oxygen hearths. Because of these factors, the amount of steel produced using EAFs has been rising continuously for more than 50 years and today makes up roughly 33% of the world’s total steel production [3].

2.4 Oxygen steelmaking

Currently, basic oxygen facilities create around 66% of the world’s steel. Small oxygen furnaces can blow oxygen into vast quantities of liquid iron and waste steel, which makes them faster at charging than open-hearth operations. Large vessels with a capacity of up to 350 metric tons of iron may convert iron to steel in less than an hour. Open-hearth factories started to close after oxygen steelmaking was introduced in the 1960s because it was more affordable and made them less competitive. It shut down in 1992 both in the US and in China in 2001.

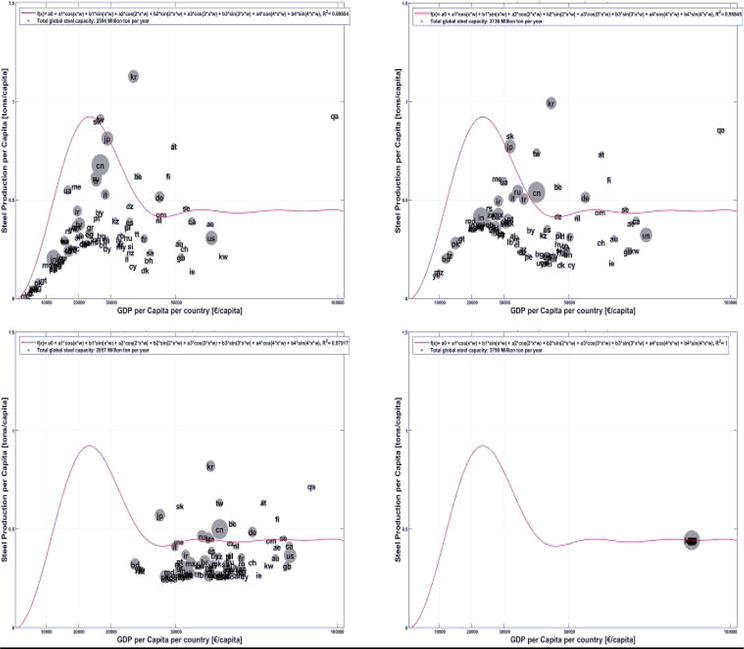

According to the GDP and population growth forecasts made by Toktarova et al. [4], the world’s steel output continues to rise at its current rate until 2030 (Figure 1 up left), when it slows down and achieves a maximum of 2336 Mt. (Figure 1 up right). Every 10 years, 10% of the vertical space between each point in Figure 1‘s points and the curve is closed. When low-income nations develop as projected but slowly, global steel production rises progressively starting in 2060 (Figure 1 below left), achieving steady-state steel production per person by 2100 and overall production of 2418 Mt. in 2100. (Figure 1 below right) [3].

Figure 1.

Proportion of per-capita steel output over per-capita GDP in 2030-up left, 2040- up right, 2060-below left and 2100-below right.

As shown in Table 1, the production of latest steel (primary steel) rises gradually till 2040, when it is anticipated to reach a level of around 1.5 GtCS, before dropping precipitously from 2040 to 2060 and stabilizing at about 0.3 Gt in 2100. The percentage of recycled steel overtakes the percentage of new steel starting in 2060 and stabilizes at 89.1% in 2100. Steel recycling, which now averages 80.6% globally, might climb to 88.1% if actions were taken internationally to promote global recycling across sectors without improvements in sectors with low recycling rates.

Empty cell

2015

2020

2030

2040

2050

2060

2070

2080

2090

2100

Total steel (GtCS)

1.61

1.72

2.06

2.35

2.13

2.05

2.12

2.23

2.33

2.41

Primary steel (GtCS)

1.22

1.24

1.38

1.54

1.18

0.83

0.72

0.52

0.51

0.28

SecondarySteel (GtCS)

0.41

0.49

0.67

0.80

0.96

1.23

1.40

1.71

1.82

2.15

Primary steel

74.4

71.6

67.3

65.5

55.6

40.5

34.2

23.5

22.2

11.1

Recycled steel

25.4

28.4

32.7

34.5

44.6

59.3

65.8

76.5

77.8

89.1

Table 1.

Production estimates for primary and secondary steel in absolute terms and in relation to overall production through the year 2100.

3.2 Future energy demand and carbon intensity for steel production

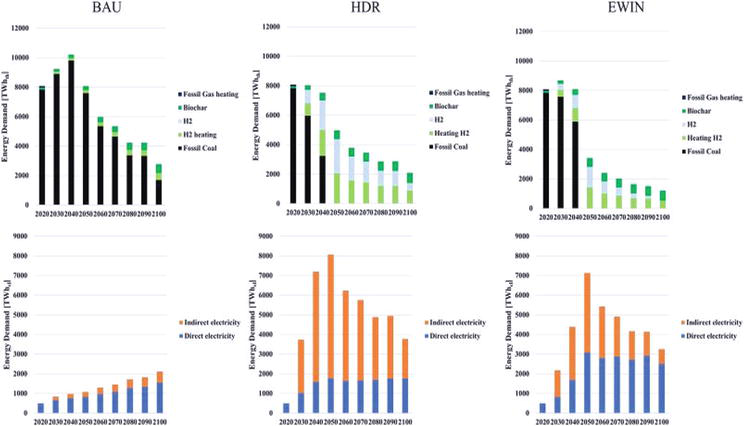

Figures 2 and 3 display the worldwide thermal and electrical energy requirements for the three scenarios’ steel production. In all cases, recycling steel in an EAF boiler has the biggest influence on the energy demand for steel globally. Due mostly to the electricity required for electrolysis, the High Dynamic Range (H-DR) scenario has the highest electrical energy consumption.

Figure 2.

Thermal energy requirements (up) and electrical energy requirements (below), by fuel and steel production method, for the Business as Usual (BAU) (left), H-DR (middle), and EWIN (right) scenarios, respectively.

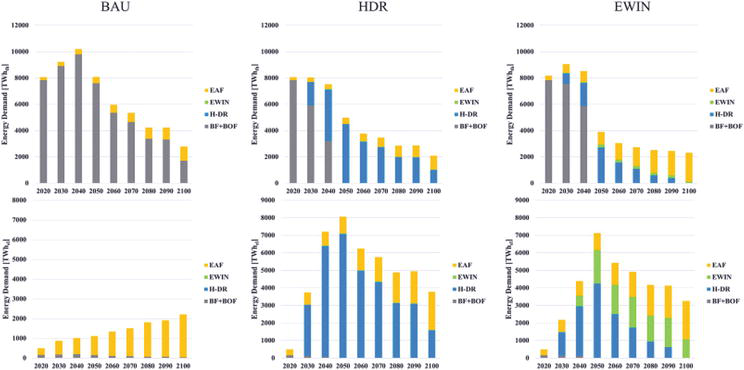

Figure 3.

Energy requirements for technology for the BAU (left), H-DR (middle), and EWIN (right) scenarios, shown on the top and bottom, respectively.

3.3 Geographical distribution

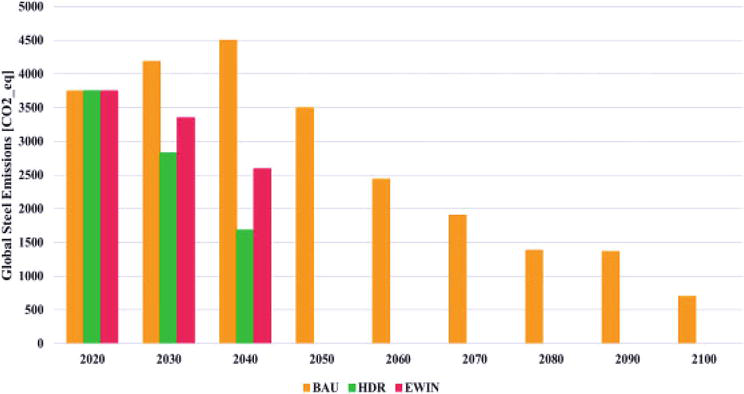

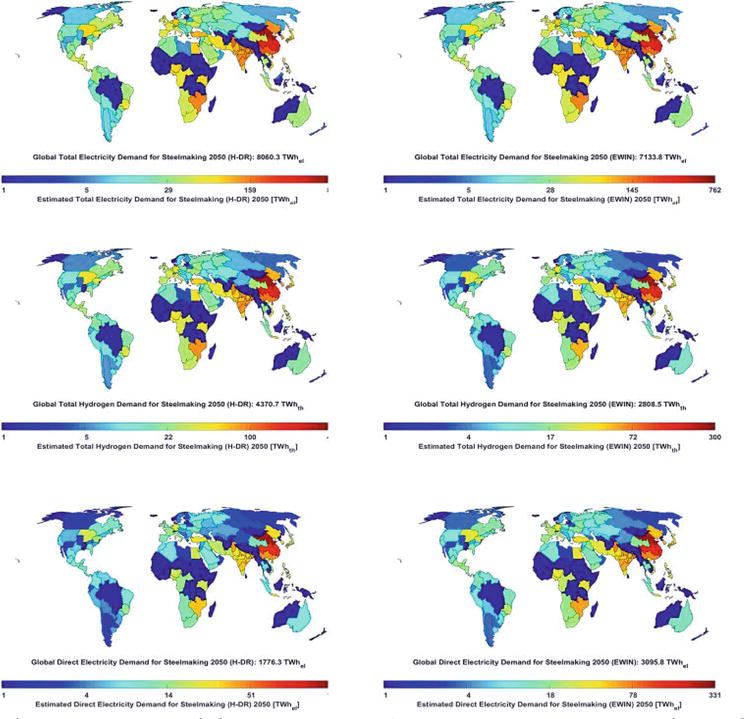

Although the scenario for steel production in Table 1 depicts an increase in the necessity for steel globally, the development of the various steel-producing countries may follow different paths. According to the findings of the analysis of 145 regions, the geographic distribution of production capacity is largely mirrored in the regional distribution (2018). Notwithstanding the chance that this structure might change, as described in Section 4, China is still the world’s top producer of steel. The color bar scales logarithmically as a result of the huge differences in production levels between the zones. According to Figure 4, China will require the most electrical and thermal energy in 2050 (2201 and 1948 TWhel, and 1193 and 767 TWhth of hydrogen for the H-DR and EWIN scenarios, respectively), as well as the most fossil fuels [3] (Figure 5).

Figure 4.

Under scenarios ranging from 2020 to 2100, worldwide CO2 emissions for the manufacture of steel are reported.

Figure 5.

Projection of the H-DR scenario’s 2050 energy requirement for steel production by geographic region.

It is anticipated that global steel production will reach its first high around 2040, followed by a brief dip for the following 20 years, then climb gradually and slowly until it surpasses the 1st peak in the latter half of the 21st century. Due in large part to recycling, which significantly lowers the thermal energy demand, the world’s thermal energy demand for the manufacturing of steel is seeing a different pattern.

3.4 Economics of future primary steel alternatives

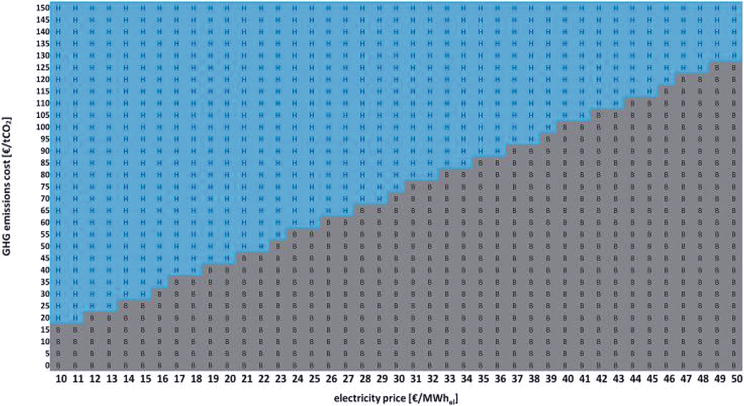

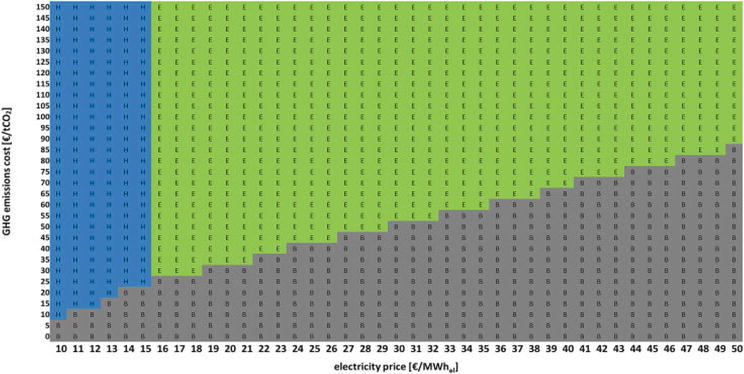

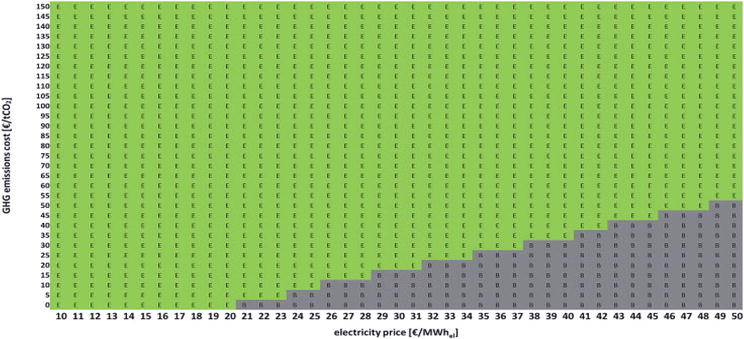

Figures 6–8 depict, accordingly, the economic feasibility of each of the steel production pathways for a range of energy prices and Greenhouse Gases (GHG) emission costs for the years 2030, 2040, and 2050. Because of the technological maturity H-DR has, it will be the least priced technology in 2030, assuming less electricity costs and a suitably more carbon pricing mechanism. In 2040, here the trend will be maintained as H-DR replaces EWIN as the preferable technology in scenarios with extremely low electricity costs and more emissions costs, respectively. EWIN is highly expensive at lower power rates than the H-DR path due to its high capital costs, which, if reduced in the following decades, will prevent the technology from seriously affecting the steel manufacturing landscape. EWIN is high energy efficient than H-DR, but its high capital costs make it less feasible than H-DR. Because of its greater energy efficiency, Fischedick et al. [5] estimate of a large decline in EWIN capex shows that EWIN will become the preferred steelmaking process for low electricity prices even in the absence of carbon pricing [6].

Figure 6.

The least expensive primary steel production method in 2030 for various power costs and GHG emission costs. Blue cells stand in for H-DR, and gray cells for blast furnace (BF) + basic- oxygen furnace (BOF).

Figure 7.

Shows the least expensive primary steel production technique for 2040, given various power costs and the cost of GHG emissions. Blue cells stand in for H-DR, green cells for EWIN, and gray cells for BF+BOF.

Figure 8.

In 2050, the least expensive primary steel production process will depend on the cost of GHG emissions and the price of power. Blue cells stand in for H-DR, green cells for EWIN, and gray cells for BF+BOF.

To fulfill the objectives of the Paris Accord and the limitations set forth in the most recent IPCC assessments for a society with zero greenhouse gas emissions, the worldwide steel sector must adapt and change. This study gives the first forecasts of global steelmaking with specific transition paths for a complete and through the end of the century with high worldwide-local resolution, the worldwide steel industry can be de-fossilized without the need of CCS or BECCS. For there to be viable routes for a full de-fossilization of the steel sector, the following prerequisites must be satisfied:

Primary steel manufacturing must replace the use of fossil fuels: Good examples of electricity-based technologies for the production of steel from raw materials are H-DR and EWIN.

To fully de-fossilize steelmaking, Carbon Capture, Storage and Utilization Technologies are insufficient and furthermore, it is hotly contested whether gaseous CO2 sequestration even comes close to meeting sustainability requirements.

A net-zero steel sector is used to decarbonize steel manufacturing. If H-DR takes over as the principal steel manufacturing method, the steel industry might have one of the highest hydrogen demand levels in 2050, with 2800–4400 TWhH2 [7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22].

It is necessary to transition the world’s energy system towards very high shares of renewable energy, particularly renewable electricity: The remaining emissions from steelmaking will be those associated with the power sector and how electricity is generated when the industry transitions to electricity-based technology. So long as steel production is entirely powered by electricity and green hydrogen, there would be no greenhouse gas emissions from the power sector, which would enable there to be no greenhouse gas emissions from the steel industry.

Steel recycling rates must be high: Steel recycling will have a major impact on the energy demand and carbon intensity of steelmaking because steel is a material that may theoretically be recycled to extremely high percentages much exceeding 90% and is already being recycled at a rate of 80.6% at the moment. The primary use of steel nowadays is structural steel, which serves as storage for steel for decades. From 2050 onward, this impact will have very major shares of steel recycling in total steel production [23, 24, 25, 26, 27, 28, 29, 30, 31, 32, 33, 34, 35, 36, 37, 38, 39, 40, 41, 42, 43].

References

1.World Steel Association by Dr Edwin Basson Director Genera, 2018

2.Fruehan RJ. Overview of steelmaking processes and their development. The Making, Shaping and Treating of Steel: Steelmaking and Refining Volume. 1998;1:2-3

3.Kallanish. Brazil’s steel production. Consumption Fall in June. 2022;1:1-22

4.Toktarova A, Walter V, Göransson L, Johnsson F. Interaction between electrified steel production and the north European electricity system. Journal of Applied Energy. Elsevier. 2022;310:1-25

5.Fischedick M, Marzinkowski J, Winzer P, Weigel M. Techno-economic evaluation of innovative steel production technologies. Journal of Cleaner Production. 2014;84:563-580. DOI: 10.1016/j.jclepro.2014.05.063

6.Lopez G, Farfan J, Breyer C. Trends in the global steel industry: Evolutionary projections and defossilisation pathways through power-to-steel. Journal of Cleaner Production. 2022;375:134182

7.Aboumahboub T, Brecha RJ, Shrestha HB, Fuentes U, et al. Decarbonization of Australia’s energy system: Integrated modeling of the transformation of electricity, transportation, and industrial sectors. Energies. 2020;13:1-39. DOI: 10.3390/en13153805

8.Aghahosseini A, Breyer C. Assessment of geological resource potentialfor compressed air energy storage in global electricity supply. Energy Conversion and Management. 2018;169:161-173. DOI: 10.1016/j.enconman.2018.05.058

9.Arens M, Åhman M, Vogl V. Which countries are prepared to green their coal- based steel industry with electricity? - reviewing climate and energy policy as well as the implementation of renewable electricity. Renewable and Sustainable Energy Reviews. 2021;143:110938. DOI: 10.1016/j.rser.2021.110938

10.Bailera M, Lisbona P, Pena B, Romeo LM. A review on CO2 mitigation in the Iron and steel industry through power to X processes. Journal of CO2 Utilisation. 2021;46:101456. DOI: 10.1016/j.jcou.2021.101456

11.Bhaskar A, Assadi M, Nikpey Somehsaraei H. Decarbonization of the iron and steel industry with direct reduction of iron ore with green hydrogen. Energies. 2020;13:1-23. DOI: 10.3390/en13030758

12.Bogdanov D, Farfan J, Adovskaia K, Aghahosseini A, Child M, Gulagi A, Oyewo AS, et al. Radical transformation pathway towards sustainable electricity via evolutionary steps. Nature Communications. 2019;10(1077):1-16

13.Bogdanov D, Gulagi A, Fasihi M, Breyer C. Full energy sector transition towards 100% renewable energy supply: Integrating power, heat, transport and industry sectors including desalination. Applied Energy. 2021a;283:116273. DOI: 10.1016/j.apenergy.2020.116273

14.Meyers RA. Sustainability Science and Technology. New York: Springer New York. pp. 1-30. DOI: 10.1007/978-1-4939-2493-6_1071-1

15.Brown TW, Bischof-Niemz T, Blok K, Breyer C, Lund H, Mathiesen BV. Response to ‘burden of proof: A comprehensive review of the feasibility of 100% renewable-electricity systems. Renewable and Sustainable Energy Reviews. 2018;92:834-847. DOI: 10.1016/j.rser.2018.04.113

16.Child M, Koskinen O, Linnanen L, Breyer C. Sustainability guardrails for energy scenarios of the global energy transition. Renewable and Sustainable Energy Reviews. 2018;91:321-334. DOI: 10.1016/j.rser.2018.03.079

17.Creutzig F, Ravindranath NH, Berndes G, Bolwig S, Bright R, Cherubini F, et al. Bioenergy and climate change mitigation: An assessment. GCB Bioenergy. 2015;7:916-944. DOI: 10.1111/gcbb.12205

18.Devlin A, Yang A. Regional supply chains for decarbonising steel: Energy efficiency and green premium mitigation. Energy Conversion and Management. 2022;254:115268. DOI: 10.1016/j.enconman.2022.115268

19.Energiewende, Agora, Guidehouse. Making Renewable Hydrogen Cost-Competitive: Policy Instruments for Supporting Green H₂.ETC, 018. Mission Possible: Reaching net-zero carbon emissions from harder-to-abate sectors [WWW Document]. 2021. Available from: https://www.energy-transitions.org/publications/mission-possible/, [Accessed: October 8, 2021]

20.Gielen D, Saygin D, Taibi E, Birat J-P. Renewables-based decarbonization and relocation of iron and steel making: A case study. Journal of Industrial Ecology. 2020;24:1113-1125. DOI: 10.1111/jiec.12997

21.ETOGAS, 2013. Power to Gas: Intelligente Konvertierung und Speicherung von Energie in der industriellen Umsetzung [WWW Document]. ETOGAS GmbH, Stuttgart. Available from: https://goo.gl/E1vzLb, [Accessed: September 28, 2021]

22.Fasihi M, Weiss R, Savolainen J, Breyer C. Global potential of green ammoniabased on hybrid PV-wind power plants. Applied Energy. 2021;294:116170. DOI: 10.1016/j.apenergy.2020.116170

23.Galimova T, Ram M, Bogdanov D, Fasihi M, Khalili S, Gulagi A, et al. Global demand analysis for carbon dioxide as raw material from key industrial sources and direct air capture to produce renewable electricity-based fuels and chemicals. Vol. 1. pp 1-16. DOI: 10.1016/j.jclepro.2022.133920

24.Goransson L, Lehtveer M, Nyholm E, Taljegard M, Walter V. The benefit of collaboration in the north European electricity system transition—System and sector perspectives. Energies. 2019;12:4648. DOI: 10.3390/en12244648

25.Grond, L., Schulze, P., Holstein, J., 2013. Systems Analyses Power to Gas [WWW Document]. KEMA NV, Groningen. URL: https://docplayer.net/7637393-Dnv-kema-energy-sustainability-final-report-systems-analyses-power-to-gas-deliverable-1-technology-review.html, [Accessed: September 28, 2021]

26.Hansen K, Breyer C, Lund H. Status and perspectives on 100% renewable energy systems. Energy. 2019;175:471-480. DOI: 10.1016/j.energy.2019.03.092

27.Hasanbeigi A, Price L, Chunxia Z, Aden N, Xiuping L, Fangqin S. Comparison of iron and steel production energy use and energy intensity in China and the U.S. Journal of Cleaner Production. 2014;65:108-119. DOI: 10.1016/j.jclepro.2013.09.047

28.IEA. Iron and Steel [WWW Document]. 2020a. Available from: https://www.iea.org/reports/iron-and-steel, [Accessed: October 8, 21]

29.Iron and steel technology roadmap. International steel Agency. Vol. 1. 2020. pp. 1-186

30.IEA. Energy Technology Perspectives 2020. Paris: International Energy Agency; 2020c

31.IEA, 2020d. World Energy Model [WWW Document]. IEA, Paris. Available from: https://www.iea.org/reports/world-energy-model, [Accessed: September 24, 2021]

32.IEA. An Energy Sector Roadmap to Carbon Neutrality in China [WWW Document]. 2021d. Available from: https://www.iea.org/reports/an-energy-sector-roadmap-to-carbon-neutrality-in-china

33.Jaxa-Rozen M, Trutnevyte E. Sources of uncertainty in long-term global scenarios of solar photovoltaic technology. Nature Climate Change. 2021;11:266-273. DOI: 10.1038/s41558-021-00998-8

34.Karakaya E, Nuur C, Assbring L. Potential transitions in the iron and steel industry in Sweden: Towards a hydrogen-based future? Journal of Cleaner Production. 2018;195:651-663. DOI: 10.1016/j.jclepro.2018.05.142

35.Khalili S, Rantanen E, Bogdanov D, Breyer C. Global transportation demand development impacts on the energy demand and greenhouse gas emissions in a climate-constrained world. Energies. 2019;12:3870. DOI: 10.3390/en12203870

36.Zhang K. Journal of Cleaner Production. Delft, Netherland: Delft University of Technology; Open Access. 2019;240:1-21. DOI: 10.1016/S0959-6526(19)33382-7

37.Mandova H, Leduc S, Wang C, Wetterlund E, Patrizio P, Gale W, et al. For CO2 emission reduction using biomass in European integrated steel plants. Biomass Bioenergy. 2018;115:231-243. DOI: 10.1016/j.biombioe.2018.04.021

38.Mandova H, Patrizio P, Leduc S, Kjarstad J, Wang C, Wetterlund E, et al. Achieving carbon-neutral iron and steelmaking in Europe through the deployment of bioenergy carbon capture and storage. Journal of Cleaning Products;218:118-129. DOI: 10.1016/j.jclepro.2019.01.247

39.Midrex. World Direct Reduction Statistics 2018 [WWW Document]. 2019. Available from: https://www.midrex.com/wp-content/uploads/Midrex-STATSbook2019Final.pdf, [Accessed: October 8, 2021]

40.Morfeldt J, Nijs W, Silveira S. The impact of climate targets on future steel production – An analysis based on a global energy system model. Journal of Cleaner Production. 2015;103:469-482. DOI: 10.1016/j.jclepro.2014.04.045

41.Neij L. Cost development of future technologies for power generation—A study based on experience curves and complementary bottom-up assessments. Energy Policy. 2008;36:2200-2211. DOI: 10.1016/j.enpol.2008.02.029

42.Nuber D, Eichberger H, Rollinger B. Circored fine ore direct reduction – The future of modern electric steelmaking. Millennium Steel. 2006;126(47–51):2006

43.Otto A, Robinius M, Grube T, Schiebahn S, Praktiknjo A, Stolten D. Power-to-Steel: reducing CO2 through the integration of renewable energy and hydrogen into the German steel industry. Energies. 2017;10:1-21. DOI: 10.3390/en10040451

Written By

Nidhi Nischal and M. Vijay Kumar

Submitted: 06 May 2023Reviewed: 12 May 2023Published: 15 December 2023